Skip to content

Skip to content When divorce becomes real, one of the first fears is simple and urgent: Will I have enough money to get through this without being blindsided?

That fear is valid. In Texas, financial preparation isn’t just paperwork. It’s protection. If you approach divorce with organized records, a clear picture of your assets and debts, and a plan for immediate cash flow, you put yourself in a much stronger position from the day the case begins.

If you’ve been searching for How to Prepare Financially for Divorce in Texas (Checklist), the most important shift is this. Don’t treat preparation like a chore. Treat it like a strategy. Every statement you gather, every account you identify, and every budget line you build helps you protect your future under Texas law.

Why Financial Preparation Is Your First Line of Defense

Many people come into divorce feeling financially foggy. One spouse handled most of the bills. Accounts are joint. Credit cards are on autopay. Retirement funds exist, but the details are unclear. That uncertainty is exactly what creates financial power imbalances in a Texas divorce.

Texas is a community property state. That means property acquired during the marriage is generally part of the marital estate and subject to division in a manner the court considers just and right. If you don’t know what exists, what you owe, what was owned before marriage, or what’s been mixed together over time, you’re starting from a weaker position than you need to.

The cost of waiting

Delay is expensive. So is disorder.

The financial spread between a cooperative case and a contested one is dramatic. The average cost of a Texas divorce without shared children is $15,600, while divorces involving shared children average $23,500. In contrast, an uncontested divorce with limited attorney help can cost as little as $1,500 to $3,500 according to Texas divorce cost data discussed here.

That doesn’t mean every case can or should be uncontested. Some cases involve serious disagreements over property, children, support, or safety. But it does mean this: when you walk in prepared, you reduce avoidable conflict. You spend less time chasing missing records, arguing over basic facts, and reacting to financial surprises.

Practical rule: The earlier you organize your finances, the more choices you keep.

What preparation actually does for you

Good preparation helps you do more than fill out forms. It helps you:

- Identify what you own so assets don’t get overlooked

- Document what you owe so debts don’t get shifted unfairly

- Spot separate property issues before they become courtroom fights

- Strengthen your position for settlement because your numbers are supported by records

- Prepare for temporary orders involving who pays which bills while the case is pending

Texas divorces often move quickly at the beginning. Once the case is filed, immediate questions can arise about the home, access to accounts, support, and parenting arrangements. If your financial house is in order, you can respond with facts instead of panic.

The real trade-off

Some people avoid financial prep because they don’t want to “make things worse.” I understand that instinct. But silence and passivity usually don’t preserve peace. They just leave you exposed.

What works is calm, lawful preparation. Gather records. Make copies. Learn the difference between community and separate property. Understand your monthly cash flow. Protect access to basic living funds. Those steps aren’t aggressive. They’re responsible.

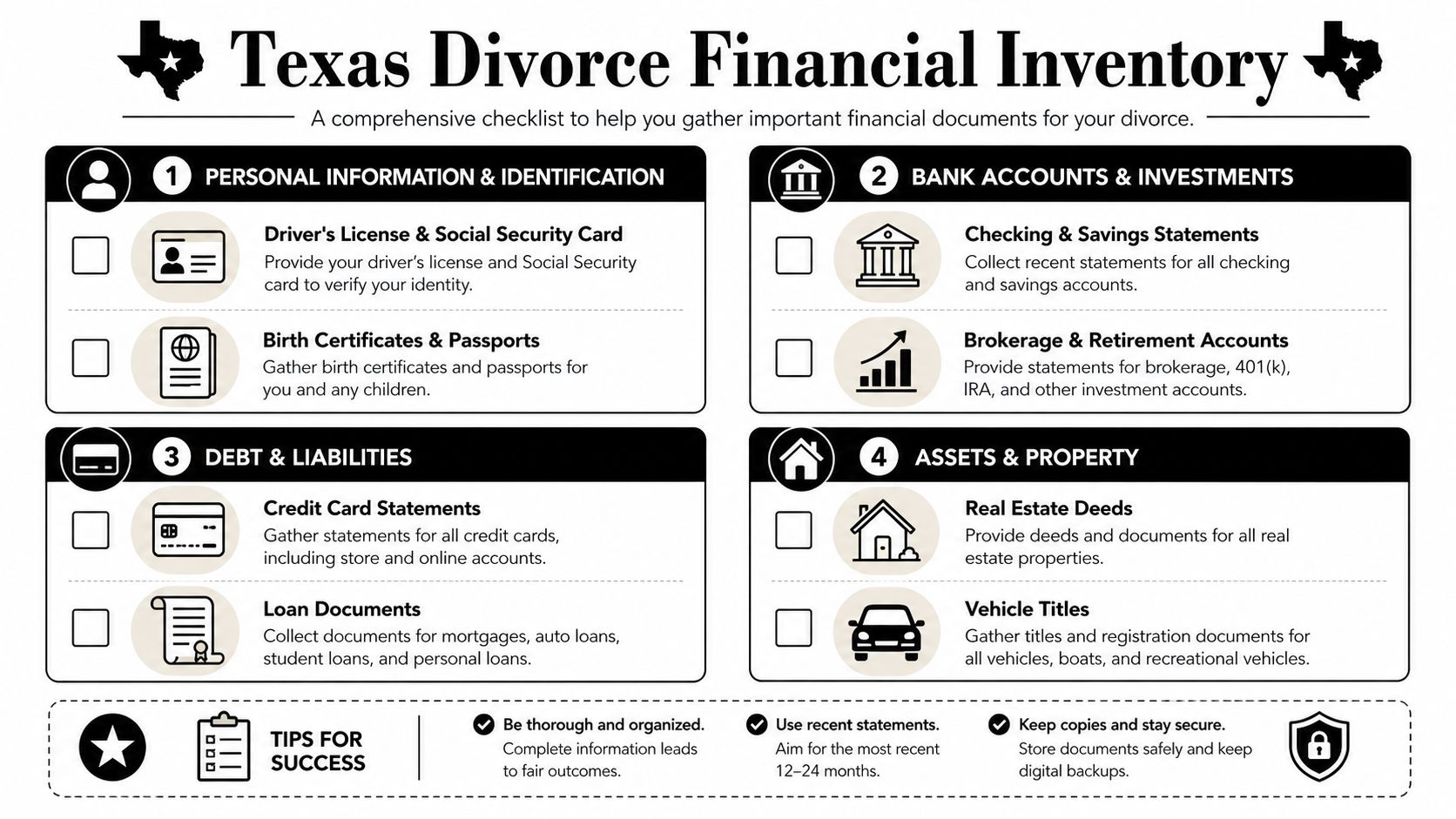

Build Your Complete Financial Inventory

Your financial inventory is the foundation of the entire case. If the inventory is incomplete, every later conversation about settlement, mediation, support, and property division becomes harder than it needs to be.

Texas courts start from a presumption that property is community property. To claim an asset as separate, you must provide clear and convincing evidence by tracing it with documentation like pre-marital asset statements and records showing it was never commingled with joint funds. Failure to do so means the asset will likely be divided, as explained in this discussion of financial documents and tracing in Texas divorce.

Start with the core records

Build one master file, digital or paper, and keep it organized by category. In most cases, you should gather enough records to show patterns, not just snapshots.

- Bank records. Collect checking and savings statements for all individual and joint accounts.

- Credit card records. Pull statements that show balances, spending patterns, and any unusual transfers.

- Income proof. Save pay stubs, bonus records, commission information, and other proof of earnings.

- Tax returns. Include personal returns and any business returns if either spouse owns a business.

- Retirement and investment accounts. Gather account statements and note contribution history where possible.

- Real estate records. Include deeds, mortgage statements, refinance paperwork, and property tax records.

- Vehicle documents. Titles, loan statements, and payoff information matter.

- Insurance policies. Health, life, auto, homeowners, and disability policies can all matter in divorce.

- Business records. If a spouse owns part of a company, gather formation documents, balance sheets, profit-and-loss statements, and compensation records.

If you struggle with paper clutter, one practical step is implementing financial receipt systems so you can sort records by vendor, date, and category before your attorney ever has to review them.

Build an asset and debt list in plain English

Don’t wait for perfect documents before making your list. Start with a working inventory and improve it as you go.

Use a simple chart like this:

| Category | What to list | Why it matters |

|---|---|---|

| Cash accounts | Bank name, account type, ownership | Shows available funds and whether accounts are joint or separate |

| Real estate | Address, title holder, loan balance | Helps identify equity and source of acquisition |

| Retirement | Account type and current statement | Retirement funds often require special handling in divorce |

| Debts | Creditor, balance, whose name is on it | Debt allocation can be as important as asset division |

| Personal property | Vehicles, jewelry, collections, valuables | These items are often forgotten until late in the case |

This is also the stage where many people realize they need formal discovery. If your spouse controls most of the records or you suspect something is missing, learn how the discovery phase of divorce can force production of documents and sworn answers.

If an account exists, list it. If you aren’t sure whether it matters, list it anyway.

Don’t overlook digital assets

Modern divorces involve more than bank accounts and retirement plans. If you or your spouse own cryptocurrency, NFTs, or other digital assets, treat them like real property interests that need documentation and valuation.

In high-net-worth cases, especially where business ownership is involved, digital assets can become a serious tracing problem. Wallet records, exchange histories, and transaction logs may matter. If a spouse claims crypto is separate property, documentation becomes even more important because the same tracing rules still matter.

Separate property claims rise or fall on documents

Separate property usually includes things owned before marriage, certain gifts, and inheritances. But the label alone doesn’t protect the asset. The proof does.

Create a separate file for any asset you believe is separate and include:

- Original acquisition records showing when and how you got it

- Statements over time showing where the asset was held

- Evidence against commingling if funds moved through joint accounts

- Title or ownership documents where applicable

What doesn’t work is relying on memory, informal explanations, or a belief that “everyone knows” something was yours before marriage. Courts decide property issues based on evidence.

Secure Your Finances and Protect Your Credit

Once you know what exists, take steps to protect access and stability. This part matters because some divorces become financially tense before the petition is ever filed.

If one spouse controls online banking, manages the passwords, or can freeze practical access to money, the other spouse can end up struggling to pay rent, groceries, transportation, or attorney fees. That’s a dangerous position to be in.

Open an account you control

A practical first move is opening an individual bank account in your own name and directing your paycheck there if appropriate. Financial experts recommend establishing an individual bank account and routing your paycheck to it before filing. This creates a documented baseline for your living expenses and ensures you have access to funds for an attorney retainer and immediate costs, as approximately 35% of divorcing individuals discover hidden debts or accounts during discovery, based on this discussion of preparing divorce finances in Texas.

This does not mean hiding money, draining joint accounts, or acting deceptively. It means making sure you can function. There’s a difference between protecting access and trying to manipulate the estate.

Pull your credit and read it carefully

A current credit report can reveal problems that don’t show up in a shared checking account. Look for:

- Unknown revolving debt in either spouse’s name

- Personal loans you didn’t know existed

- Joint obligations with missed payments

- Recently opened accounts that need explanation

- Address or employment discrepancies that suggest undisclosed activity

A credit report also helps your attorney spot issues early. If there’s a hidden debt problem, it’s better to find it before settlement talks than after you sign a decree.

Keep your actions reasonable

Texas judges care about conduct around finances once divorce is underway. If you move money, be prepared to explain why, how much, and where it went. Reasonableness matters.

A simple framework helps:

- Cover necessities. Housing, food, insurance, transportation, and legal fees are ordinary concerns.

- Document transfers. Keep screenshots, receipts, and account statements.

- Avoid cash withdrawals without records. Unexplained cash creates suspicion.

- Don’t cancel essentials. Insurance and bill disruptions can create bigger problems fast.

If you’re worried your spouse may empty accounts or interfere with finances after filing, temporary court relief may be necessary. In some cases, a temporary restraining order in a Texas divorce can help preserve property and stop harmful financial conduct while the case proceeds.

Here’s a short video that helps explain the kind of early divorce planning many Texans need:

Immediate priority: Make sure you can pay for your life next month, not just argue about fairness next year.

Protect your digital access too

Financial security also includes privacy. Change passwords for your personal email, cloud storage, and financial apps if you can do so lawfully and safely. Save copies of records in a location your spouse can’t alter.

What works is quiet, documented, ordinary self-protection. What doesn’t work is retaliation.

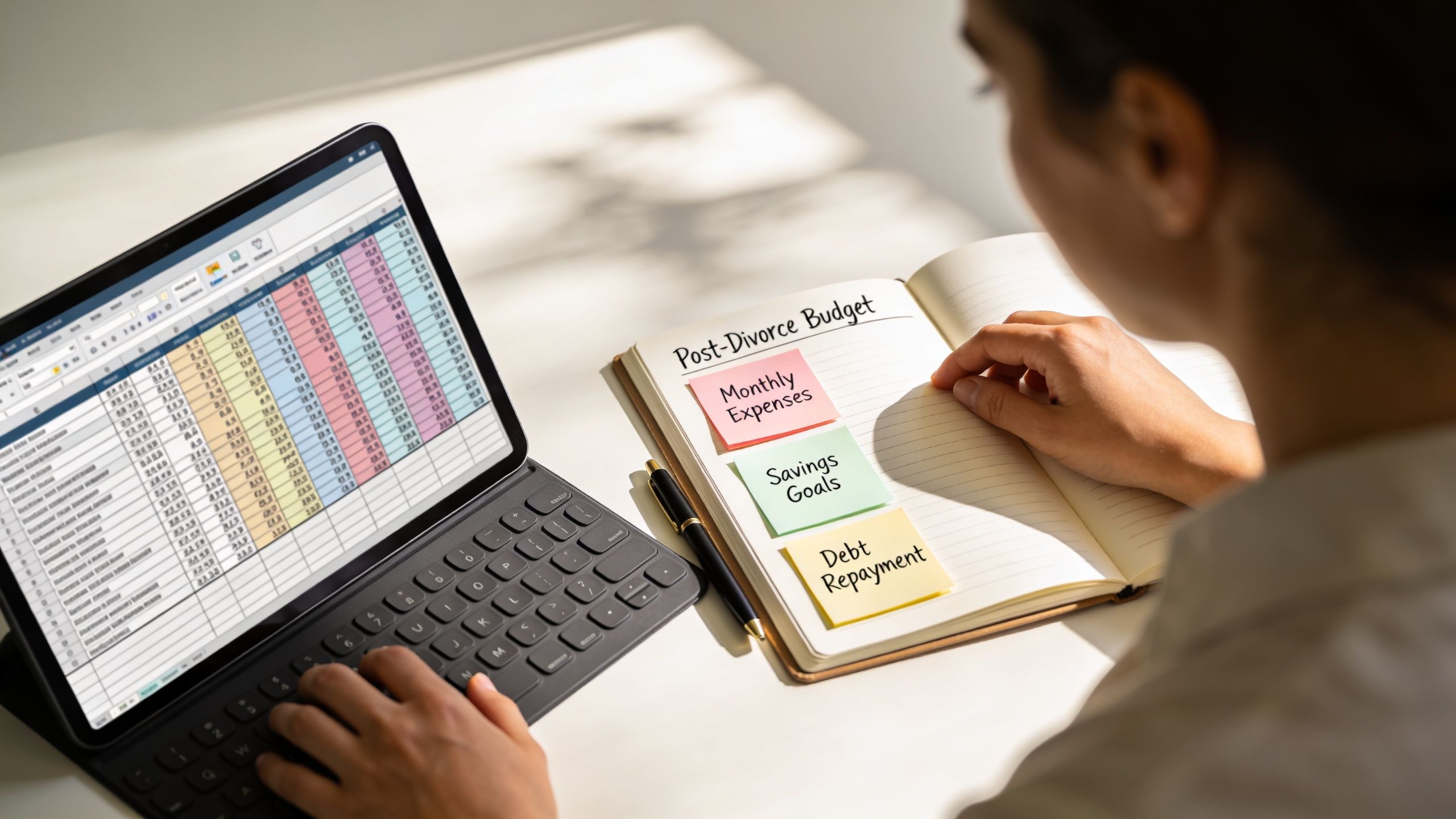

Create Your Post-Divorce Budget and Financial Plan

A lot of people spend all their energy looking backward at what the marriage cost. You also need to look forward at what your life will cost after divorce.

That budget matters for settlement talks, mediation, temporary orders, child-related expenses, and any claim involving spousal maintenance. Texas requires meaningful financial disclosures early in the case. In Texas, parties must provide mandatory financial disclosures within 30 days of the divorce response. This includes income and expense information that forms the basis for support calculations. Spousal maintenance is capped at the lesser of $5,000 per month or 20% of the payer's average monthly gross income, according to this overview of Texas divorce financial disclosures.

Start with current household reality

Before you can project a post-divorce budget, identify how money works now. Use actual statements, not guesses.

Break your current spending into three groups:

| Budget group | Examples | Why it matters |

|---|---|---|

| Fixed expenses | Mortgage or rent, insurance, car payments | These usually continue in some form after separation |

| Variable expenses | Groceries, gas, school costs, household spending | These can shift quickly once households split |

| Irregular expenses | Repairs, annual fees, medical costs, activities | These are easy to forget and can wreck a budget |

If children are involved, include school expenses, health costs, childcare, and activity-related spending. Child support discussions are only as accurate as the financial information behind them.

Build the budget you’ll actually live on

Your post-divorce budget should answer a few direct questions.

Can you afford to stay in the home? If not, what would replacement housing cost? What happens if one income becomes responsible for two households? What expenses are likely to rise because you’re no longer sharing them?

Use realistic categories such as:

- Housing including rent or mortgage, taxes, repairs, and utilities

- Transportation including fuel, insurance, payment, tolls, and maintenance

- Health care including premiums, prescriptions, and out-of-pocket costs

- Children’s needs including school, supplies, clothing, childcare, and activities

- Debt service including minimums and any required payoff planning

- Savings for emergencies and predictable future expenses

A budget is evidence. It shows what you need, what you can pay, and where a proposed settlement falls apart.

Understand how this affects negotiation

A vague budget leads to vague negotiation. A supported budget gives you something far stronger. It shows the court or the other side how your monthly life works.

That matters in mediation. It matters at temporary orders. It matters if one spouse is asking for maintenance or arguing they can’t pay.

If you’re a parent, this is also the right time to think beyond dollars. Parenting schedules affect transportation, childcare, after-school care, and work flexibility. If you need more guidance on those issues, our firm’s resources on child custody, child support, mediation, and enforcement can help you understand how the financial side connects to parenting decisions.

Don’t build a fantasy budget

What doesn’t work is creating a best-case budget based on hope. Courts and opposing counsel will test your numbers. If they don’t match your documents or your real lifestyle, your credibility suffers.

Use conservative figures. Include the expenses you know are coming. If something is uncertain, flag it and discuss it with your lawyer.

Assembling Your Professional Team and Preserving Evidence

Some divorces can be resolved with straightforward financial records and solid negotiation. Others need specialists. Knowing the difference can save you from expensive mistakes.

If your case involves a business, executive compensation, complex investments, or a spouse who controls the books, outside financial help may be necessary. In high-net-worth divorces, especially those involving business ownership, a forensic accountant is often necessary to conduct a business valuation and trace assets. A 2025 report noted that in the DFW area, 28% of high-asset divorces involved undisclosed crypto assets, as noted in this article about Texas divorce financial information and crypto tracing.

When a forensic accountant makes sense

A forensic accountant is often useful when:

- A business is involved and income may not match tax return appearances

- Accounts are layered across companies, trusts, partnerships, or digital platforms

- Cash flow seems inconsistent with the lifestyle in the marriage

- Separate property tracing is complicated because funds were mixed over time

- Crypto or digital assets exist and the records are technical or incomplete

A financial professional can also help distinguish between income available for support and paper income that doesn’t reflect real cash flow.

Watch for warning signs of hidden assets

You don’t need to make accusations without proof. But you should take warning signs seriously.

Common red flags include sudden transfers, unusual debt, incomplete disclosures, missing statements, new passwords, changes in business compensation, or a spouse who becomes unusually secretive about taxes and accounts. If those signs are present, preserve what you can access lawfully and speak with counsel early.

For a closer look at these issues, review this guide on hidden assets in Texas divorce.

Save records in the ordinary course. Don’t alter them, annotate them, or cherry-pick only the helpful ones.

Preserve evidence the right way

Evidence preservation is often simple, but it needs consistency.

Save PDFs of statements. Screenshot account summaries. Keep emails about money. Preserve texts discussing large purchases, transfers, or debts. If a business is involved, keep copies of anything that shows compensation, distributions, reimbursements, or owner perks.

If you need help sorting out what type of professional to involve, one option is the Law Office of Bryan Fagan, PLLC, which handles Texas divorce matters involving property division, support, mediation, temporary orders, and high-asset disputes. The right team depends on the complexity of your facts, not on a one-size-fits-all checklist.

What to Do Next A Clear Path Forward

Financial preparation changes the tone of a divorce. It takes you from reacting to planning.

You don’t need to solve every issue in one weekend. You do need to start. Gather the records. Identify the accounts. Protect access to money you can lawfully use for living expenses. Build a budget based on real numbers. If your case involves a business, digital assets, or missing information, get professional help before small problems become expensive ones.

Key takeaway

The strongest financial position in a Texas divorce usually comes from a few disciplined habits:

- Know what exists by building a complete inventory

- Know what’s yours to prove if separate property is part of the case

- Know how you’ll function by securing access to funds and credit information

- Know what life will cost after divorce through a grounded monthly budget

- Know when to escalate to attorneys, forensic accountants, or other professionals

Texas divorce law gives structure to the process, but structure alone won’t protect you. Documentation will. Timing will. Good decisions at the beginning will.

What works and what doesn’t

What works is preparation that is lawful, calm, and thorough. What doesn’t work is hiding your head in the sand, hoping your spouse will disclose everything voluntarily, or assuming the court will somehow piece your financial life together for you.

If you have children, remember that financial planning also supports better custody and support planning. If you have a business, the records matter more than ever. If you’re worried about immediate account access or retaliation, temporary relief may be part of the strategy.

You don’t have to walk into this process guessing. You can walk into it prepared.

If you’re getting ready for divorce and want a clear plan for protecting your money, your property, and your next chapter, schedule a free consultation with the Law Office of Bryan Fagan, PLLC. You’ll get Texas-focused guidance on property division, custody, support, mediation, temporary orders, and the financial steps that can make a real difference from the start.