Skip to content

Skip to content You may have just realized that your spouse’s compensation is not just a salary, but a stack of stock options, RSUs, or company shares that could shape your financial future long after the divorce is over.

That moment rattles people. A bank account feels easy to divide. A house feels concrete. Equity compensation does not. It can be unvested, hard to value, restricted by company rules, and tied to tax consequences that do not show up on the first spreadsheet.

The good news is that dividing stock options in Texas divorce cases is not guesswork. Texas law gives courts and lawyers a workable framework for sorting out what belongs to the community estate and what remains separate property. The challenge is not just applying the legal rule. The challenge is making sure the decree, tax planning, and payout structure protect what you receive in the end.

Your Guide to Stock Options and Your Divorce

A common turning point comes during the property inventory. You ask for pay records and retirement statements, then discover references to grants, vesting schedules, exercise windows, and equity award summaries. Suddenly, the divorce is not only about who keeps the house or how to divide savings. It is also about compensation that may not fully mature until years from now.

That is where many people freeze. They worry they will miss something valuable or agree to a settlement that looks fair on paper but falls apart once taxes, timing, and restrictions show up.

Why these assets need close attention

Stock options and similar awards often sit in the background during marriage. They may not feel real until they vest or are exercised. In divorce, that delay creates risk.

You need to know:

- What kind of award exists: Stock options, RSUs, and purchase plans behave differently.

- When the award was granted: Timing matters under Texas property law.

- What conditions still apply: Continued employment, vesting, and company transfer rules can all affect value.

- How the payout will happen: A future payout may create tax and cash flow problems later.

Many couples once planned these assets together. If you are trying to rebuild financial stability after separation, it can help to revisit broader money planning habits, including achieving financial goals as a couple, because divorce often exposes which long-term financial assumptions were never clearly documented.

What usually works and what usually does not

What works is a document-first approach. You gather grant notices, plan documents, vesting schedules, brokerage statements, and employment agreements early.

What does not work is assuming the payroll summary tells the whole story. It usually does not.

Tip: If an award has multiple vesting dates, treat each tranche as a separate problem until your attorney confirms otherwise. Small timing differences can change characterization.

People also make mistakes when they focus only on percentages. Ownership percentage matters, but net value matters more. If you receive a future share that you cannot control, cannot sell right away, or must report differently for tax purposes, your outcome may look very different from the decree language.

Understanding Your Spouse’s Equity Awards

A lot of clients walk into my office with a compensation portal screenshot and one question. "Do I get half of this?" That screenshot is a starting point, not an answer.

Equity compensation can represent a large part of a family’s balance sheet, but the label on the award rarely tells you how it should be divided or what it will be worth after divorce. Before anyone can negotiate a fair settlement, you need to identify the award type, the governing plan rules, and the tax consequences that may hit months or years after the decree. For a broader foundation on how Texas courts approach property division, review this guide to the division of marital assets in Texas.

Equity Award Types at a Glance

| Award Type | What You Get | Key Feature |

|---|---|---|

| Stock Options | A right to buy company stock later if plan rules allow | Value depends on timing and stock price |

| RSUs | Company shares or cash value after vesting conditions are met | No purchase required by the employee |

| ESPPs | A chance to buy company stock through an employee purchase plan | Built around payroll participation |

| Incentive-style option awards | A type of option subject to specific plan and tax treatment rules | Can require close review of exercise and holding rules |

| Non-qualified option awards | A common form of option compensation | Often handled differently from incentive-style awards |

Stock options in plain English

A stock option is a contractual right. It gives the employee the chance to buy shares later at a set price if the plan terms are satisfied.

That distinction matters in divorce because the option may have no current cash value, may not be transferable, and may create taxable income only if the employee spouse exercises it later. A decree that awards a percentage without addressing who controls exercise, who advances the exercise cost, and who pays the resulting tax can leave the non-employee spouse with a paper victory and no practical way to collect.

Start with a few direct questions:

- What is the grant date?

- What service period was the award meant to compensate?

- Has the option vested, and if so, when?

- Is the option currently exercisable?

- Does the option expire quickly if employment ends?

- Does the plan prohibit transfer to a former spouse?

Those answers shape both characterization and settlement strategy.

RSUs require a different analysis

Restricted Stock Units, or RSUs, usually do not give the employee a right to buy shares. They are usually a promise to deliver shares or a cash equivalent later if the vesting conditions are met.

Clients often assume RSUs are easier because there is no exercise price. Sometimes they are. But they can create their own problems. If vesting happens after divorce, the employee spouse may receive payroll withholding, a Form W-2, and shares deposited into an account the other spouse cannot access. That means the decree needs more than a percentage. It needs a payment procedure, a deadline, record-sharing requirements, and a clear method for handling withholding so the non-employee spouse receives the intended net benefit rather than an avoidable dispute.

General Texas divorce guidance discussing stock-based compensation often treats restricted stock and options under similar characterization principles. The practical details still differ, especially on payout mechanics and later tax reporting.

ESPPs and why they still matter

An Employee Stock Purchase Plan usually looks less complicated than an unvested option grant, but it should not be ignored.

ESPP shares are often acquired through payroll deductions during a set offering period. That means the account may contain a mix of contributions made during marriage, shares purchased at a discount, and stock that has already been sold. In practice, I look for the offering periods, payroll records, purchase confirmations, and any later sales because each step can affect reimbursement claims, capital gains reporting, and the true net value of the account.

The documents you should request

Do not rely on a compensation summary or year-end paystub. Those documents rarely show enough detail to draft enforceable divorce language.

Request the underlying records:

- Grant paperwork: This identifies the grant date, award type, and basic terms.

- Vesting schedules: Each tranche may need separate treatment.

- Plan documents: These often control transfer restrictions, expiration rules, and what happens after termination of employment.

- Brokerage records: These show exercises, sales, tax withholding, and current holdings.

- Employment agreements or offer letters: These may explain whether the award was intended to reward past service, future service, or both.

- Tax forms: W-2s, 1099s, and prior exercise records help show how the company and brokerage reported the compensation.

One practical point matters here. In many cases, the decree and the stock plan have to work together. If the plan does not allow direct transfer to a former spouse, the order should say exactly how notice will be given, when the employee spouse must exercise or sell if required, how taxes and costs will be allocated, and when the non-employee spouse gets paid.

That is how you protect the value of the award, not just the percentage written on paper.

How Texas Law Characterizes Stock Options

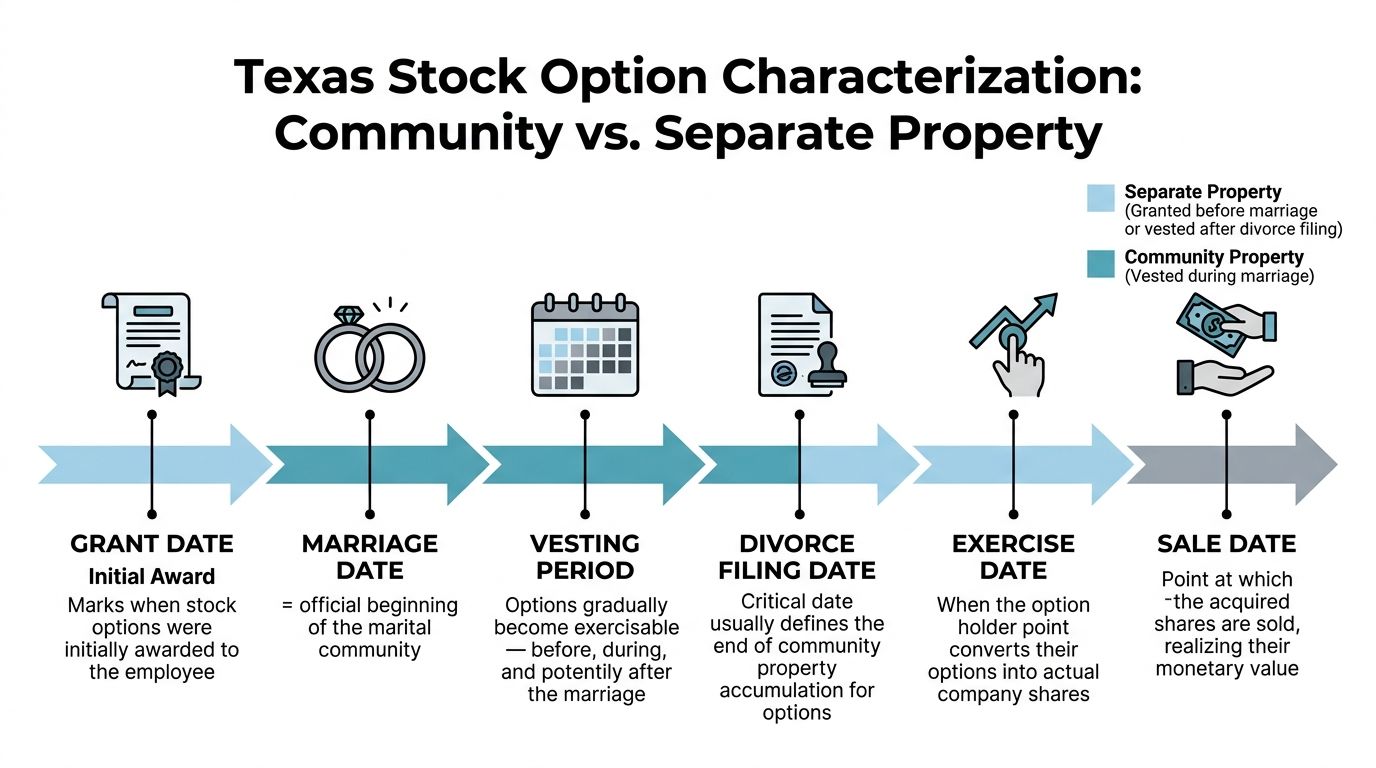

A divorce decree can say you receive half of a stock option award and still leave you with a future fight over what that means. Under Texas law, the first question is not who sees the grant in the online portal. The first question is what part of that award was earned during the marriage, what part was earned outside the marriage, and how that characterization affects the after-tax value each spouse may ever receive.

Texas treats stock options differently from a regular paycheck because the earning period often stretches across multiple dates. Grant date matters. Vesting date matters. The date of marriage and the date of divorce matter too.

Texas Family Code Section 3.007 gives courts a time-rule framework for separating the community and separate portions of stock options and similar rights. That rule brings structure to a problem that used to produce more inconsistent results. It also gives lawyers and experts a roadmap for drafting decrees that match the economics of the award instead of guessing at a percentage.

Why Texas uses a time-based rule

Many equity awards are compensation for a span of service, not a single day. An employer may grant options to reward past performance, to keep an employee in place, or to do both at once. Texas addresses that reality by measuring the relevant service period rather than stopping at the grant date.

That approach creates results that surprise people. An award granted before marriage can still have a community component if part of the earning period falls during the marriage. An award granted during marriage can also include a separate property component if vesting depends on continued service after divorce.

If you want more background on how courts sort property generally, this overview of division of marital assets in Texas gives the broader community-property framework.

The core formula for grants before marriage

For options granted before marriage but vesting later, Texas does not automatically label the whole grant as separate property. The separate property portion is based on the time outside the marriage that counts toward earning the award. In practical terms, that usually includes the period from grant to marriage and the period from divorce to vesting, compared against the full period from grant to vesting.

A simple example shows how this works. If a grant is made before marriage, vests years later, and the marriage covers only part of that full earning period, the community estate usually owns only the slice tied to the marital portion of the timeline. The employee spouse keeps the separate share. The community share is then subject to division in the divorce.

That distinction matters on paper and in actual dollars. If the decree overstates the community percentage, one spouse may end up paying the other on value that Texas law would have treated as separate property. If the decree understates the community share, the non-employee spouse may lose value that should have been preserved.

The rule for grants during marriage

Options granted during marriage are not always entirely community property either. If the award requires continued employment after divorce before it vests, Texas can treat the post-divorce service period as part of the employee spouse’s separate property interest.

That is why the grant date alone rarely answers the question. The service period attached to the award often drives the characterization.

Multi-tranche awards need separate attention

A single grant may vest in several installments over several years. Each tranche can require its own calculation because each one may have a different vesting date and, in turn, a different community percentage.

Sloppy drafting causes expensive problems later. I often see spouses focus on the total number of options and miss the fact that tranche one, tranche two, and tranche three may not belong to the community in the same proportions. If the decree treats the whole grant as one bucket, the math can be wrong from the start. That error then spills into tax reporting, exercise decisions, and the net amount each spouse receives.

Key takeaway: One grant does not always equal one percentage. Staggered vesting usually requires tranche-by-tranche analysis.

Why characterization affects more than ownership

Characterization is the legal starting point, not the end of the analysis. Once the community share is identified, the decree still needs to address who controls exercise, who advances the strike price if cash is required, who bears withholding, how sale decisions will be communicated, and how the non-employee spouse will receive funds if the plan bars direct transfer.

Those details matter because the spouse receiving a percentage on paper may still face delay, tax confusion, or a lower net recovery if the order does not spell out the mechanics. In other words, the right percentage is necessary, but it is not enough.

Valuation and Timing The Two Biggest Hurdles

A spouse can walk out of mediation feeling good about receiving half the options, then learn years later that the award was never worth what it looked like on paper. That gap between paper value and spendable value causes many of the worst stock option mistakes I see in Texas divorces.

A stock option may be unvested, subject to forfeiture, restricted by the employer’s plan, or so far above the current market price that it has no real present value. The court still has to divide the estate in a just and right manner, but that does not mean every option award should be treated like cash in a bank account.

Valuation is a net-value problem

The first question is not just, "What are these options worth today?" The better question is, "What would each spouse receive after vesting risk, exercise cost, taxes, and sale timing?"

That shift matters. An option with an attractive spread can still produce a disappointing result if exercising it requires substantial cash, triggers withholding, or forces the non-employee spouse to wait on the employee spouse’s decisions. In other cases, a conservative present value may undervalue a grant that is likely to vest soon and can be exercised efficiently.

For that reason, valuation often requires judgment, not a single clean number. Public-company options may support a stronger present-day estimate. Private-company grants usually create more disagreement because transfer limits, liquidity limits, and uncertain future pricing all affect what the award is worth in a divorce settlement.

If your estate also includes ownership interests, deferred compensation, or other hard-to-price assets, this guide to business valuation in Texas divorce explains why assumptions and expert analysis often drive the final result.

Timing changes the economics

Timing is not a side issue. Timing often decides whether a division method is workable.

If the options are vested and the company is public, the parties may be able to estimate value with reasonable confidence and negotiate an offset. If vesting is years away, continued employment is uncertain, or the company is private, a buyout today can turn into a bad trade for one spouse.

I tell clients to focus on three practical timing questions:

- How soon can the award vest or be exercised?

- What must happen before any money can be realized?

- Who bears the risk if the value drops, the employee leaves, or the company never provides liquidity?

Those questions usually matter more than the headline number on the grant statement.

Two workable division methods

Texas divorces usually approach stock options in one of two ways, and each method carries different financial and tax consequences.

Present-day offset

One spouse keeps the options, and the other receives other property now. That might be more cash, a larger share of retirement funds, or more equity in real estate.

This method often works well for couples who need a clean break or expect conflict after divorce. It can also reduce later disputes over notice, exercise timing, brokerage access, and post-divorce tax reporting.

The trade-off is valuation risk. If the options are guessed too high, the employee spouse gives up too much other property. If they are guessed too low, the non-employee spouse leaves value on the table. That problem gets worse when the award is unvested, tied to performance targets, or issued by a private company.

If and when division

Under an if-and-when structure, the employee spouse keeps the award in place under the employer plan, and the non-employee spouse receives the assigned share only if and when the options are exercised or the stock is sold.

This approach often fits cases with limited liquid assets or awards that are too uncertain to price fairly today. It also avoids forcing both sides to pretend they can predict future company value with confidence.

The downside is ongoing entanglement. The spouses may remain tied to each other for years. The non-employee spouse may depend on the employee spouse for account statements, exercise notices, sale details, and tax documents. If the decree does not address those mechanics with precision, enforcement problems are common.

Choosing the better structure

No single method is best in every case. The better choice depends on the company, the award terms, the rest of the marital estate, and the level of trust between the spouses.

A present-day offset is often the better fit when the options can be valued with reasonable confidence, there are enough other assets to balance the division, and the parties want to sever financial ties. An if-and-when division is often the better fit when current value is too speculative, liquidity is tight, or the plan bars transfer and leaves future payment as the only realistic option.

The decision should not stop at ownership percentages. It should address net outcomes. Who fronts the exercise price. How withholding is handled. When notice must be given. What documents must be shared. How long the non-employee spouse has to receive payment after exercise or sale. Those details decide whether the spouse awarded a share will ever receive the value the decree appears to promise.

Practice tip: The best option division is usually the one that produces the most predictable after-tax result with the fewest chances for future dispute.

Calculating the Division A Practical Example

A common Texas divorce problem looks like this. One spouse says, “I got these options before we married, so they are mine.” The other says, “They vested during the marriage, so we split them.” Neither answer is precise enough to settle the case.

Assume Alex received a stock option grant before marriage. The grant vests later. Alex and Jordan are divorcing, and the question is not just who gets what on paper. The core question is how much of the award is separate property, how much falls into the community estate, and whether the eventual payout will match what the decree appears to award.

Example using the Texas time rule

Using the pre-marriage grant example discussed earlier, start with these dates: the options were granted 5 years before marriage, the full grant-to-vesting period is 10 years, the marriage lasted 3 years, and vesting will occur 2 years after divorce.

Under that timeline, the separate property portion is measured by the time outside the marriage that still counts toward earning the award. That means 5 years before marriage plus 2 years from divorce to vesting. The result is 7 out of 10 years, or 70 percent separate property. The remaining 30 percent is community property.

That 30 percent is the part the court can divide in a just and right manner. It does not mean the non-employee spouse automatically receives 30 percent of the total grant. The final share depends on the overall property division, the decree language, and whether the parties use an offset or an if-and-when payout structure.

How I would walk a client through the math

Start with the grant documents, not memory. Confirm the grant date, vesting schedule, number of shares, strike price, and whether the award has multiple tranches. In practice, one grant can require several separate calculations.

Then mark four dates on a timeline:

Grant date: This shows when the award began.

Marriage date: Time before this date may support a separate property claim.

Divorce date: It matters because some awards continue to accrue character after the marriage ends.

Vesting date: The full period from grant to vesting is usually the denominator in the calculation.

Once those dates are pinned down, calculate the portion tied to separate property under the applicable rule. The balance is community property. After that, ask the harder question: what is that community share worth after exercise cost, withholding, and eventual capital gains tax?

That last step is where expensive mistakes happen.

A numbers problem can turn into a cash flow problem

Say the community portion equals 300 options. That still does not tell either spouse what will land in a bank account. If the strike price is high, the employee spouse may need substantial cash to exercise. If the stock is illiquid or subject to blackout periods, there may be no immediate sale to cover that cost. If the decree awards the non-employee spouse a percentage of the options but stays silent on who advances the exercise funds, collection problems start fast.

I have seen settlements that looked fair until the first vesting event arrived. Then the spouses realized they had never agreed on notice, exercise timing, sale timing, or reimbursement. Paper value and usable value are not the same.

Where calculation errors usually start

The formula itself is usually manageable. The evidence causes the dispute.

Common trouble spots include:

Using one vesting date for a multi-tranche award: Each tranche may need its own timeline.

Relying only on pay stubs or equity summaries: Those records often omit the terms that control characterization and payout.

Ignoring modified grants: Refresh grants, repricings, substitutions after a merger, or amended vesting schedules can change the analysis.

Stopping at percentages: A spouse may win a percentage in the decree and still lose value if the order does not address exercise costs, taxes, and payment deadlines.

This short video helps illustrate why timeline facts matter in divorce property questions:

Practice reminder: Get the timeline right, then draft for the actual payout. In stock option cases, a clean formula without clear payment mechanics often leads to post-divorce enforcement work.

Beyond the Formula Tax Burdens and Liquidity Traps

Many people think the hard part ends once the ownership percentage is calculated. It does not.

The legal share and the practical benefit are not the same thing. A decree can award you an interest in options, yet leave you dealing with tax reporting questions, future withholding disputes, or years of waiting for a company event that may never happen on the timeline you expected.

The tax issues many settlements miss

The verified material available here identifies a major gap in many discussions of stock option division. Post-divorce tax mechanics are often overlooked, and poor planning can lead to unexpected capital gains liability. In Texas tech and energy cases with substantial options, that mistake can significantly affect the final result (reference).

The same verified guidance also notes there is minimal source coverage on several important topics:

- how basis rules apply after division,

- tax filing obligations for the non-employee spouse,

- how to structure division to reduce double taxation concerns, and

- how Section 83(b) issues may intersect with community property division.

That means your lawyer and tax professional may need to solve problems that generic divorce articles barely mention.

If you want a general refresher on how gain recognition works after an asset is sold, this overview of capital gains tax can help frame the conversation before you meet with your attorney or CPA.

The non-employee spouse’s blind spot

A non-employee spouse often assumes the employee spouse will “handle the taxes.” That assumption is dangerous.

The employee may control exercise timing, receive the compensation reporting, or be subject to payroll withholding. But if your decree gives you a share of proceeds, you still need to understand:

- when you will be paid,

- whether the payment is gross or net of withholding,

- what records you will receive,

- whether you need year-end tax information, and

- who bears responsibility if the employer reports everything under one spouse’s name.

A decree that skips these details invites a later dispute.

Liquidity can be worse than taxes

Taxes reduce value. Illiquidity can trap it.

If the company is private, the options or resulting shares may not be readily saleable. You may have value on paper and no practical ability to turn that value into cash. That creates pressure when you are trying to refinance a home, pay support, rebuild savings, or move on.

In those cases, I usually see better outcomes when the divorce team addresses liquidity directly instead of treating it as a future problem.

That may mean asking:

- Should one spouse trade away the future equity interest for another asset now?

- If not, what notice rights apply before exercise or sale?

- What happens if the company blocks transfer?

- What if the employee spouse leaves the company and the award is forfeited?

Key takeaway: A strong decree does not just say who gets a share. It says how that share will be tracked, reported, paid, and documented.

What to Do Next Protecting Your Financial Future

You do not need to master securities law to protect yourself in divorce. You do need a disciplined plan.

The right next move is usually not arguing over percentages before you have the documents. It is building a clean record, choosing the right division method, and drafting a decree that is effective in practice.

Start with the paper trail

Gather every document tied to the award.

Your checklist should include:

- Grant notices and award agreements: These identify the grant date and core terms.

- Vesting schedules: You need exact vesting structure, especially if tranches differ.

- Plan documents: Transfer limits and exercise rules often appear here.

- Account statements: Brokerage and compensation portal records help trace exercises and holdings.

- Employment agreements or offer letters: These can explain why the award was issued.

If your spouse has access to an employer equity portal, capture records early and preserve them.

Be precise in the decree

Many otherwise solid settlements break down here. General language does not protect you.

A workable decree should address issues such as:

Characterization language

The decree should identify what portion is separate and what portion belongs to the community estate.Method of division

If there is an offset, spell it out. If payment will occur if and when the award is exercised or paid, define the procedure.Notice obligations

The employee spouse should not be free to exercise, sell, or receive payment without notice if the other spouse has a decree-based interest.Tax handling

The decree should state how withholding, reporting, and reimbursements will be handled.Information sharing

Build in deadlines for producing plan statements, confirmations, and year-end tax documents.

This is especially important in a high-net-worth divorce attorney context, where executive compensation often drives the long-term outcome more than the checking account balance ever will.

Use the full Texas divorce process to your advantage

Stock option cases are easier to handle when you use each phase of the divorce intentionally.

- At filing: Ask early for financial disclosures and preserve records.

- During temporary orders: If needed, address restrictions on hiding, transferring, or exercising assets without notice.

- In discovery: Request the underlying award documents, not just summaries.

- In mediation: Test both a buyout and an if-and-when structure before locking into one path.

- At decree drafting: Treat implementation language as seriously as the property percentages.

- After divorce: Calendar notice dates, vesting dates, and any reporting deadlines immediately.

If children are involved, remember that complex property disputes often affect the rest of the case too. Delays in asset division can shape negotiations around support, possession schedules, mediation timing, and even post-decree enforcement. Related topics such as custody, support, mediation, and enforcement should be part of the larger strategy, not treated as separate silos.

Bring in the right professionals

A family lawyer should not guess at option valuation. A CPA should not draft your decree. Complex equity cases usually need both legal and financial eyes on the same problem.

That can include:

- A forensic accountant: Helpful when valuation is disputed or the award structure is layered.

- A CPA or tax advisor: Important when future exercise, withholding, and reporting may create uneven burdens.

- Your divorce attorney: The person responsible for making sure the legal language matches the financial reality.

What to do next: Do not sign a settlement involving options or RSUs until someone has reviewed the grant documents, vesting terms, payout structure, and likely tax issues together.

You can get through this. The key is not treating stock options like ordinary income or ordinary savings. They are different assets with different risks. When they are handled carefully, you can leave the divorce with clarity, protection, and a much stronger chance of preserving your true net value.

If you are dealing with stock options, RSUs, executive compensation, or other complex property issues in a Texas divorce, the Law Office of Bryan Fagan, PLLC can help you evaluate your options and protect your financial future. You do not have to sort through grant documents, vesting schedules, mediation strategy, and decree language on your own. Schedule a free consultation to get practical guidance specific to your situation.