Skip to content

Skip to content You may be staring at a pension statement right now and thinking, “I worked for this for years. Am I really about to lose half of it?” That fear is real, and in Texas divorce cases, retirement accounts often become one of the most important financial issues you’ll face.

A pension can look abstract on paper, but it often represents your future housing, medical care, monthly cash flow, and peace of mind. If you’re dealing with dividing pension in Texas divorce, the good news is that Texas law gives courts a structured way to sort it out. The process is technical, but it is manageable when you understand the rules and make smart decisions early.

Your Retirement and Your Divorce What You Need to Know

For many people, a pension feels different from other property.

You can split a bank account and see the dollars move. You can sell a house and divide the proceeds. A pension is more personal because it usually took years, sometimes decades, to build. It’s tied to your work history and your plans for later life.

That anxiety tends to hit hardest in long marriages. In so-called gray divorces, rates for people ages 65+ rose from 5% in 1990 to 15% in 2022, and retirement assets often match or exceed the value of the marital home after years of accumulation, according to this discussion of retirement division in gray divorce. The same source notes that divorce costs in Texas average $15,600 for childless couples and $23,500 for couples with children, which makes careful planning even more important.

If you’re sorting through a larger estate, outside financial guidance can help you think beyond the decree and focus on long-term stability. A useful starting point is this Guide to Finance and Divorce for High Net Worth Individuals, especially if your retirement accounts are only one part of a broader asset picture.

Why pensions create so much confusion

Most clients don’t get stuck on the idea of sharing property. They get stuck on how a pension is measured and when payments occur.

Common questions include:

- What part is marital property if you started working before the marriage?

- What happens if you’re not retired yet and no one knows the final monthly benefit?

- Does the divorce decree alone work or is another order needed?

- Should you trade the pension for another asset like home equity or investment accounts?

Practical rule: A pension issue gets easier once you break it into three separate questions. What part is community property, what is it worth, and what order is needed to divide it.

If you want a focused overview of retirement asset issues generally, this resource on dividing retirement accounts in Texas divorce can help you place pensions in the larger property division picture.

The biggest shift in mindset is this. You don’t protect your future by reacting emotionally to the word “split.” You protect it by understanding the numbers, the paperwork, and your settlement options.

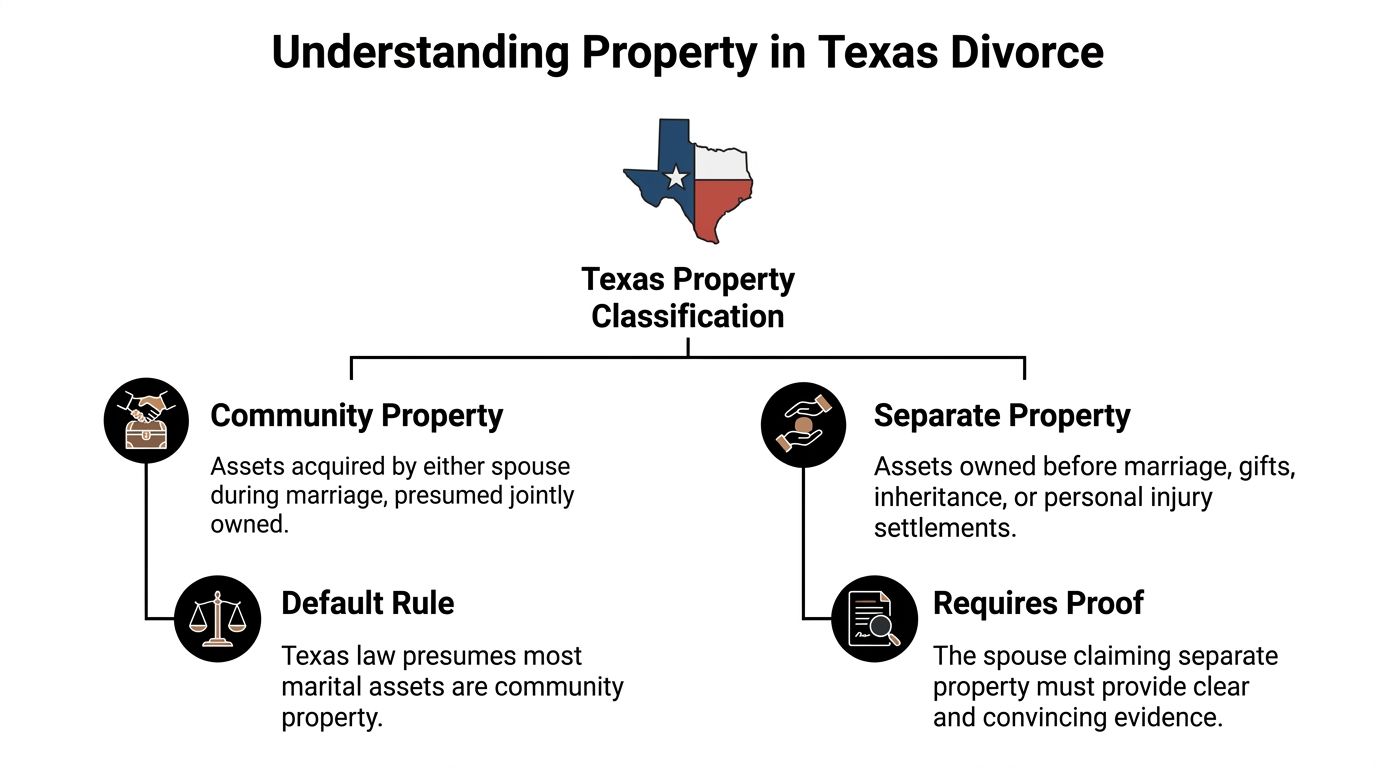

Community vs Separate Property in Texas

Texas treats marriage a little like a shared savings jar.

If either spouse puts earnings into that jar during the marriage, the law starts with the assumption that both spouses have an interest in it. That basic idea drives most property division issues in divorce, including pensions.

What Texas Family Code Section 3.003 means in real life

Under Texas Family Code § 3.003, property possessed during or on dissolution of marriage is presumed to be community property. In plain English, that means the court starts from the position that property connected to the marriage belongs to the marital estate unless someone proves otherwise.

For pensions, that matters a lot. Texas is a community property state, and pensions acquired during marriage are generally presumed to be marital property subject to a “just and right” division, which often results in a 50/50 split of the community portion, as explained in this overview of dividing retirement accounts during a Texas divorce.

That phrase, just and right, is important. It doesn’t automatically mean an exact half of everything. It means the court aims for a fair division under the facts of your case.

Community property in a pension

Think of a pension like a timeline.

Part of that timeline may fall before marriage. Part may fall during marriage. In some cases, work service continues after separation or divorce. The court is usually concerned with the portion earned during the marriage.

Here's a simple way to categorize it:

- Before marriage: This portion may be separate property.

- During marriage: This portion is generally presumed community property.

- After divorce: Future service usually belongs to the employee spouse alone, though the marital portion may still be tied to future payment calculations.

If a pension was entirely earned during the marriage and is worth $500,000, a court may award each spouse $250,000 through a QDRO, according to the same Bastine Law discussion linked above.

Separate property is possible, but you must prove it

Separate property usually includes property owned before marriage, along with certain gifts and inheritances.

That doesn’t mean you can say, “Part of this pension is mine alone.” In Texas, the spouse making that claim must prove it with clear and convincing evidence.

That usually means records. Not guesses. Not memory.

Useful proof may include:

- Employment records showing service dates before marriage

- Plan statements showing account balances at the time of marriage

- Payroll and contribution documents tracing what was earned when

- Gift or inheritance documentation if a retirement asset has an unusual funding history

If you can’t trace it, the court may treat it as community property.

A good example is a $140,000 401(k) that includes $80,000 of premarital separate property. In that situation, only the $60,000 community portion would be divided, often 50/50, resulting in $30,000 to each spouse from the community share, while the owner keeps the separate portion.

Where people get tripped up

People often assume the account title controls ownership. It doesn’t.

If the pension is in your name through your employer, that doesn’t end the analysis. The court looks at when the benefit was earned, not just whose name appears on the plan.

People also assume “fair” means “equal in every line item.” It doesn’t. One spouse might keep more of a retirement asset while the other receives more of another asset to balance the overall result.

How Texas Courts Value Your Pension for Divorce

Once you know some or all of a pension is part of the marital estate, the next problem is valuation. That’s where many smart people feel lost.

A pension isn’t always a pile of cash sitting in an account. Sometimes it’s a promise of monthly income later. That difference affects how lawyers, courts, and plan administrators deal with it.

Two practical ways pensions get divided

Texas divorces usually approach pension division in one of two broad ways.

Present value offset

One spouse keeps the pension. The other receives different property of comparable value.

That offset might involve home equity, brokerage funds, cash, or another retirement account. This approach can simplify life after divorce because the parties don’t remain financially tied to the same pension.

But it comes with risk. If the pension is undervalued, the spouse taking the offset may give up too much. If it is overvalued, the employee spouse may surrender more property than necessary.

Deferred division

Instead of trading the pension away in settlement, the parties divide the benefit when it is eventually paid.

This is common when the pension is not yet in pay status or when a clean present-value calculation is difficult. In that situation, the non-employee spouse receives a defined share later, usually through a court order directed to the plan.

This method can feel less satisfying because it delays closure. Still, it may be the most accurate approach when future retirement benefits depend on years of service, salary, or retirement date.

Berry and Taggart formulas

Texas courts use established formulas to determine the marital portion of pension benefits. The two names you’ll hear most often are Berry and Taggart.

According to Best Lawyers’ discussion of pension division in gray divorce, the Berry formula applies when benefits haven’t started, while the Taggart formula applies when pension payments have already begun. The choice of formula directly affects the final dollar amount each spouse receives.

That timing point matters more than many people realize.

A simple when-then guide

| Situation | Likely approach |

|---|---|

| Benefits have not started | Berry formula is generally used to identify the marital share |

| Benefits are already being paid | Taggart formula is generally used |

| Reliable present value can be established and other assets are available | A negotiated offset may be possible |

| Value is harder to pin down or retirement is years away | Deferred division is often more practical |

Why timing changes the outcome

A pension can increase over time because of continued work, salary history, or plan design. So the date of divorce and the date benefits begin may both matter.

For that reason, valuation often requires careful review of:

- Service years during the marriage

- Whether retirement has already happened

- Plan terms for monthly benefit calculation

- Whether an expert needs to estimate present value

The formula isn’t just math. It determines what part of the pension belongs to the marital estate in the first place.

In higher-asset cases, lawyers often work with actuaries or financial experts to value the pension accurately. That can be especially important if one spouse wants to negotiate an offset instead of waiting for future payments.

The strategic question you should ask

The legal question is “What is the community share?” The financial question is different.

It’s this: What outcome protects your future best?

For some people, regular future income is more valuable than taking another asset today. For others, a clean break is worth more than staying linked to an ex-spouse’s retirement plan for years.

That decision should factor in your age, health, need for liquidity, housing goals, and tolerance for long-term uncertainty.

The Legal Orders Required for Pension Division

A divorce decree can say you are awarded part of a pension. That still may not get money into your hands.

Retirement plans usually need a separate order that tells the plan administrator exactly what to do. If that order is missing, vague, or inconsistent with the decree, problems can follow.

Why the decree usually isn’t enough

A pension plan administrator is not a mind reader. The administrator follows plan rules and written orders.

That means your decree must often be paired with a more detailed implementation order. For many private retirement plans, that order is a Qualified Domestic Relations Order, usually called a QDRO.

A QDRO tells the plan:

- who receives a share,

- what share they receive,

- when payment should happen, and

- how the division should be handled under plan rules.

It also helps avoid tax and distribution problems when retirement benefits are transferred properly.

The basic sequence

This process is easier to manage when you think of it as a checklist instead of a mystery.

Identify the plan correctly

Get the exact plan name and governing documents if possible. A pension, 401(k), teacher plan, military retirement, and federal plan do not all use the same paperwork.Review the decree language carefully

The decree should clearly describe what is being divided. If the decree is sloppy, the later order can become harder to draft or approve.Draft the proper order

For many employer plans, that means a QDRO. For other plans, a different type of order may be required.Seek plan review when appropriate

Many plans have model language or internal review procedures. Using them can reduce rejection risk.Get the judge’s signature

The order becomes enforceable only after the court signs it.Submit the signed order to the plan

This final step is where many people stumble. A signed order sitting in a file cabinet does nothing.

Critical point: Winning the language in the decree is only part of the job. The order must also be entered and accepted by the retirement plan.

A useful comparison by plan type

| Retirement Plan Type | Required Court Order | Key Consideration |

|---|---|---|

| Private pension or 401(k) | QDRO | The order must match plan rules and clearly define the alternate payee’s share |

| Military retirement | A military retirement division order | Federal rules and payment procedures may apply |

| Federal civilian retirement | A court order acceptable for processing | Agency-specific requirements matter |

| Teacher plan such as TRS | A domestic relations order that fits plan requirements | Model forms and administrative rules can control whether the order is workable |

If you want to understand how pension language fits into the final judgment itself, it helps to review the broader role of the decree of divorce.

Why precision matters so much

Retirement orders fail for ordinary reasons. A date is wrong. A formula is unclear. The decree says one thing while the order says another. The plan name is incomplete.

That may sound minor, but pension division is one area where small drafting errors can create very expensive consequences. The verified material for this article notes a 2018 case involving appeals over conflicting decree terms about 50% gross annuity versus the community share. That kind of dispute shows why exact language matters.

TRS also illustrates the point. The Teacher Retirement System of Texas requires model DROs for active employees or retirees since January 1, 2015, to help ensure the order can be administered.

Mediation and timing still matter

Most Texas divorces settle before trial, often through informal negotiation or mediation. That’s often the best time to resolve pension language with care.

If your case involves retirement assets, don’t treat the pension order as an afterthought. Raise these questions early:

- Has the plan’s model language been requested?

- Will the order be drafted before the decree is signed, or after?

- Who is responsible for submission to the plan administrator?

- How will survivor benefits or death issues be addressed?

Those details affect whether your award works in practice, not just on paper.

Navigating Military, Federal, and Private Pensions

The same Texas property principles may apply across many divorces, but pension rules do not look the same from one plan to the next. The plan type changes the paperwork, the review process, and sometimes the payment path.

Private pensions

Private employer pensions and many workplace retirement plans are often the most familiar category in divorce practice.

The main issue is usually making sure the order fits the plan’s terms. One plan may allow certain wording that another rejects. That’s why lawyers often ask for the summary plan description, sample order language, or administrator procedures before finalizing the documents.

For these plans, a QDRO is often the central tool.

Military retirement

Military divorces add a federal layer on top of Texas divorce law. The court may still decide what part of the retirement benefit is marital under Texas principles, but payment and administration are shaped by military-specific rules.

That’s one reason military pension cases deserve close review. Other retirement-related issues can also intersect with service benefits, elections, and post-divorce payment logistics.

If your case involves the armed forces, this overview of military divorce laws in Texas can help you see how pension issues fit into the larger military divorce process.

Federal civilian pensions

Federal pensions are their own category.

A federal employee may participate in a retirement system with agency-specific requirements for dividing benefits. The order used for a private pension may not work here. Timing, survivorship language, and the agency’s processing rules can all affect whether the order is accepted.

In practical terms, federal pension cases reward patience and careful drafting. Small wording differences can change whether the agency treats the order as processable.

Teacher Retirement System of Texas

TRS cases are common in Texas and often misunderstood.

The Teacher Retirement System does not automatically divide benefits because a decree says so. The order must be drafted in a way the system can administer. The verified data for this article notes that TRS has required model DROs since January 1, 2015, for active employees or retirees.

That means form matters. A lot.

A side-by-side way to think about these plans

What stays the same

Across private, military, federal, and teacher pensions, some core truths remain:

- The benefit may include a community portion tied to the marriage.

- The court order must be accurate and usually plan-specific.

- Future income planning matters as much as legal wording.

What changes

The differences usually involve:

- Which order is required

- Who reviews that order

- Whether direct payment is available

- What administrative rules control implementation

A pension division that looks simple in the decree can become complicated once the plan administrator reviews it.

If you’re a business owner, professional, or spouse in a long-term marriage, these plan-specific differences can shape settlement strategy. You may decide to keep the pension division in place, trade it for another asset, or use mediation to negotiate a cleaner overall package.

Key Strategies and Common Mistakes to Avoid

The legal rules matter. Your decisions matter just as much.

Dividing pension in Texas divorce isn’t only about who gets what on paper. It’s about whether the deal you make will still serve you years from now.

Strategy starts with the right question

Don’t ask only, “Can I get part of the pension?”

Ask, “Should I want the pension, or should I negotiate for something else?”

A present-value offset can be attractive if you want a clean break and immediate control over an asset. Deferred division may make more sense if the pension is especially strong and another asset would be a weak substitute.

Neither choice is automatically better. The better choice is the one that fits your real life.

Common mistakes that cost people later

Treating the pension like an afterthought

People spend weeks arguing over the house and leave retirement language for the end. That’s backwards when the pension may be one of the largest assets in the estate.Using vague decree language

If the decree says “half the pension” without clarifying the marital share, payment method, and plan-specific details, you may invite avoidable conflict.Forgetting survivor benefit issues

If you are the non-employee spouse, your future payments may depend on how survivor issues are handled. This point often gets overlooked in settlement talks.Assuming the court order files itself

It doesn’t. Someone must prepare, sign, submit, and confirm implementation.Ignoring the tax and liquidity picture

A pension may have long-term value, but that doesn’t mean it helps with near-term housing, moving costs, or monthly bills.

Bottom line: A pension can be valuable and still be the wrong asset for you to keep.

A more strategic way to prepare

Try to evaluate your options through three lenses:

| Lens | What to ask |

|---|---|

| Cash flow | Will this choice help you meet monthly needs after divorce? |

| Control | Do you want a clean break, or are you comfortable waiting for future payments? |

| Security | If something changes with your ex-spouse’s retirement path, are you protected? |

This is also the point in a case where some people use outside support. That may include a financial planner, an actuary, a mediator, or a law firm that handles retirement-order drafting and plan communication. The Law Office of Bryan Fagan, PLLC is one example of a Texas family law practice that assists with retirement asset division and QDRO-related work in divorce matters.

The bigger lesson is simple. Don’t negotiate a pension based on fear, pride, or guesses. Negotiate it based on a plan.

What To Do Next Protecting Your Future

A pension issue can feel overwhelming because it combines law, math, procedure, and emotion all at once. But the path forward is usually clearer once you focus on the right steps.

Key takeaway

Keep these points in front of you:

- Texas starts with a community property presumption for property tied to the marriage.

- Only the community portion of a pension is subject to division.

- Valuation method matters, especially if benefits have or haven’t started.

- The decree alone may not be enough. A separate retirement order is often required.

- Your long-term security should shape your settlement choices, not just the desire to “win” one asset.

If children are involved, remember that retirement issues are only one part of the divorce. Custody, support, possession schedules, mediation, and enforcement can all affect your overall plan. A workable divorce strategy looks at the whole picture, not just one account statement.

What to do next

Start gathering documents now.

Collect plan statements, employment records, beneficiary information, and any documents that show what existed before marriage. If mediation is coming up, make sure pension questions are on your issue list well before the final session.

You don’t have to figure this out alone. A careful review of your pension, the decree language, and the required retirement order can protect you from mistakes that are hard to fix later.

If you’re facing divorce and need guidance on dividing pension in Texas divorce, you can schedule a free consultation with Law Office of Bryan Fagan, PLLC. A focused consultation can help you understand your rights, identify the community and separate portions of retirement assets, and build a practical plan for your future.