Skip to content

Skip to content Going through a divorce feels like untangling a thousand different threads, and one of the most knotted ones is often your retirement savings. When you’re dividing retirement accounts in a Texas divorce, the law starts with a simple presumption: anything earned or grown during the marriage is community property. That means it’s subject to a "just and right" division, no matter whose name is on the paperwork. This guide will help you understand what that really means for your future and empower you to take control.

Your Guide to a Secure Financial Future After Divorce

You’ve likely spent years, maybe decades, carefully building that 401(k) or IRA. The thought of it being split can be terrifying. But uncertainty is the enemy of good decision-making. Our goal here is to replace that anxiety with knowledge, so you can confidently protect your long-term financial stability.

Understanding Texas Community Property

The entire framework for dividing assets in a Texas divorce rests on the Texas Family Code and its distinction between "separate" and "community" property. This concept is absolutely critical when it comes to your retirement accounts.

Separate Property: This is anything you owned before the marriage. It can also include specific gifts or inheritances you received during the marriage. For a retirement account, the balance on your wedding day is typically your separate property—but the burden is on you to prove it with clear, convincing evidence.

Community Property: This bucket includes all assets acquired by you or your spouse from the date of marriage until the date of divorce. When we talk about retirement accounts, this means every contribution, employer match, and bit of investment growth that happened during the marriage is part of the community estate.

A huge misconception we see all the time is the belief that an account is safe just because it’s only in your name. In Texas, that’s flat-out wrong. The law cares about when the money was earned, not whose name is on the statement.

Why This Matters for Your Retirement

Failing to properly classify your retirement funds can be a devastatingly expensive mistake. If you can’t trace the separate property portion of your account—meaning you don’t have the pre-marriage statements to prove its value—a court may treat the entire account as community property. This could lead to you unintentionally giving up a huge chunk of your pre-marital savings.

At The Law Office of Bryan Fagan, PLLC, we’ve guided countless Texas families through these exact complexities. We cut through the legal jargon and explain how the law applies to your specific accounts, so you can walk into negotiations prepared. Understanding these fundamental rules is the first step toward rebuilding your finances after divorce.

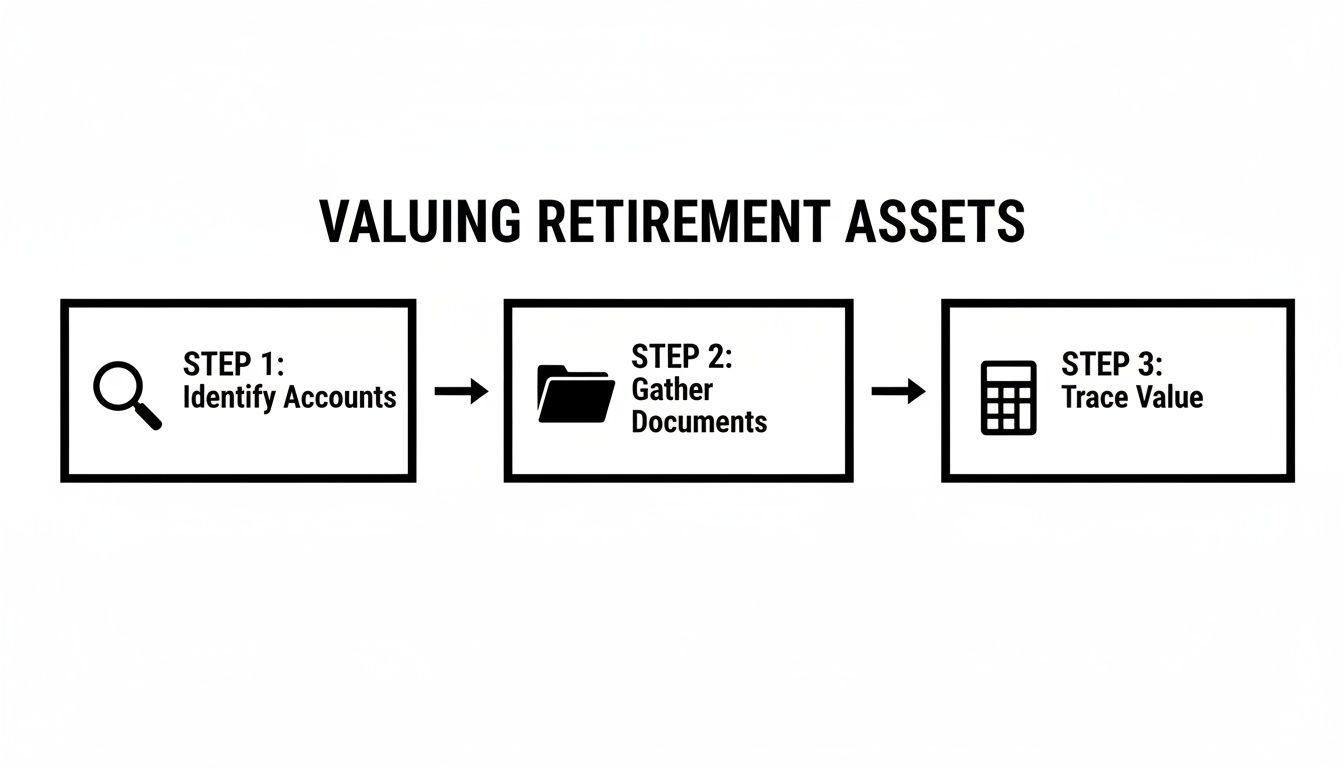

Identifying and Valuing Every Retirement Asset

Before a single dollar from a retirement account can be divided in a Texas divorce, you have to know exactly what you're working with. This first, crucial step involves creating a complete inventory of every retirement asset and figuring out its value. It's the foundation for your entire financial settlement, so getting it right is non-negotiable.

This isn’t a one-sided task. Both you and your spouse are required to disclose a full list of all retirement benefits. And we're not just talking about the obvious 401(k). Many other valuable, and often overlooked, plans need to be on the table.

Building a Complete Inventory

The first goal is simple: list every retirement-related asset that exists, no matter whose name is on the account. A truly thorough inventory will track down everything.

This includes common accounts like:

- Defined Contribution Plans: Think 401(k)s, 403(b)s, and 457 plans.

- Individual Retirement Accounts (IRAs): This covers Traditional, Roth, SEP, and SIMPLE IRAs.

- Defined Benefit Plans (Pensions): These are promises of future monthly income, often from government or long-standing corporate jobs.

- Military Retirement: A specialized asset with its own complex division rules.

- Executive Compensation Plans: Don’t forget about stock options, restricted stock units (RSUs), or other deferred pay that acts like a retirement fund.

Getting the statements and plan documents for these accounts is an absolute must. This usually happens during the formal discovery phase of a divorce, a legal process where spouses are compelled to exchange all financial information. You can get a deeper understanding of what this involves by reading our guide on the discovery process in a Texas divorce.

The Critical Process of Tracing

Once you have a full list of accounts, the real work begins. We call it "tracing." In legal terms, this means proving what portion of an account is separate property (assets you owned before the wedding) and what part is community property (everything earned or grown during the marriage).

To do this, you’ll need to hunt down very specific documents:

- Account statements from the date of marriage: This is your proof of the starting balance that belongs to you alone.

- Account statements from the date you separated or filed for divorce: This helps establish the end-date for community property accumulation.

- A complete history of statements, if you can get them, to show a clear record of contributions and market growth over the years.

If you can't clearly prove what was yours before the marriage, a Texas court may presume the entire account is community property, and therefore divisible.

According to the Texas Family Code, any contributions made during the marriage—plus employer matches and investment growth on those contributions—are considered community property. Your premarital balance, however, remains your separate property. For example, if you entered the marriage with a $50,000 401(k) and another $250,000 was added while you were married, the court won't just split the $250,000. It will apply a specific formula to allocate the investment growth proportionally between the separate and community shares. This math gets complicated fast, which is why an attorney who gets these nuances is so critical.

When to Bring in a Forensic Accountant

Sometimes, tracing isn't a simple A-to-B exercise. What if funds were shuffled between different accounts? Or an account was cashed out years ago? What if you just have a gut feeling your spouse isn't telling the whole truth? This is when you may need a forensic accountant.

These financial detectives are experts at piecing together complex money trails. They can trace commingled funds, uncover hidden assets, and give you a professional valuation that will stand up in court. Their expertise is especially vital for business owners, high-net-worth couples, or anyone dealing with pensions or the unique rules for government employee benefits. For example, correctly valuing a federal pension requires an understanding of specific federal retirement calculations that a specialized expert can provide.

The Mechanics of Splitting Different Retirement Accounts

Trying to figure out how to split a 401(k) or a pension can feel overwhelming, especially with your financial future on the line. The good news is that the process isn't a mystery—it's highly structured. The critical thing to understand is that the legal tool used to divide a 401(k) is completely different from the one used for an IRA.

Getting this wrong can lead to serious financial mistakes. Getting it right starts with a solid foundation of information.

The first step is always identifying every single plan and gathering the right documents to trace its value.

Dividing 401(k)s and Pensions with a QDRO

When it comes to employer-sponsored plans like 401(k)s, 403(b)s, and traditional pensions, you absolutely must have a special court order called a Qualified Domestic Relations Order (QDRO). This is arguably the single most important document for splitting these kinds of retirement funds.

A QDRO is a separate legal order, signed by the judge after your divorce is finalized. It’s a direct instruction to the plan administrator explaining exactly how to divide the account.

It’s a massive mistake to assume your Final Decree of Divorce is enough to get the job done. It's not. Plan administrators are legally barred from touching an employee’s retirement account without a valid QDRO that meets both federal law and their own internal requirements.

Here is a step-by-step breakdown of how a QDRO works:

- Negotiation: You and your spouse agree on a percentage or dollar amount of the community portion of the retirement account to be divided. This is finalized in your divorce decree.

- Drafting: After the divorce, an attorney drafts the QDRO with specific language that the retirement plan requires.

- Approval: The draft is sent to the plan administrator for pre-approval.

- Court Order: Once approved, the QDRO is signed by the judge, making it a legal order.

- Execution: The signed order is sent back to the plan administrator, who then creates a separate account for the non-employee spouse, allowing them to roll the funds over without penalty.

A properly executed QDRO is the only way to divide these plans without triggering devastating taxes and penalties. Without it, the transfer is treated as an early withdrawal, which can have massive financial consequences. A distribution from a 401(k) without a QDRO can trigger a 10% early withdrawal penalty if you're under 59½, on top of ordinary income taxes. On a $150,000 transfer, that could easily cost you $45,000 or more—money that a QDRO would have protected.

How IRAs Are Divided

Individual Retirement Accounts (IRAs), both Traditional and Roth, are much simpler to divide. They do not require a QDRO. Instead, the division is handled through what’s called a "transfer incident to divorce."

For this to work, your Final Decree of Divorce must include specific language ordering the IRA custodian—the bank or financial firm holding the account—to transfer a certain dollar amount or percentage of the assets to an IRA in your ex-spouse's name.

The process boils down to two key steps:

- Clear Language in the Decree: Your divorce decree needs to be crystal clear about the amount to be transferred and include all necessary account details.

- Direct Trustee-to-Trustee Transfer: The funds must move directly from one IRA to another. Never withdraw the cash yourself to give to your ex-spouse, as this is a taxable event and will trigger penalties.

While this method is more straightforward, the wording in your legal documents has to be precise to make sure the financial institution processes the transfer as a non-taxable event.

The Unique Rules for Military Retirement

Dividing military retirement pay is its own unique world, governed by a federal law known as the Uniformed Services Former Spouses' Protection Act (USFSPA). Just like with a 401(k), this division requires a specific order that is separate from your divorce decree, often called a Military Pension Division Order (MPDO).

A few key points to remember are:

- The 10/10 Rule: The Defense Finance and Accounting Service (DFAS) will only make direct payments to a former spouse if the marriage lasted at least 10 years and those 10 years overlapped with at least 10 years of creditable military service.

- Disposable Retired Pay: The law only permits the division of "disposable retired pay." This is the gross pay minus certain deductions, like any pay the service member waived to receive VA disability benefits.

If you don't meet the 10/10 rule, it doesn't mean the former spouse gets nothing. It just means DFAS won't be the one cutting the check. The service member will be responsible for paying their ex-spouse directly. Given these nuances, our guide on dividing a 401(k) and other retirement plans offers more context that you may find helpful.

How Different Retirement Accounts Are Divided in a Texas Divorce

| Account Type | Division Method | Key Legal Document | Primary Consideration |

|---|---|---|---|

| 401(k) / 403(b) | Segregation into a separate account for the non-employee spouse. | Qualified Domestic Relations Order (QDRO) | Avoiding taxes and penalties through a proper QDRO is critical. |

| Traditional Pension | A portion of future benefit payments is assigned to the non-employee spouse. | Qualified Domestic Relations Order (QDRO) | The valuation can be complex, often requiring an actuary. |

| IRA (Traditional/Roth) | A tax-free "transfer incident to divorce" to the other spouse's IRA. | Final Decree of Divorce | The language in the decree must be precise to avoid a taxable event. |

| Military Retirement | A portion of disposable retired pay is paid to the former spouse. | Military Pension Division Order (MPDO) | The USFSPA and the "10/10 Rule" govern direct payments from DFAS. |

Each of these division methods requires careful attention to detail and a deep understanding of the law. A mistake with a QDRO or a poorly worded decree can have financial consequences that last for years.

Strategic Negotiations and Common Financial Pitfalls

Dividing retirement funds isn't just a math problem—it’s one of the most significant negotiations you’ll face in your divorce. The decisions made here will ripple for decades, impacting your long-term security far more than who gets the living room furniture.

Going into these discussions with a clear head and a solid strategy is absolutely essential for protecting your financial future.

Whether you’re in a formal mediation or working things out through your attorneys, the goal is to land a settlement that is genuinely fair and sustainable for you.

Thinking Beyond the 50/50 Split

While Texas law starts with a "just and right" division, that doesn't automatically mean every single asset gets sliced down the middle. A divorce is a comprehensive negotiation, and this is where you can get creative to find solutions that actually work for your life.

One of the most common trade-offs we see involves the family home versus retirement accounts. For instance, one spouse may feel a deep emotional attachment to the marital residence and want to stay, especially if children are involved.

- Scenario: You might offer to give up your share of the community interest in your spouse's 401(k) in exchange for their equity in the family home.

On the surface, this can feel like a clean, simple solution. But you absolutely must analyze the true value of what you’re giving up versus what you’re getting. A dollar in home equity is not the same as a dollar in a pre-tax retirement account.

The Dangers of Asset-Swapping Without a Plan

Trading big assets like the house for a 401(k) can be a powerful negotiation tool, but it's also loaded with financial traps if you aren't careful. The biggest issues are liquidity and taxes.

- Home Equity: The equity in your home isn't cash in your pocket. To access it, you have to sell the house or take out a loan. You also take on all the financial burdens alone: the mortgage, property taxes, insurance, and all the surprise maintenance costs.

- Retirement Funds: A 401(k) or traditional IRA is funded with pre-tax dollars. When you eventually withdraw that money in retirement, you will owe income tax on every single dollar. That $100,000 you see on a statement is not $100,000 in your pocket.

Let's say you trade your $100,000 community interest in a 401(k) for $100,000 of home equity. Down the road, those retirement funds could have a tax liability of $20,000 or more, while the home equity comes without that immediate tax hit. Any fair trade has to account for these future tax consequences.

Common and Costly Financial Pitfalls to Avoid

In our years of helping Texas families navigate divorce, we see the same painful and expensive mistakes happen over and over again. Just being aware of these pitfalls is the first step to making sure you don't fall into them.

Forgetting to Update Beneficiaries: This is a tragically common and devastating error. Your divorce decree does not automatically remove your ex-spouse as the beneficiary on your 401(k) or life insurance policy. If you were to pass away before updating this separate paperwork, your ex—not your children or new partner—could inherit the entire account.

Failing to Finalize the QDRO: So many people sign their divorce decree and assume the retirement division is done. It's not. The Qualified Domestic Relations Order (QDRO) is a separate, post-divorce legal order that must be drafted, signed by the judge, and then approved by the retirement plan administrator. Waiting years to do this can make the process incredibly difficult, and in some cases, even impossible.

Cashing Out an Account to "Settle Up": Never, ever just withdraw funds from your 401(k) to write a check to your spouse. This is considered an early distribution. If you are under 59½, you will face a 10% federal penalty on top of paying ordinary income tax on the full amount. This one mistake can cost you tens of thousands of dollars that a proper QDRO would have easily avoided.

One of the most critical aspects of a successful settlement is understanding the long-term implications of your choices. A decision that seems easy today, like giving up your claim to a pension to avoid a fight, could leave you financially vulnerable in retirement. We help you see the full picture.

The complexities of dividing retirement accounts in a Texas divorce require both legal knowledge and financial foresight. If you're facing these negotiations, you don't have to do it alone. The team at The Law Office of Bryan Fagan, PLLC, is here to provide the compassionate, authoritative guidance you need to avoid these pitfalls and secure a settlement that truly protects you.

Your Post-Divorce Action Plan for Finalizing the Division

The moment the judge signs your Final Decree of Divorce brings a wave of relief, but when it comes to retirement accounts, it’s really just the starting line. Think of your decree as the instruction manual; now you have to actually build the thing. This is where your post-divorce action plan becomes critical to making sure every dollar you were awarded actually makes it into your name.

This is the phase where small oversights can lead to major delays or, worse yet, lost funds. Following a clear, systematic process ensures the careful negotiations you just went through translate into real-world financial security. This is not the time to take your foot off the gas.

The Immediate Priority: Getting the QDRO Right

If your divorce settlement includes a 401(k), pension, or another employer-sponsored plan, your most urgent task is finalizing the Qualified Domestic Relations Order (QDRO). Your divorce decree gives you the right to a portion of the funds, but the QDRO is the legal instrument that actually moves them.

The process involves a few non-negotiable steps:

- Drafting the Order: Your attorney or a QDRO specialist will draft the order based on the exact terms in your divorce decree. It must contain very specific language required by both federal law and the retirement plan administrator’s own internal rules.

- Approval by the Plan: Before it ever sees a judge, the draft QDRO is often sent to the plan administrator for pre-approval. This step is crucial because it confirms the plan will accept the order as written, preventing a frustrating rejection later.

- Getting the Judge’s Signature: Once pre-approved, the QDRO is submitted to the court for the judge's signature, making it an official, enforceable court order.

- Final Submission to the Plan: The signed, certified order is then sent back to the plan administrator for final processing and implementation.

The timeline for a QDRO to be fully processed can be surprisingly long, often taking several months after the divorce is final. This isn't a failure of the process; it's simply the reality of coordinating between law firms, courts, and large corporate plan administrators. Staying proactive is key.

Implementing the Division and Following Up

Once the plan administrator accepts the signed QDRO, they will begin the process of segregating your awarded funds. For a 401(k), this usually means they will create a new account in your name holding your share of the assets. You are now officially in control of that money.

From there, your focus shifts to managing your newly acquired asset.

- Set Up a Rollover IRA: Your best move is almost always to execute a direct rollover of the funds from the plan into a new IRA that you control. This move gives you full authority over investment choices and, importantly, avoids any immediate tax consequences.

- Confirm the Transfer: Don’t just assume the money has moved. You need to follow up with both the 401(k) plan administrator and your new IRA custodian to confirm that the transfer is complete and the funds are properly invested.

- Choose Your Investments: The money will likely land in a low-risk cash or money market fund by default. It’s up to you to act. Work with a financial advisor to create an investment strategy that aligns with your long-term goals and risk tolerance.

Updating Your Own Financial Life

With your share of the retirement assets secured, the final piece of the puzzle is updating your personal financial and estate planning documents. This step is all about protecting your assets for your own future and ensuring they go to your intended heirs, reflecting your new, single status.

Your post-divorce financial checklist should include:

- Updating Beneficiaries: Immediately change the beneficiary designations on your new rollover IRA, any life insurance policies you own, and any other financial accounts. You don't want your ex-spouse to remain the default recipient.

- Creating a New Will: Your old will is likely invalid or, at the very least, completely outdated. You need a new will and other estate planning documents (like a power of attorney) that name the people you now want to inherit your assets and make decisions on your behalf if you're unable.

By methodically working through this action plan, you ensure there are no loose ends. You fought hard for a fair division during your divorce; now is the time to secure that victory and start building your new financial foundation.

Frequently Asked Questions About Texas Retirement Division

Even after you get a handle on the basics of splitting retirement accounts in a Texas divorce, it's the specific "what if" questions that can keep you up at night. Every family's financial situation is different, and those small details often feel like major roadblocks. Let's walk through some of the most common questions we hear from clients and get you the practical answers you need.

What Happens to the 401(k) Loan My Spouse Took Out?

This is a scenario we see all the time. One spouse takes out a loan against their 401(k) during the marriage, and now that it’s time to divorce, that outstanding balance throws a wrench in the works. How does Texas law untangle this?

Simply put, a loan taken from a community property retirement account during the marriage is almost always considered a community debt. That means the debt belongs to both of you, not just the spouse whose name is on the 401(k).

When the account is valued for division, the outstanding loan amount is usually added back to the account’s total value before calculating the split. Then, the loan itself is listed as a community debt to be divided between you. For instance, if the account holds $80,000 and has a $20,000 outstanding loan, the community estate really has a $100,000 asset and a $20,000 liability. This keeps one spouse from being unfairly stuck with a loan that likely benefited you both.

Can I Keep My 401(k) if I Give My Spouse the House?

This is one of the most popular trade-offs people propose in divorce negotiations—swapping one big asset for another to create a "clean break." You might offer to keep your entire 401(k) if your spouse gets all the equity in the family home. While this can work, it's a deal you have to approach with extreme caution.

The biggest issue is that a dollar in home equity is not the same as a dollar in a pre-tax retirement account. They are fundamentally different assets.

- Tax Consequences: The money in a traditional 401(k) is all pre-tax. You haven't paid a dime of income tax on it yet, and you will when you start making withdrawals in retirement. Home equity, on the other hand, is post-tax money.

- Liquidity and Access: Getting cash out of your home means selling it or taking out a new loan, which comes with its own costs and hurdles. A 401(k) is a liquid financial asset, even if access is restricted before retirement age.

A fair trade has to account for these differences. Simply swapping a $150,000 401(k) for $150,000 in home equity is not an equal exchange. That 401(k) carries a significant future tax liability, meaning its real, after-tax value is much lower than what the statement says.

To make sense of these complex valuations, working with a financial expert is often the smartest move. There are resources available to find local financial professionals in Texas who can help you understand the true value of what you're trading.

How Long Does It Take for a QDRO to Be Finalized?

When it comes to a Qualified Domestic Relations Order (QDRO), you'll need to have some patience. A lot of people are surprised to learn that the process doesn’t end the day the judge signs the divorce decree. In reality, getting a QDRO fully processed can take several months.

The timeline is a multi-step journey, and each stage has its own potential for delays:

- Drafting: First, an attorney or a QDRO specialist has to draft the order to match the terms of your divorce decree.

- Plan Administrator Pre-Approval: The draft is then sent to the retirement plan administrator for review. They need to make sure it meets their very specific internal requirements. This step alone can take weeks, sometimes months.

- Getting the Judge's Signature: Once the plan administrator gives the thumbs-up, the QDRO goes to the judge to be signed and entered as a formal court order.

- Final Implementation: The signed, certified order is sent back to the plan administrator, who finally processes the transfer and moves the funds into a new account for the receiving spouse.

This is a methodical process that demands careful follow-up. Don't just assume it’s done. You'll want to stay on top of it until you get written confirmation that the funds have officially been divided and moved into an account in your name.

What to Do Next: Secure Your Financial Future

A fair and accurate division of retirement assets is essential for securing your financial independence. We're here to provide the compassionate, authoritative guidance you need to make the best decisions for your future.

Your job right now is to start gathering paperwork. Create a dedicated folder—whether it’s on your computer or a physical file—and start collecting statements for every single retirement account you and your spouse have. The better organized you are from the start, the smoother and less expensive this process will be.

Don't make the mistake of assuming an account is "yours" just because your name is on it. In Texas, when the money was put in is what really matters.

At The Law Office of Bryan Fagan, PLLC, we know this can feel like an impossible mountain to climb. We’re here to give you a clear strategy, make sure every dollar is accounted for, and protect your financial future. If you're ready to get started, contact us today for a free, no-obligation consultation with one of our experienced Texas divorce attorneys.