Skip to content

Skip to content Going through a divorce is overwhelming enough without the added stress of figuring out what happens to your debt.

In Texas, the law provides a clear framework for untangling your finances, but the process can still feel confusing and isolating. You are not alone in feeling this way. Understanding how Texas law treats your financial obligations is the first step toward regaining control and moving forward with confidence. This guide will provide you with the practical, step-by-step information you need to protect yourself.

Understanding Community vs. Separate Debt in a Texas Divorce

When you are facing a divorce, one of the most pressing questions is, "What happens to all our debt?" To answer that, you first need to understand how Texas law classifies every dollar you and your spouse owe. In Texas, all liabilities fall into one of two categories: community debt or separate debt.

Texas is a community property state. As explained in Texas Family Code § 3.002, property possessed by either spouse during or on dissolution of marriage is presumed to be community property. The simplest way to think about this is that your marriage is a financial partnership. Most debts taken on by either you or your spouse from the day you said "I do" until the day of your divorce are presumed to belong to this partnership. It doesn't matter whose name is on the loan or who used the credit card; if the debt was acquired while you were married, a Texas court will almost always view it as community debt.

The Core Difference: Community vs. Separate

The primary exception to the community property rule is separate debt. According to Texas Family Code § 3.001, separate property includes assets owned before marriage or acquired during marriage by gift or inheritance. This same principle applies to debt. A liability you brought into the marriage—like a student loan from your college days—is your separate debt.

A car loan you took out a year before getting married is a classic example of separate debt. Conversely, the mortgage you both signed to buy your family home is a textbook community debt. This distinction is the bedrock of how a Texas court will divide your liabilities in a "just and right" manner.

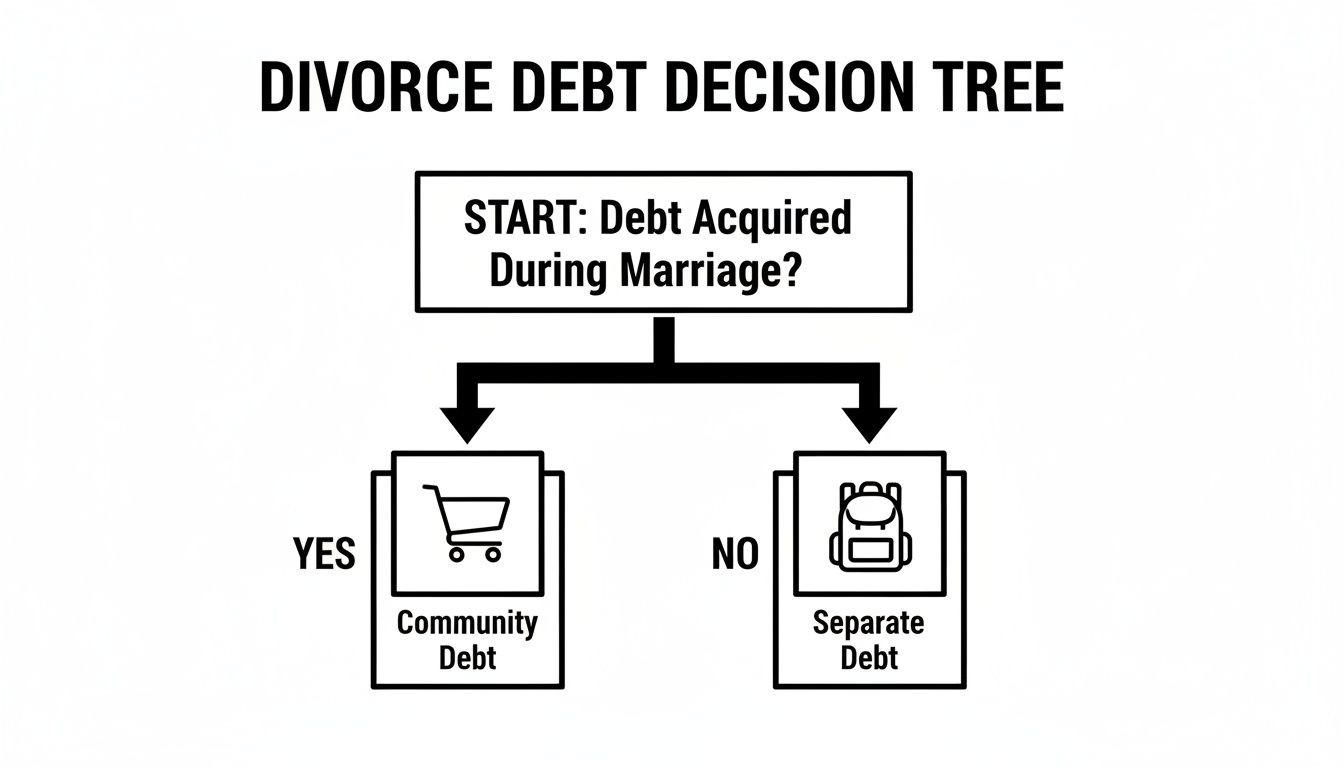

This decision tree helps visualize how the timing of a debt is the most important factor in its classification.

The takeaway here is simple but crucial: the date a debt was first taken on is almost always the deciding factor.

The "Inception of Title" Rule in Texas

To determine when a debt legally began, Texas courts use a principle called the "inception of title" rule. This rule pinpoints the exact moment a right to property or a liability was created, which classifies it as either separate or community.

For example, imagine you signed a contract for a business loan the week before your wedding. Even if you made every payment from a joint checking account during your marriage, that debt is likely still your separate property. Why? Because the "inception of title"—the moment the debt legally came into existence—happened before your marriage community was formed.

A Note on Commingling: Things get complicated when you use community funds (like your paychecks) to pay down a separate debt. This is called "commingling," and it can blur the lines. If you cannot clearly trace the funds, you may inadvertently give the community an interest in what was once your separate debt. This is why keeping meticulous financial records is absolutely essential for business owners and individuals with significant separate assets.

How to Prove a Debt Is Separate Property

The law begins with a powerful presumption: any debt existing at the time of divorce is a community debt. If you believe a specific debt belongs solely to you, the burden is on you to prove it. The standard of proof is high—you must provide "clear and convincing evidence."

This means you need solid documentation to show that:

- The debt existed before your date of marriage.

- The debt was directly tied to a gift or inheritance received only by you.

- The debt can be traced back to one of your separate property assets.

Gathering old loan agreements, bank statements, and other financial records from before your marriage is a critical step in preparing for your divorce. You can learn more about this legal framework in our detailed guide on separate property vs. community property in Texas. Protecting what's yours—and proving which debts are yours alone—demands a solid legal strategy backed by clear evidence.

How Common Types of Debt Are Divided in Texas

Untangling your finances is often one of the most difficult parts of a divorce. When you're trying to figure out who is responsible for the mortgage, car loans, and credit card bills, it's easy to feel overwhelmed. Once you have a clear grasp of the difference between community and separate debt, you can begin to see how a Texas court will likely handle your financial situation.

Let's walk through some of the most common types of debt we help our clients navigate.

Mortgages and Home Equity Loans

For most Texas families, the house is not only the biggest asset—the mortgage is also the largest single debt. Because it was almost certainly taken out during the marriage, the mortgage is a community debt. This leaves you with a few primary options for your divorce procedure:

- Sell the House: This is often the cleanest solution. Many couples sell the home, use the proceeds to pay off the mortgage and any home equity loans (HELOCs), and then divide the remaining profit according to their settlement or court order.

- One Spouse Keeps the House: If you or your spouse wish to remain in the home, the person keeping it will typically be required to refinance the mortgage into their name alone. This is a crucial step that removes the other spouse from the loan, protecting their credit and freeing them from future liability. This process can be started even before the final decree is signed.

- "Owelty" Lien or Buyout: If refinancing isn't immediately possible, one spouse can "buy out" the other's share of the home's equity over time. This agreement is secured with a formal lien on the property, ensuring the spouse who moves out is paid their fair share. This is a common strategy in mediation.

One of the biggest mistakes you can make is assuming your divorce decree is the final word for your lender. If the judge orders your ex to pay the mortgage but your name is still on the original loan, the bank can—and will—come after you if a payment is missed. To see what's involved in getting your name off the loan, you can read our guide on assuming a mortgage after a divorce.

Credit Card Debt

In Texas, any credit card debt accumulated during the marriage is generally considered community debt. This is true even if the card was in only one spouse's name.

A common point of confusion is the difference between being an "authorized user" versus a joint account holder. If you are only an authorized user, you are not legally responsible for the debt with the credit card company. However, the account's payment history can still impact your credit score, so getting your name removed from those cards is a vital, protective step.

Auto Loans

Just like a mortgage, a car loan taken out while you were married is a community debt. The division of this debt almost always follows the vehicle itself. The spouse who is awarded the car in the divorce will also be assigned the associated loan.

Ideally, the person keeping the car should refinance the loan in their name only as part of the divorce process. This creates a clean financial separation and shields the other spouse's credit from any late or missed payments in the future.

Student Loans

Student loans can be more complex, and the classification depends entirely on timing.

- Loans from Before Marriage: If you or your spouse brought student loan debt into the marriage, it is almost always treated as separate debt. The person who took out the loan is responsible for paying it back.

- Loans During Marriage: This is where it gets tricky. If a loan was taken out during the marriage to pay for one spouse's education, a court will often view it as a community debt. The reasoning is that the entire "community" was expected to benefit from the higher earning potential that degree would provide. A judge will evaluate all the facts to determine what is fair and just.

Business and Tax Debts

If you and your spouse own a business, untangling its finances requires specialized expertise. Any business loans, lines of credit, or other liabilities acquired during the marriage are typically community debts, especially if the business was a primary source of family income. Properly dividing these debts begins with a thorough business valuation to get an accurate picture of the company's assets and liabilities.

The same principle applies to tax debt. If you filed joint tax returns, any unpaid taxes owed to the IRS are the responsibility of both of you. Your divorce decree does not bind the IRS—they can collect the full amount from either spouse. It is absolutely critical to address tax debt directly in your divorce settlement to prevent serious financial and legal trouble later on.

Steps to Protect Your Financial Health During Divorce

It’s natural to feel overwhelmed by debt and an uncertain financial future during a divorce. But this is precisely the moment to take control. By taking deliberate, strategic steps, you can protect your financial health and build a solid foundation for your new life.

Step 1: Uncover the Full Financial Picture

You cannot protect yourself from debts you don't know exist. Your first step, even before filing for divorce, is to get a complete inventory of every liability in your name, your spouse's name, and held jointly. The most effective way to do this is to pull a comprehensive credit report for both of you.

This report will show you:

- Mortgages and home equity lines of credit (HELOCs).

- Car loans.

- Joint credit cards and any accounts where you are listed as an authorized user.

- Personal loans or lines of credit.

- Student loans.

Review every single line item. If you see an account you don't recognize, consider it a red flag that requires immediate investigation with your attorney. This discovery process is the foundation of your entire financial strategy.

Step 2: Separate Your Financial Identities

Once you have a complete list of all debts, it's time to begin separating your finances. This process is crucial for limiting your exposure to new debt your spouse might accumulate and for establishing your own independent financial footing.

- Close Joint Accounts: The best option for joint credit cards is to pay them off and close them completely. If a balance prevents you from closing an account, contact the creditor to freeze it to prevent new charges and ask to have your name removed.

- Open New Accounts: Open new checking, savings, and credit card accounts in your name only. Begin directing your income into these accounts and using them for your personal expenses. This creates a clear financial trail that is invaluable during property division negotiations.

Critical Warning: Your divorce decree does not override your original agreement with a lender. If the final decree orders your spouse to pay off a joint car loan but your name is still on the loan agreement, the creditor can—and will—come after you if your ex defaults. Your credit score will suffer, and you could even face a lawsuit. The only way to fully protect yourself is to ensure the debt is refinanced.

Step 3: Your Financial Protection Checklist

As you move through the divorce process, from filing to the final decree, taking proactive steps can protect your credit and finances.

| Action Step | Why It's Important | When to Do It |

|---|---|---|

| Pull Credit Reports | Creates a complete inventory of all debts and can uncover hidden liabilities. | Immediately, when divorce is first considered. |

| Close or Freeze Joint Accounts | Prevents your spouse from running up new debt for which you could be held liable. | As soon as possible, after documenting balances. |

| Open Individual Accounts | Establishes your financial independence and creates a clear separation of finances. | Immediately, when you decide to separate. |

| Notify Creditors in Writing | Informs them of your separation and opens a line of communication about potential options. | After filing for divorce, or once you have a clear plan. |

| Consult a Family Law Attorney | Ensures any settlement you agree to is fair, enforceable, and protects your long-term interests. | Before signing any agreement or final decree. |

Taking these steps provides a strong defense for your financial future and gives you more control over the outcome.

Step 4: Communicate and Negotiate Strategically

Being upfront with creditors about your divorce can often lead to better outcomes. Informing them in writing that you are separating may make them more willing to work with you on payment plans or offer temporary solutions.

This is also where smart negotiation in mediation comes into play. To navigate the financial complexities of divorce, understanding and implementing effective debt management strategies is a critical step in protecting your financial health. Instead of leaving these major decisions to a judge, mediation allows you and your spouse to craft creative solutions that work for your specific situation. For example, you could agree to sell an asset to pay off a high-interest credit card, or one spouse could take on more debt in exchange for keeping an asset of equivalent value. This approach gives you far more control.

Because these financial decisions will impact you for years, we strongly advise consulting with an experienced family law attorney before you sign any binding agreement. We can help you see the long-term implications and protect you from a deal that seems good now but could cause serious problems down the road.

What to Do When an Ex-Spouse Refuses to Pay a Debt

It’s one of the biggest fears people have after a divorce is finalized. You did everything right, you have a final decree signed by a judge, but now your ex-spouse is refusing to pay a debt they were ordered to handle. You're worried their irresponsibility is going to ruin your credit. What can you do?

First, take a deep breath. Your divorce decree is not a suggestion—it’s a legally binding court order. If your ex-spouse fails to follow it, they are in violation of the law, and Texas law provides powerful tools to hold them accountable.

Your Divorce Decree vs. Your Creditors

This is a critical point every person going through a divorce needs to understand: your divorce decree is a contract between you and your ex-spouse. It is not a contract with your bank, credit card company, or mortgage lender.

If your name is still on a joint loan, the creditor can pursue you for payment if your ex defaults. They do not care what your divorce decree says. This is why it is so important to remove your name from shared debts by refinancing or closing accounts as part of the divorce settlement itself.

Filing a Motion for Enforcement

If your ex-spouse is not paying a debt as ordered, your primary legal remedy is to file a Motion for Enforcement. This is a formal legal action filed with the same court that issued your divorce decree, asking the judge to force your ex to comply.

The process is straightforward:

- Your attorney files the motion, detailing the violation.

- The court schedules a hearing that both you and your ex-spouse must attend.

- At the hearing, you must present evidence proving the violation, such as default notices from the lender or bank statements showing missed payments.

You can find more details on this process in our guide on how to enforce a divorce decree.

Potential Remedies and Court Actions

When a judge finds that your ex-spouse has willfully violated the divorce decree, they have significant power to enforce the order. The remedies can include:

- Contempt of Court: The judge can hold your ex in contempt, which can result in significant fines or even jail time until they comply with the order.

- Money Judgment: The court can order a money judgment against your ex for any amount you were forced to pay on their behalf, plus your attorney's fees and court costs.

- Forced Sale of an Asset: A judge can order an asset awarded to your ex in the divorce—such as a vehicle, boat, or even real estate—to be sold to pay off the debt.

- Clarification Order: If the original decree's language was ambiguous, the court can issue a new, more specific order that clarifies the payment obligations in no uncertain terms.

Do not let fear or frustration paralyze you. While it is incredibly stressful when an ex-spouse refuses to pay their share, Texas law provides a clear path forward to protect your credit and enforce your rights.

Taking Control of Your Financial Future After Divorce

Dealing with debt during a divorce feels overwhelming, but this process is also your opportunity to build a new, stable financial life. You can emerge from this with a clear path forward and a renewed sense of control.

What to Do Next

A solid post-divorce financial plan doesn't have to be complicated. By focusing on a few key priorities, you can build a strong foundation for your next chapter.

- Create a Complete Inventory: The first step is to list every single debt. Don't leave anything out, from the mortgage and car loans to every credit card.

- Classify Your Debts: With your attorney, go through that list and classify each debt as community or separate. This is a crucial step that determines who is responsible for what under Texas law.

- Proactively Protect Your Credit: Begin separating your financial life from your spouse's. This means closing joint accounts, refinancing loans into one person’s name, and monitoring your credit score.

- Negotiate from a Position of Strength: Remember that you often achieve a better, more practical outcome by negotiating a settlement in mediation. Leaving these decisions entirely up to a judge means giving up control over the final result.

As you map out your new financial reality, tools like an Alimony Calculator can provide a rough estimate of potential spousal support, helping you create a more accurate post-divorce budget.

The single most important step you can take is to seek professional legal guidance from an attorney who specializes in Texas family law. Trying to make these financial decisions on your own can lead to costly mistakes that follow you for years.

We invite you to schedule a free, confidential consultation with the attorneys at The Law Office of Bryan Fagan, PLLC. Let us help you protect what matters most—your family, your finances, and your future. You don't have to navigate this alone. We're here to provide the clear, compassionate, and authoritative support you need to move forward with confidence.

Frequently Asked Questions About Divorce and Debt

Here are answers to some of the most common "what if" questions we hear from clients facing divorce in Texas.

What if My Spouse Secretly Ran Up Huge Credit Card Debt?

Discovering a mountain of secret debt is a painful and surprisingly common situation. In Texas, because of community property laws, any debt incurred during the marriage is presumed to be a community debt—even if you had no knowledge of it.

However, you are not necessarily stuck with half the bill. You have the right to fight back. During your divorce, you can argue that the debt was not for a community purpose. If your spouse was spending money on an affair, a gambling addiction, or other personal pursuits that did not benefit the family, a judge can assign that debt 100% to them. This is known as proving a "waste claim" on community assets, and it requires strong evidence to be successful.

Can a Judge Force Me to Sell Our House to Pay Debts?

Yes, a Texas family court judge has the authority to order the sale of the family home to pay off community debts. This can be a difficult reality to face, but it often becomes necessary when there are significant liabilities—like high-interest credit card debt or unpaid taxes—and not enough cash or other liquid assets to settle them.

For a court, selling the house is often the cleanest way to clear the financial slate, pay off creditors, and allow both you and your ex-spouse to move forward free and clear.

However, this is not the only option. Through negotiation or mediation, you can propose other solutions. For example, one spouse might agree to refinance the mortgage and buy out the other's share, or you could agree to use other assets to pay down the debt. The court's goal is a "just and right" division, and a well-reasoned, agreed-upon settlement is often preferred.

How Does Bankruptcy Affect Debt Division in a Divorce?

Filing for bankruptcy during a divorce adds another layer of complexity. The timing of the filing and the type of bankruptcy are critical.

- A Chapter 7 bankruptcy, which can wipe out certain unsecured community debts like credit cards and medical bills, might simplify the property division process.

- A Chapter 13 bankruptcy, however, involves a multi-year repayment plan and typically puts the divorce on hold until the bankruptcy court gives its approval to proceed, which can cause significant delays.

Before taking this step, it is imperative that you speak with both an experienced divorce attorney and a qualified bankruptcy lawyer. The interaction between federal bankruptcy law and Texas family law is complex, and a misstep can have severe and lasting consequences on your financial future.

My Ex Was Ordered to Pay a Joint Loan but Filed for Bankruptcy. What Happens to Me?

This is one of the most challenging situations a person can face after a divorce. The divorce decree ordered your ex to pay a debt, but their bankruptcy may have legally discharged their obligation to that creditor.

Here's the problem: the creditor does not care about your divorce decree. They only care that your name is on the original loan. As a co-signer, the creditor has every legal right to come after you for the full amount of the remaining debt.

Your recourse is to go back to the divorce court. While the debt itself may have been discharged in bankruptcy, the obligation your ex owed to you under the divorce decree may not have been. You can ask the court for an order requiring your ex to reimburse you for any payments you are forced to make. Unfortunately, collecting this money can be a long and difficult fight.

Navigating the complexities of debt, divorce, and bankruptcy requires an expert guide. The experienced attorneys at the Law Office of Bryan Fagan, PLLC can help you understand your rights and protect your financial future. If you are facing these difficult questions, schedule a free, confidential consultation with us today at https://texasdivorcelawyer.us to get the clear, compassionate advice you deserve.