Skip to content

Skip to content You log in to a joint account, see a past-due notice, and suddenly the divorce stops feeling theoretical.

When one spouse stops paying bills during divorce, the problem isn't just unfair. It can turn into a housing issue, a credit issue, and a court issue very quickly. In Texas, waiting for your spouse to “do the right thing” usually doesn't protect you. Acting early does.

If you're dealing with missed mortgage payments, a car note that hasn't been paid, utilities at risk of shutoff, or a joint credit card balance that's spiraling, you need a practical plan and a legal strategy.

The Immediate Fallout From Unpaid Bills

The first shock is usually simple. A payment you assumed was handled wasn't handled.

Then the consequences start stacking up. A lender may charge late fees, report delinquency, and begin acting under the loan documents regardless of who moved out of the house, as noted in this guidance on divorce-related mortgage nonpayment. That means the bank is looking at the contract, not the breakup story behind it.

Credit damage starts before the divorce ends

If your name is on the debt, missed payments can affect you even if your spouse promised to cover them. That's especially hard for clients who were trying to keep things calm and avoid conflict. They often assume a private agreement gives them breathing room. It usually doesn't.

Credit problems also create side effects. You may have a harder time refinancing, renting a new place, replacing a vehicle, or opening services in your own name. If you're already seeing damage, it can help to understand practical steps to improve credit while your legal case moves forward.

Essential services can become leverage

Utilities, rent, insurance, internet, and car payments often become pressure points during divorce. One spouse stops contributing, the other tries to keep the household afloat, and the missed bill becomes a tool of control.

Practical rule: Treat housing, transportation, utilities, and insurance as emergency items. Those are the bills that can cause the fastest real-world harm.

A utility company usually cares about the account status, not who was “supposed” to pay under an informal separation arrangement. The same is true for many joint financial accounts. Your long payment history may not stop a shutoff notice or account restriction if the balance is delinquent.

Housing problems escalate fastest

The most dangerous category is usually the roof over your head. Once arrears begin to accumulate, what looked like a private argument can become an emergency court problem. When a mortgage goes unpaid, the issue can shift from monthly budgeting to foreclosure risk.

Here's the practical order of concern:

- Mortgage or rent. Housing loss creates the biggest disruption.

- Electricity and water. Shutoffs can make the home unlivable.

- Vehicle note and insurance. Without a car, many people can't get to work or transport children.

- Minimum debt payments. These matter for credit and collections, but they usually come after safety and shelter.

If you're asking what happens if one spouse stops paying bills during divorce, the short answer is this. The fallout often arrives before the judge does. That's why the first moves you make matter so much.

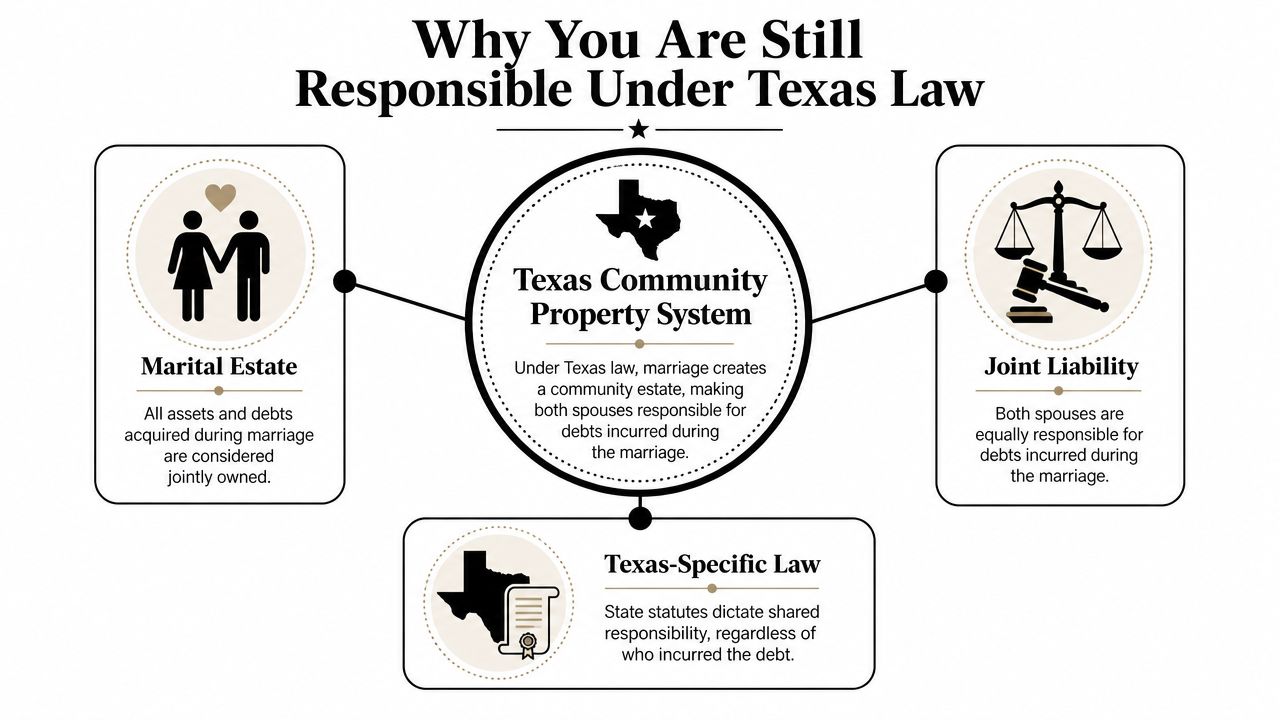

Why You Are Still Responsible Under Texas Law

One of the hardest parts of this situation is how unfair it feels.

You may be thinking, “If the court is going to assign that bill to my spouse, why should I be exposed now?” Texas law draws a line between what spouses owe each other and what a creditor can still collect.

In Texas, debts incurred during marriage are generally treated as community obligations, and Texas Family Code § 3.202 allows creditors to pursue either spouse for those debts. The divorce court can assign responsibility between the spouses, but that allocation doesn't stop a lender from trying to collect from either party, as explained in this discussion of how debt is treated in a Texas divorce and in this Texas law overview on unpaid bills during divorce.

Your divorce order and your loan contract are not the same thing

A simple analogy helps. Think of the divorce court and the creditor as two separate lanes.

In one lane, the family court decides how responsibility should be divided between you and your spouse. In the other lane, the lender looks at the note, the credit agreement, or the account documents and asks whose name is legally tied to the debt. The family court can control the first lane. It usually can't rewrite the second one without the creditor's involvement.

That's why these statements can both be true at once:

| Situation | What it means |

|---|---|

| Your spouse was ordered to pay the bill | You may have a reimbursement or enforcement claim against your spouse |

| Your name is still on the account | The creditor may still pursue you |

The timing issue catches people off guard

In practice, the legal milestones that matter are temporary orders and the final divorce decree. Until then, the payment arrangement can stay unstable. If your spouse stops paying, the damage can happen before the divorce is finished.

The creditor is not required to wait for your divorce to be resolved before taking collection action.

That's why “I'll deal with it in the final decree” is often the wrong strategy when the bills are already going unpaid. If the debt is tied to your name, your credit, or your access to basic services, delay can be expensive.

For business owners and high-asset families, this issue gets more complicated. One spouse may be covering personal bills through a business account, drawing unevenly from a joint line of credit, or selectively paying debts that protect their own interests. The legal analysis is more involved, but the practical point stays the same. If the debt touches you, don't assume the problem belongs only to the other spouse.

Using the Courts for Immediate Financial Relief

Texas divorce courts don't expect you to sit still while the financial ground shifts under you. The main tool for stabilizing things is a temporary orders hearing.

If your spouse has stopped paying bills, temporary orders can create enforceable rules while the divorce is still pending. You can learn more about the process in this overview of a temporary orders hearing in a Texas divorce.

What temporary orders can do

During a pending divorce, courts can use temporary orders to address nonpayment behavior, and a court may order repayment of a nonpaying spouse's share of utilities or other household costs when the evidence shows a pattern of contribution that later stopped, according to this family-law discussion of unpaid household bills during divorce.

Depending on the facts, a judge may address issues such as:

- Who pays which bills while the case is pending

- Who has temporary use of the home or vehicle

- Whether one spouse must provide temporary support

- How joint funds can be used

- Whether reimbursement should be addressed later because one spouse had to cover urgent expenses now

What works and what usually doesn't

The clients who do best in these hearings usually bring proof, not just frustration.

Helpful evidence often includes account statements, screenshots of missed payments, bank records showing prior payment patterns, text messages or emails about who was handling the bill, shutoff notices, late notices, and proof that children or the household are being affected. Judges respond to specifics.

What doesn't work as well is broad blame without documentation. “My spouse is financially abusive” may be true, but you still need records that show the stopped payments, the timing, and the immediate risk.

If you had to pay an essential bill to prevent shutoff, repossession, or further damage, save every receipt and every notice. That paper trail often matters later.

Mediation can help, but it has limits

Some couples can solve this issue in mediation. That may work when both spouses are still communicating and the underlying problem is cash flow, not sabotage. A mediated temporary agreement can be useful if it is clear, written, and quickly enforceable.

But mediation is often the wrong first move when a mortgage is already behind, utilities are at risk, or one spouse is using nonpayment to force concessions on custody or property. In those cases, a court order is usually the safer route.

For parents, the stakes are even higher. If children are living in the home, the court is looking at stability, not just fairness. For professionals and business owners, the court may also need to sort out whether household bills were historically paid through salary, distributions, or business income. Those details can change the temporary relief strategy.

If you need legal help with that process, the Law Office of Bryan Fagan, PLLC handles Texas divorce matters involving temporary orders, support disputes, and property division issues.

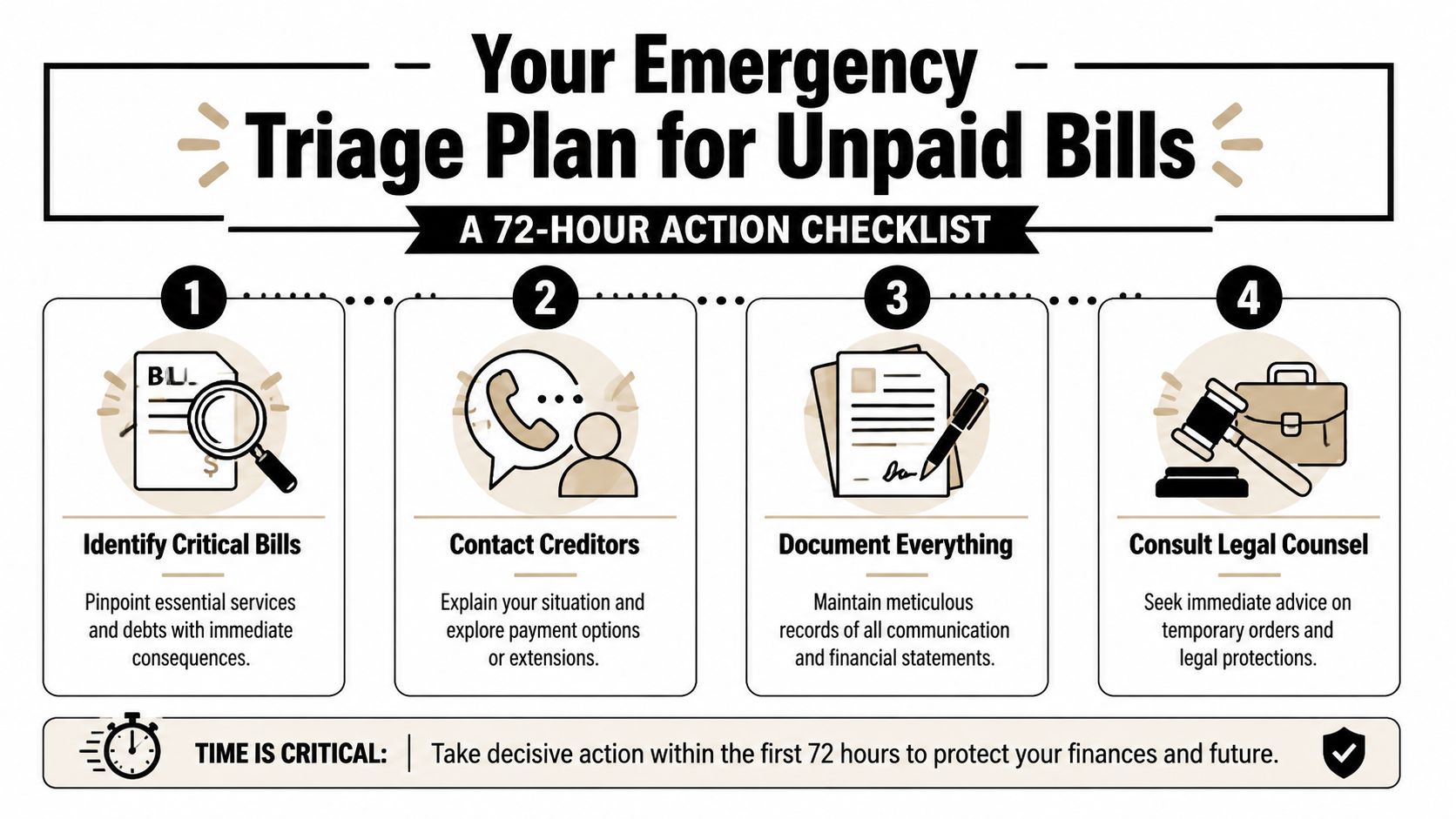

Your Emergency Triage Plan for Unpaid Bills

When bills stop getting paid, the first goal isn't winning the whole divorce. The first goal is preventing avoidable damage.

A major gap in divorce advice is the practical order of operations when bills stop. People often need a triage answer for the first 24 to 72 hours to prevent eviction or credit damage, not just a reminder that both parties are responsible, as noted in this discussion of emergency steps and documentation.

Step 1 Gather documentation fast

Start building a clean file today. Don't trust memory.

Pull together:

- Recent statements for mortgage, rent, utilities, car loans, credit cards, insurance, and bank accounts

- Past-due notices and any shutoff, default, or delinquency alerts

- Payment history showing who had been paying the bill before the stoppage

- Written communications such as texts, emails, or app messages where payment responsibility was discussed

- Proof of your emergency payments if you covered something to stop immediate harm

Take screenshots and save PDFs. If an online portal shows a due date or missed payment, preserve it before the information changes.

Step 2 Identify the bills that can't wait

Not every debt belongs in the same emergency bucket.

Use this quick triage table:

| Priority level | Bills to focus on |

|---|---|

| Highest | Rent, mortgage, electricity, water, vehicle note if needed for work, auto insurance |

| Next | Medical insurance, phone, internet if needed for work or school |

| Then | Minimum payments on revolving debt and nonessential subscriptions |

If you have limited funds, put them where they prevent the biggest immediate loss. In many cases, that means paying a critical bill even if you believe your spouse should have paid it. If you do that, document the payment carefully so your attorney can later ask for reimbursement or offset.

Step 3 Communicate with creditors carefully

You don't have to give a full life story, and you shouldn't make statements that create confusion about the account.

Call with a narrow goal. Confirm the status. Ask what the deadline is to avoid the next level of consequence. Ask whether there is any short-term hold, extension, or payment option available. Write down the name of the representative, the date, and what was said.

A simple script works:

“I'm calling because there is a family-law matter pending, and I need to confirm the current status of the account and the immediate steps required to avoid further action.”

Keep it factual. Don't argue about your spouse. Don't guess. Don't promise full future payment unless you know you can make it.

Step 4 Lock down account visibility and access

If you've been shut out of shared financial information, start restoring visibility. Change passwords on your personal email, review your own bank access, and gather account numbers from statements or tax records if needed. If paychecks are still going into a joint account, talk with your lawyer quickly about the best next step.

For business owners, this step is even more urgent. Separate business records from household records and identify whether any marital bills were being paid through the company. That affects both proof and strategy.

Step 5 Alert your attorney with a usable packet

Lawyers can move faster when they receive organized facts instead of a long stream of panic texts.

Send a short summary that includes:

- Which bills are unpaid

- What deadline or risk exists right now

- What you already paid, if anything

- What proof you have attached

- Whether children, housing, transportation, or essential utilities are affected

That gives your attorney the raw material to decide whether to request emergency relief, temporary orders, reimbursement claims, or another immediate filing.

Common Scenarios for Bill Disputes in Divorce

Most bill fights during divorce fall into a few recurring patterns. The legal details vary, but the pressure points are familiar.

The mortgage stops after one spouse moves out

One spouse leaves the home and decides they shouldn't have to keep paying for a place they no longer live in. The spouse remaining in the house, often with the children, learns the mortgage is behind only after a notice arrives.

The mistake here is assuming the lender will pause because a divorce is pending. It won't. In this situation, the immediate focus is usually preserving the home, documenting the missed payments, and asking the court to allocate responsibility on a temporary basis.

The car note becomes a control tactic

A different version shows up with vehicles. One spouse keeps title or account control over the car loan, but the other spouse needs the vehicle to get to work, pick up the children, or attend medical appointments. Then the payments stop.

This is the kind of dispute that often looks small on paper and huge in real life. Losing transportation can threaten your income and your parenting schedule. A temporary order can be the difference between inconvenience and chaos.

The joint credit card balance jumps after filing

Sometimes the issue isn't nonpayment. It's new spending.

A spouse may continue using a joint card heavily after the divorce is filed, leaving the other spouse worried about growing balances and eventual collection pressure. In those cases, your lawyer may need to address account use, temporary restraints, records of charges, and how to separate necessary spending from strategic overspending.

Financial conflict during divorce often follows old habits that were never clearly documented. If you want a better sense of how couples should structure shared expenses before and during conflict, these rondre's couple budgeting insights offer a useful framework.

What these situations have in common

Each scenario turns on the same practical questions:

- Is there an immediate threat to housing, transportation, or services

- Can you prove who had been paying before

- Do you need court action now or reimbursement later

- Is the dispute really about cash flow, or is it about gaining an advantage

When clients ask what happens if one spouse stops paying bills during divorce, the answer depends less on the label of the bill and more on how quickly the missed payment can destabilize your life.

Enforcement and Your Final Divorce Decree

Temporary orders deal with the emergency. The Final Decree of Divorce is where the court formally divides debts and addresses how the financial mess gets resolved between you and your spouse.

If you paid bills your spouse should have covered, that history can matter in the final property division. The court may account for who carried what burden during the case. This is one reason documentation matters from the beginning.

When the decree is ignored

A final decree has more force than a private promise. If your former spouse still refuses to follow the court's orders, you may need post-divorce enforcement. This can involve a motion asking the court to compel compliance with the decree. If you're dealing with that problem, this guide to enforcing a Texas divorce decree explains the process.

Possible remedies depend on what the decree says and what was violated. In some cases, the court may order compliance, clarify obligations, or address unpaid amounts through enforcement proceedings. The exact remedy will depend on the wording of the order and the type of debt involved.

A decree doesn't erase every outside risk

This is the hard truth many people learn late. Even after divorce, a creditor may still look to the contract if your name remains on the account. The decree helps you enforce rights against your ex-spouse. It does not automatically remove you from a loan.

That's why the long-term cleanup matters too. After the divorce, account transfers, refinances, closures, and title changes should be handled as soon as possible when the decree requires them.

What to Do Next to Protect Your Financial Future

If your spouse has stopped paying bills, don't wait for the situation to “settle down.” Most of these cases get worse, not better, with silence.

Start with the basics. Save the notices. Pull the statements. Protect the bills that keep a roof over your head, lights on, and transportation available. Then get legal advice quickly so your response matches the risk.

You don't need a perfect plan on day one. You need a workable one. For some people, that means using available funds to stop immediate damage and asking the court for reimbursement later. For others, it means moving quickly for temporary orders because the nonpayment is part of a broader pattern of financial pressure.

If children are involved, act even faster. Housing instability, utility shutoffs, and transportation problems don't stay “financial” for long. They spill into school, parenting time, and daily safety.

The question isn't just what happens if one spouse stops paying bills during divorce. The primary question is what you do in the next few days to protect yourself. Quick action, good records, and a focused legal strategy usually put you in a much stronger position.

If you're facing unpaid bills, account lockouts, or a spouse who's using money to gain an advantage during divorce, schedule a free consultation with Law Office of Bryan Fagan, PLLC. You can discuss your situation, understand your options under Texas law, and build a plan to protect your home, credit, and financial future.