Skip to content

Skip to content You may be staring at old bank statements, a house deed, and a sinking feeling that money you thought was yours alone may no longer look that way in a Texas divorce.

When people search for commingled property divorce texas, they’re usually not looking for a textbook answer. They want to know one thing: Did I accidentally put my separate property at risk, and can I still protect it?

That concern is valid. In Texas, small financial habits can create major legal consequences. A deposit into the wrong account, a refinance, a title change, or years of casual transfers between spouses can turn a simple property question into one of the hardest fights in a divorce.

This issue also touches more than property division. It can affect settlement negotiations, mediation strategy, your post-divorce housing options, and how secure you feel when you’re also dealing with parenting plans, support, and the stress of court. If children are involved, property uncertainty often adds pressure to decisions about conservatorship, schedules, and budgeting after divorce.

Your Separate Inheritance and the Joint Bank Account

It usually starts with convenience.

You receive an inheritance from a parent or grandparent. You mean to keep it separate. But life is busy, and the joint account is the account you use for everything. Mortgage payments come out of it. Groceries come out of it. Your paycheck goes in. So does your spouse’s.

Then divorce enters the picture.

Suddenly, that inheritance isn’t just money. It’s your safety net, your family connection, maybe even the last financial gift from someone you loved. And now you’re hearing a term that feels cold and technical: commingling.

Why this becomes a problem fast

Texas is a community property state. That means the law starts from a strong presumption that property possessed by either spouse during or at divorce is community property. If you say an asset is separate, you have to prove it with clear and convincing evidence.

That’s a high bar.

A helpful starting point is learning how Texas courts define separate property in a Texas divorce. Once separate money mixes with marital money, the fight often shifts from ownership by memory to ownership by records.

A real Texas example

One Texas case shows how detailed and difficult these disputes can become. A wife proved that $282,847.69 in an account existed before marriage, but commingling and other disputes still complicated the case. The court ultimately awarded the husband $68,752.66 of community interest. You can read that example in this discussion of separating commingled marital assets in a Texas divorce.

Practical rule: If separate funds enter an account that also receives paychecks, pays family bills, or funds joint purchases, you should assume a tracing problem may already exist.

That doesn’t always mean you’ve lost the asset. It does mean your case may depend on records, timing, and careful legal analysis rather than your intent alone.

Many people are shocked by that. They say, “But I never meant to give it away.” Intent matters in some property questions. But in commingling cases, courts often focus on whether the separate funds can still be clearly identified.

If they can’t, the personal stakes are obvious. What you thought was protected may be pulled into the pool of property the court divides.

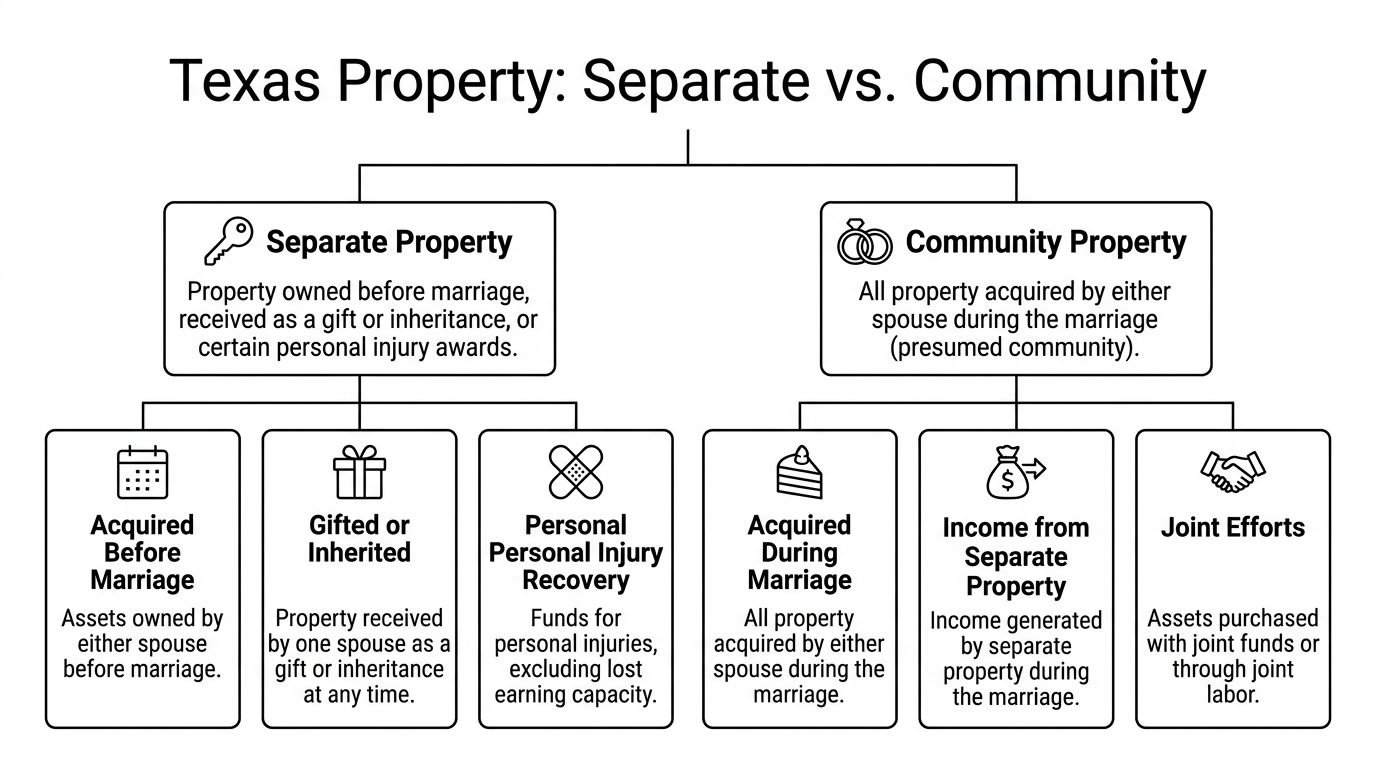

Understanding Separate and Community Property in Texas

Texas law sorts property into two basic buckets. If you don’t know which bucket an asset starts in, it’s almost impossible to understand how it gets mixed later.

Think of marriage like a kitchen.

You each walk in with some ingredients you already owned. Those are your separate ingredients. Then, during the marriage, you cook meals together, buy more groceries, and stock the pantry with income earned while you’re married. That shared food supply is the community estate.

What counts as separate property

Under Texas Family Code § 3.001, separate property includes assets you owned before marriage, as well as property acquired during marriage by gift, inheritance, or personal injury recovery, excluding lost earnings. Property that doesn’t fit those categories is presumed community, as explained in this overview of commingling of assets under Texas law.

In plain English, separate property often includes:

- What you already had: A bank account, land, stocks, or a vehicle you owned before the wedding.

- What came to you alone: An inheritance left to you, or a gift made specifically to you.

- Certain injury recoveries: Some personal injury proceeds, but not compensation for lost earnings.

What counts as community property

Community property generally includes property acquired during the marriage that isn’t separate by law.

That can include:

- Income earned during marriage

- Assets bought with marital earnings

- Accounts built up during marriage

- Property acquired while married, even if only one name appears on it

People often get tripped up. They assume title controls everything. It doesn’t. A house, car, or account in one spouse’s name can still be treated as community property depending on when and how it was acquired.

Why the distinction matters in real life

The court doesn’t dump everything into a pile and split it down the middle. Texas courts divide community property in a just and right way. That means the result isn’t automatically equal.

A judge may look at issues such as:

| Issue | Why it matters |

|---|---|

| Marriage circumstances | The history of the marriage can affect division |

| Income differences | One spouse may have less earning power |

| Child-related needs | Parenting responsibilities can affect future finances |

| Contributions and fault issues | The court may consider the broader picture |

This also affects the larger divorce process. In many Texas divorces, property questions get addressed through temporary orders, document exchange, mediation, and, if needed, trial. If you’re also sorting out children’s issues, you may need to negotiate property alongside parenting arrangements, support, and possession schedules.

The legal label on an asset often matters less than the proof behind it.

If you keep that idea in mind, you’ll understand why commingling becomes such a serious problem.

How Separate Property Becomes Commingled Property

Commingling rarely happens because someone set out to create a legal mess. It happens because married life is practical.

You move money where it’s needed. You pay bills. You refinance. You put both paychecks in one account because that’s easier. You use inherited money to fix the roof because the house needs repair now, not later.

Those choices feel normal. But they can blur the line between separate and community property.

The most common ways this happens

A classic example is the inherited-funds problem. You inherit money that begins as separate property. Then you deposit it into a joint checking account that also receives employment income and pays everyday family expenses. Over time, the original source becomes harder to isolate.

Another example involves a premarital account. You had savings before marriage, then continued using the same account during marriage for deposits, withdrawals, and family spending. The account may still contain some separate funds, but proving which part remained separate can become difficult.

A home can create another layer of complexity. Maybe you owned it before marriage. Then marital funds paid the mortgage, taxes, or major improvements. The home may still have a separate component, but the community estate may also have claims tied to those contributions.

When the lines become too blurred

Texas courts can treat property as community if separate and community funds are mixed to the point that they defy resegregation. That phrase matters.

It means the court can no longer reliably separate one estate from the other.

Consider this example from the verified guidance: if $45,000 in separate savings is mixed with $45,000 in community income plus $10,000 in interest in a joint account, a court may be able to allocate part as separate and part as community, but only if the proof is thorough. Without that proof, the presumption favors community property.

Actions that often create unnecessary risk

Some mistakes are especially common:

- Depositing separate funds into a joint account

- Using inherited money to pay shared debts

- Adding a spouse’s name to a separate asset

- Using one account for both separate and marital transactions

- Failing to preserve statements showing the asset’s origin

People often ask whether using separate money for the marriage automatically converts it into community property. Not always. But it can create a major proof problem, and proof problems lose cases.

Why intent alone usually won’t save you

You may believe, “That was always my inheritance,” or “That account started with my money.” Courts need more than that.

They want documents that show the source of the funds and how those funds moved over time. If years of deposits and withdrawals erased that trail, the court may conclude the property is now part of the community estate.

If you can’t show where the money came from, where it went, and what remained, the law may treat the whole asset as shared.

That’s why commingled property divorce texas cases often turn into record-reconstruction projects. The dispute isn’t only about what happened. It’s about what you can still prove.

The Process of Tracing Commingled Assets

Once property has been mixed, the legal question becomes practical: can anyone unmix it in a way the court will accept?

That process is called tracing. In Texas, tracing is the disciplined reconstruction of an asset’s history so a spouse can try to overcome the community property presumption.

What tracing actually looks like

Tracing is not a casual review of a few statements.

It usually means gathering account records, deeds, loan documents, closing papers, investment statements, transfer records, and sometimes business records. The goal is to follow the money from its separate source through every major transaction.

A court may use methods such as the community-out-first presumption. In a mixed account, that approach assumes community funds were spent before separate funds. That can help preserve a separate claim in some situations, but it can also hurt if the account balance falls too low after the deposit.

If the balance drops below the amount of the separate deposit, your proof may weaken because the separate funds may be treated as having been spent.

The records that matter most

In many cases, the strongest tracing files include:

- Bank statements: Full monthly statements, not just screenshots or summaries

- Deposit records: Proof showing where the money first came from

- Wire confirmations and transfer logs: Especially helpful when money moved between accounts

- Closing documents: For real estate purchases, refinances, or sales

- Title records: Important when ownership and intent are in dispute

- Inheritance or gift documents: These support the original separate classification

- Loan histories: Useful when separate and community funds were both used on property

A useful practical skill in this stage is mastering bank account reconciliation, because tracing often depends on matching deposits, withdrawals, balances, and transfers line by line.

Why experts often become necessary

Some commingled property cases are simple enough for lawyers to present with clean records. Many aren’t.

A forensic CPA or accountant may need to reconstruct the history of an account, prepare schedules, and explain the analysis in a way a judge can follow. In complex Texas divorces, forensic tracing can take 2-6 months and cost $10,000 to $50,000 or more for expert analysis and testimony, according to this discussion of how commingled property can affect a Texas divorce.

That cost can feel frustrating. But when the asset at issue is substantial, tracing may be the only path to preserving it.

A step-by-step view of the tracing process

Step one: identify the claimed separate source

Start with the origin.

Was the money inherited? Was the asset owned before marriage? Was it a gift made specifically to you? That first proof point matters because every later step depends on it.

Step two: build the paper trail

Many people discover gaps here. Missing statements, closed accounts, merged institutions, and old transfers create problems.

Your attorney may subpoena records, request production in discovery, or work with a CPA to recreate the sequence as fully as possible. If you’re dealing with this issue now, this guide on tracing separate property in a Texas divorce is a useful next read.

Step three: test the account history

The analysis gets technical here.

Was the separate deposit preserved? Did the account balance ever drop too low? Were new community earnings deposited into the same account? Were joint expenses paid from it?

Each answer affects whether the separate claim survives.

Here is a brief perspective:

| Tracing question | Why it matters |

|---|---|

| Can you prove the original source? | Without origin proof, the claim usually starts weak |

| Did the account stay above the separate amount? | A low balance may undercut the claim |

| Were community deposits added later? | Mixed deposits complicate reconstruction |

| Did the account fund household spending? | Frequent use often muddies the analysis |

How tracing fits into the divorce process

In a Texas divorce, tracing usually doesn’t happen in isolation.

It may arise during:

- Initial case review and filing

- Temporary orders planning

- Formal discovery

- Mediation preparation

- Trial preparation

- Post-decree enforcement disputes if property division language is unclear

That timing matters. The earlier your legal team spots a tracing issue, the more options you may have. The Law Office of Bryan Fagan, PLLC handles Texas divorce matters involving property division, mediation, and enforcement, which can be relevant when tracing affects both settlement strategy and later compliance.

A short video can also help you visualize how attorneys and courts approach these disputes:

Good tracing tells a clean financial story. Bad tracing leaves the judge guessing, and that usually benefits the community property presumption.

Common Pitfalls and Costly Mistakes to Avoid

Separate property is seldom lost because of intentional disregard for the law. They lose it because they relied on assumptions that sound reasonable but don’t hold up in court.

Mistake one thinking your name on the asset settles the issue

It doesn’t.

A bank account in your name alone can still contain community funds. A house deed with one spouse’s name doesn’t automatically prove the home is separate. Texas courts care about classification, source, and proof.

Mistake two assuming everything gets split equally anyway

Texas uses a just and right division standard for community property. That means a judge is not required to divide community assets equally.

If you walk into mediation or court assuming “it’ll all come out fifty-fifty,” you may make poor settlement choices. Property division can also interact with broader divorce issues, including whether one spouse will handle more child-related expenses, whether support is at issue, and what each person needs to establish a stable home after divorce.

Mistake three adding your spouse to title without legal advice

This is one of the most damaging moves.

People do it to refinance, simplify estate planning, or signal trust in the marriage. But changing title can create a serious argument that you intended to share ownership. Even when that wasn’t your goal, it can make litigation harder and more expensive.

Mistake four keeping weak records

A verbal explanation is rarely enough in a commingling fight.

If you don’t have statements, deeds, transfer records, gift letters, inheritance documents, or account histories, your separate property claim may shrink fast. That’s especially true in long marriages, for business owners, and for people who’ve moved money across multiple institutions.

Mistake five waiting too long to get legal help

Delay creates practical damage.

Banks purge records. People forget dates. Documents get lost during separation. Spouses start moving money in ways that make reconstruction harder. By the time a case reaches mediation, a preventable tracing problem can become a litigation crisis.

A better checklist before you act

If divorce may be coming, avoid these moves unless your lawyer tells you otherwise:

- Don’t transfer major assets casually: A sudden transfer can create new disputes and credibility problems.

- Don’t close accounts without records: Preserve statements first.

- Don’t mix fresh separate funds into shared accounts: That often worsens the tracing issue.

- Don’t rely on memory: Build a document file.

- Don’t ignore related family law issues: Property strategy should fit with your plans for custody, support, mediation, and the final decree.

Warning sign: If you find yourself saying, “I know it was separate, I just can’t prove every step,” you likely need a tracing review before making settlement decisions.

The expensive part of commingling is not always the asset itself. Sometimes it’s the avoidable fight over that asset.

Proactive Strategies to Protect Your Separate Property

The cheapest commingling dispute is the one you never create.

If you already know divorce is possible, or if you want to preserve what you brought into a marriage, the law gives you tools. They work best when you use them early and document them carefully.

Keep separate property truly separate

This sounds obvious, but it’s where many people slip.

An inheritance should usually go into a separate account titled in your name alone. A premarital investment account should not become the family spending hub. If you own a business interest before marriage, keep clean books and avoid paying personal household expenses from business accounts without documentation.

For professionals, business owners, and people with family wealth, clean separation often matters more than good intentions.

Use marital agreements the right way

Prenuptial and postnuptial agreements can be powerful under Texas Family Code Chapter 4. They can define what remains separate, address future earnings, and reduce later fights over whether an asset changed character during the marriage.

But the details matter. According to the Texas Family Law Foundation, 65% of challenged prenups are upheld when disclosure was complete, while failure rates are significantly higher otherwise, as discussed in this article about commingling of funds in marriage.com/blog/commingling-of-funds-in-marriage/).

That should tell you something important. A marital agreement is not magic paper. It needs careful drafting, full disclosure, and proper execution.

Practical protection moves that help

Separate accounts for separate assets

If you receive inherited funds, keep them isolated. Don’t route paychecks through the same account. Don’t use that account for recurring household bills unless you’ve gotten advice about the consequences.

Preserve origin documents

Keep wills, probate distributions, gift letters, old statements, purchase records, and deeds together in one secure file. If you ever need to prove separate ownership, these documents do the heavy lifting.

Document property improvements

If separate property and community funds both touch the same asset, create a paper trail. This is especially important with homes, business interests, and investment accounts.

Think ahead if you’re a business owner

Business owners should consider formal structures, disciplined bookkeeping, and legal planning that separates personal and business finances. If a business began before marriage, records showing ownership, value, and capital contributions can become critical later.

Why proactive planning beats reactive tracing

Tracing tries to rebuild history after the damage is done.

Planning prevents the damage in the first place.

If you expect an inheritance, own substantial premarital assets, or have a high-value estate, legal planning now can spare you months of record chasing later. So can a review of your current titles, accounts, and transfer habits. If you’re thinking about immediate protective steps, this guide on how to protect assets during divorce can help you frame the next conversation with counsel.

A well-kept separate account is often stronger evidence than a long explanation given years later in court.

What to Do Next Your Path Forward

If this topic feels heavy, that’s normal. Property fights in divorce aren’t just about paperwork. They’re about stability, fairness, and whether you’ll have the resources you need when the case is over.

The good news is that confusion can be replaced with a plan.

Start with these immediate steps

Gather records now

Collect bank statements, deeds, account statements, inheritance documents, gift letters, loan records, and closing papers. Don’t wait until mediation is scheduled.Stop casual transfers

Avoid moving large sums, changing titles, or mixing funds further unless you’ve received legal advice specific to your case.Make a property timeline

List major assets, when you acquired them, how they were funded, and whether they were ever placed into a joint account or jointly titled.Identify the high-risk assets

Pay special attention to inheritances, premarital accounts, retirement-related questions, real estate, and business interests.Prepare for the full divorce process

Property division usually unfolds alongside filing, service, temporary orders, discovery, negotiation, mediation, and the final decree. If children are involved, your property strategy should fit with your custody and support strategy, not compete with it.

Questions worth asking before mediation or trial

Ask yourself:

- Can I prove where this asset came from?

- Do I have the statements that show what happened over time?

- Did I put separate money into an account used for family spending?

- Did we use marital funds on a house or asset I owned before marriage?

- Is this a case where a forensic accountant may be necessary?

If you can’t answer those questions clearly, you’re not alone. Many Texans don’t realize the seriousness of commingling until divorce is already underway.

Key takeaway

Commingling is often preventable, but once it happens, proof becomes everything. In a commingled property divorce texas case, your outcome may depend less on what you meant to do and more on what your documents can prove.

That’s why early legal guidance matters. It gives you time to preserve evidence, shape your mediation strategy, and avoid mistakes that can follow you into the final decree. It also helps you think through related issues, from child support and conservatorship planning to enforcement if your spouse has already moved or hidden assets.

You don’t need to solve all of this alone. You do need a clear plan, the right records, and advice grounded in Texas family law.

If you’re worried that separate property has been mixed with marital assets, schedule a free consultation with Law Office of Bryan Fagan, PLLC. You can talk through your records, your divorce timeline, and the steps needed to protect your financial future with clarity and confidence.