Skip to content

Skip to content When divorce becomes real, the question that keeps many people awake is simple: What happens to the house?

If you're searching for answers about real estate division texas divorce, you're probably not looking for abstract rules. You want to know what those rules mean for your home, your mortgage, your children, and your next financial chapter. That’s the right way to think about it.

In Texas, real estate division isn't only about ownership on paper. It's about strategy. Should you fight to keep the home, or would selling it protect you better? Is the property really community property, or do you have a separate property claim? If your spouse handled the finances, how do you make sure nothing is hidden? Those are the decisions that shape your outcome.

A clear path does exist. When you understand how Texas courts approach property, you can make better decisions early and avoid mistakes that are expensive to fix later.

The Foundation of Texas Property Division

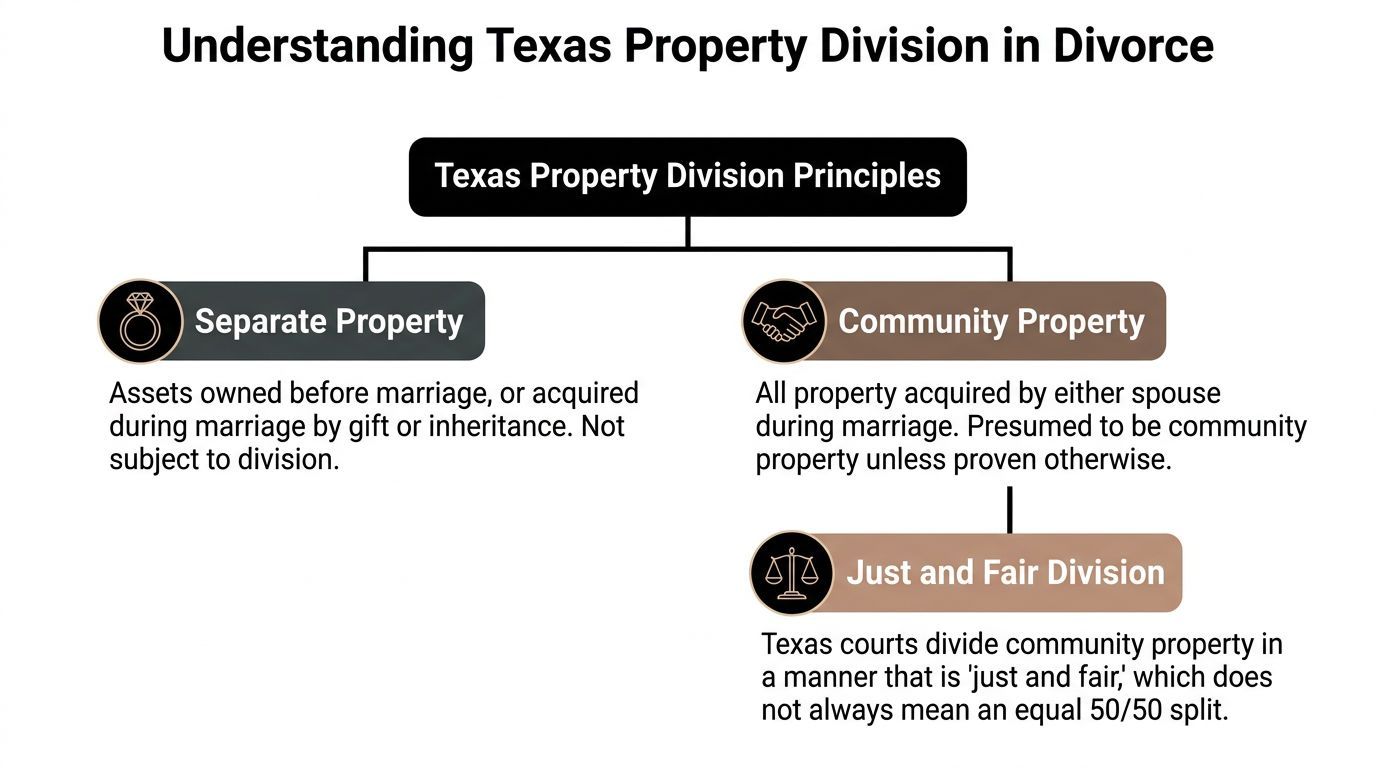

Texas starts with a basic idea. Property must first be classified, then it can be divided.

That sounds simple, but many people get confused by it. A house can feel like "ours" emotionally while still raising legal questions about whether all, part, or none of it belongs in the marital estate.

Community property and separate property in plain English

A useful way to think about this is a two-bucket system.

One bucket is separate property. That usually includes property you owned before marriage, or property you received later by gift or inheritance and kept separate.

The other bucket is community property. In general, that means property acquired during the marriage.

Texas law presumes property is community unless someone proves otherwise. So if a home was purchased during the marriage, the court often starts by treating it as part of the community estate. If one spouse says, "No, that house is my separate property," that spouse usually needs records that clearly trace why.

For a deeper explanation of how these categories work, this guide on separate property vs community property is a helpful starting point.

What just and right really means

Texas doesn't require a strict equal split. Courts divide community property in a manner that is "just and right" under Texas Family Code §7.001, which means a judge can consider factors like fault in the breakup of the marriage or a difference in earning power when dividing real estate (Texas divorce statistics discussion).

That phrase matters because many people walk into divorce assuming everything will be divided down the middle. Sometimes it is. Sometimes it isn't.

A judge may look at practical realities, such as:

- Income differences: If one spouse can earn much more after divorce, that may affect the property split.

- Child-related needs: If one parent will provide most day-to-day care, the house may become part of a broader stability plan.

- Fault issues: In some cases, the court may consider conduct that contributed to the breakup.

- Economic circumstances: Debt load, access to liquidity, and future housing needs can all matter.

Practical rule: "Fair" in Texas doesn't always mean "equal." It means the court tries to reach a division that fits the facts of your family.

Why the house becomes the center of the dispute

Real estate creates pressure because it often carries three different meanings at once.

It is an asset. It is a debt. It is also the place where your life happened.

That mix is why strategic thinking matters. A house with emotional value may still be the wrong asset to keep if the payment, taxes, upkeep, and refinance terms will strain you after divorce. On the other hand, fighting for the home may make sense if it protects children from disruption and fits your long-term budget.

The first decisions you should start making

Before anyone argues over who gets what, start asking better questions:

| Question | Why it matters |

|---|---|

| When was the property acquired? | That often shapes whether the home starts as community or separate property. |

| How is title held? | Title isn't the whole story, but it can point to records you need. |

| Were separate funds used? | Down payments, inheritances, or pre-marital equity can change the analysis. |

| Can you afford the property alone? | Winning the house can become a financial loss if you can't carry it afterward. |

The court process behind the labels

Most Texas divorces follow a practical sequence on property issues:

- Filing begins the case.

- Both sides identify assets and debts.

- Each item is characterized as community or separate.

- Real estate is valued.

- The case resolves by agreement, mediation, or trial.

- The final decree tells each spouse what must happen next.

If you're new to this process, don't worry if it feels technical. It becomes much clearer once you stop seeing the house as one single issue and start seeing it as a set of smaller questions: ownership, value, debt, tax effects, and post-divorce affordability.

Valuing Your Real Estate and Uncovering All Assets

A house can't be divided fairly until you know what it is worth.

That sounds obvious, but many spouses rely on rough online estimates, memory, or informal guesses. Those numbers may feel close enough for casual conversation. They usually aren't strong enough for a divorce settlement.

Why online estimates are not enough

A real estate website may give you a quick estimate, but divorce decisions often require something stronger. The issue isn't just the home’s likely sale price. You also need to understand equity, condition, loan balance, and whether either spouse disputes the number.

If you're trying to make sense of the market before talking with an appraiser or lawyer, learning about finding accurate comparable sales can help you understand why nearby sold properties matter more than wishful thinking.

A practical way to value the home

Valuation generally proceeds in stages.

First, gather the basics. Deed, mortgage statement, tax records, insurance information, and any recent refinance paperwork.

Next, look at the property's current condition. Deferred repairs, upgrades, additions, and neighborhood trends can all affect value.

Then decide whether an agreed value is realistic. If both spouses are close in their estimates, settlement may stay on track. If not, a formal appraisal often becomes the cleanest way to narrow the dispute.

A simple framework helps:

- Start with documents: Pull mortgage statements, closing papers, and records of major improvements.

- Review market reality: Look at recent comparable sales, not only listing prices.

- Use a formal appraisal when needed: This gives the case a stronger foundation if the home becomes a contested issue.

- Calculate net equity carefully: Sale costs, liens, and payoff amounts matter.

Discovery matters when one spouse controlled the finances

Some divorces involve open books. Others don't.

If your spouse handled most of the finances, owned business entities, used LLCs, or moved money between accounts, you may not have a full picture of what exists. That is where the discovery process becomes critical.

In a contested divorce, lawyers can use tools such as document requests, subpoenas, depositions, and sworn disclosures to identify real estate and trace how it was acquired. Those tools matter when someone suspects a rental property, land interest, or business-held property hasn't been fully disclosed.

When the paperwork doesn't match the story, the documents usually decide the issue.

The consequences of hidden real estate

Trying to hide property in a Texas divorce is a serious mistake. Undisclosed or hidden property can trigger fraud claims, and a court may award the innocent spouse up to 100% of the hidden asset's value plus attorney's fees under the Texas Family Code (TexasLawHelp discussion of dividing property and debt).

That risk changes strategy for both sides.

If you think your spouse may be hiding real estate, don't make accusations without a plan. Gather records, look at tax returns, loan applications, closing documents, property tax notices, and business filings. The goal is not drama. The goal is proof.

If you've made informal transfers, side deals with relatives, or title changes that you think "won't matter," assume they may matter a great deal.

What readers often misunderstand

People commonly assume three things that aren't safe to assume:

- "It's only in my spouse's name, so I have no claim." Title alone doesn't always control.

- "It's only in my name, so it's safe." That may be wrong if it was acquired during marriage or enhanced with community resources.

- "If I can't find it, the court can't divide it." Courts can address concealed assets when they are uncovered.

A smart question to ask yourself now

Ask this: Do I know every piece of real estate connected to my marriage, directly or indirectly?

That includes the obvious property, like the family home. It also includes less obvious interests, such as rental homes, lots, mineral-related land interests, vacation property, business-owned real estate, or property held through another entity.

The earlier those questions are asked, the stronger your position usually is.

Your Three Main Options for the Family Home

For most families, the house isn't just another line item. It's the hardest decision in the case.

You usually have three practical paths. Sell it. Buy out your spouse. Or delay the sale for a period of time. Each option can work. The right one depends on your cash flow, your children, your credit, and what kind of life you want after divorce.

If you're weighing whether the house should go on the market during the case, this resource on selling home during divorce can help you think through the timing.

Option one sells the house and divides the proceeds

This is often the cleanest option.

You sell the home, pay off the mortgage and other agreed expenses, and then divide the remaining equity according to settlement terms or the court's order. It creates closure and reduces future entanglement.

This option often works well when:

- Neither spouse can comfortably afford the home alone

- The market supports a sale

- Both spouses want a clean break

- There is conflict and ongoing co-ownership would be risky

The downside is emotional. A sale can feel like losing more than property. It can also disrupt school routines and force both spouses into a new housing search at the same time.

Option two lets one spouse keep the home

This option appeals to many parents because it can preserve stability. One spouse keeps the property and compensates the other spouse for their share of the equity, often through a buyout or offset with other assets.

That can look different from case to case. Sometimes one spouse refinances and pays cash. Sometimes the buyout is balanced against retirement accounts, brokerage assets, or another property.

Here is the practical question: Can the spouse keeping the house afford it?**

Not just this month. Long term.

A buyout also raises title and debt issues that must be written carefully into the decree. If the house is awarded to one spouse but the mortgage stays in both names, the spouse who moved out may still face credit risk. That problem belongs in the planning stage, not after the decree is signed.

Option three delays the sale

Some families choose a deferred sale.

That may happen when children need short-term stability, when the market timing is poor, or when neither spouse is ready to make an immediate move. One spouse stays in the home temporarily, and the property is sold later under terms spelled out in the decree.

A delayed sale can reduce immediate stress, but it requires very clear rules. Who pays the mortgage? Who pays for repairs? What happens if the house needs a new roof? When exactly will the property be listed? What if one spouse refuses to cooperate later?

Without detailed terms, a delayed sale can create the next lawsuit.

Reimbursement claims can change the math

The home may not be the whole story. Sometimes one estate helped another estate.

For example, a spouse may have owned the home before marriage, making it separate property under the inception of title rule. But if community funds were later used to pay the mortgage or fund renovations, that can create a reimbursement claim. These issues are often resolved through mediation, which is successful in approximately 85% of cases according to the cited source discussing Texas property division and mediation (Bryan Fagan property division guide).

That matters because "who keeps the house" is not always the same question as "who owes whom an offset."

A house can be separate property and still create a reimbursement issue. Those are two different legal questions.

This short video can help you think through the practical side of house-related divorce decisions.

A side by side way to compare your options

| Option | Best for | Main risk |

|---|---|---|

| Sell now | Couples who want a clean financial break | Emotional disruption and timing pressure |

| One spouse keeps it | Families who need housing stability and can refinance | Budget strain and ongoing debt exposure if not handled correctly |

| Deferred sale | Short-term stability needs | Future conflict if deadlines and duties aren't detailed |

The strategic question you should ask

Don't ask only, "Can I keep the house?"

Ask, "Should I keep the house based on my post-divorce income, debt, and goals?"

That shift in thinking protects people from a common mistake. They fight hard for a home that no longer fits their financial life. A strong settlement is one you can live with after the case ends.

Handling Mortgages Liens and Post-Divorce Obligations

Many divorce decrees solve the ownership issue but leave people exposed on the debt side.

That is dangerous. If your name is still on the mortgage, the lender can still look to you, even if the decree says your ex-spouse is supposed to pay.

Title and mortgage are not the same thing

This is one of the biggest points of confusion in a real estate division texas divorce case.

The deed controls ownership. The mortgage note controls liability to the lender.

You can be removed from title and still remain liable on the loan. That means a late payment by your ex-spouse can affect your credit and your ability to buy another home.

That is why decrees often need more than a transfer of title. They may need a refinance, an assumption if available, and protective language that addresses what happens if the spouse keeping the house fails to perform.

If you want a clearer look at this issue, this article on assuming mortgage after divorce explains why debt transfer deserves close attention.

Liens and other property obligations

Real estate often carries more than a mortgage.

There may be tax obligations, judgment liens, homeowner association issues, home equity loans, or repair costs that haven't been addressed. Those items need to be identified before settlement, not after.

A practical review should include:

- Mortgage balance: Confirm the current payoff, not just the monthly payment.

- Tax exposure: Review property taxes and whether any amount is delinquent.

- Additional liens: Check for home equity debt, judgment liens, or contractor issues.

- Insurance and upkeep: Decide who covers the property until transfer or sale.

Texas homeowners also need to think about tax treatment after divorce. If you're staying in the home, understanding the Homestead Exemption in Texas may help you identify ownership and occupancy issues that affect your property tax planning.

Enforcement matters if your ex-spouse won't cooperate

Some people assume the decree ends the problem. Sometimes it starts the enforcement phase.

If an ex-spouse refuses to sign deeds or transfer title as ordered, Texas Family Code §9.010 allows courts to award a money judgment for non-compliance or even order the sale of property, and title transfer delays become an issue in an estimated 20-30% of contested divorces according to the cited discussion of enforcement problems (Jeff Gilbert discussion of property division enforcement).jeffgilbertlaw.com/blog/2026/january/dividing-property-and-assets-in-texas-what-you-n/)).

That means your decree should be written with enforcement in mind. Good orders don't just say what should happen. They say when, how, and what happens if someone refuses.

The stronger the decree language, the easier it is to enforce your rights later.

A simple post-decree checklist

| After divorce issue | What to check |

|---|---|

| Deed transfer | Has the deed been signed, delivered, and recorded? |

| Mortgage responsibility | Was the refinance or assumption completed on time? |

| Lien resolution | Were all known liens addressed in the decree? |

| Sale compliance | If sale was ordered, did both spouses cooperate with listing and closing steps? |

People often focus on who "won" the house. A better focus is whether the final orders free you from future risk. That is what protects your financial future.

Special Circumstances in Texas Real Estate Division

Some property cases look simple at first and become complicated the moment you open the file cabinet.

A family home may be tied to a business. A rental property may be held in an LLC. A military family may have moved several times and used special financing. The legal rules still apply, but the strategy changes because the records, risks, and settlement options are different.

When a business owns the real estate

If you own a company, the building itself may not be titled in your personal name. It may sit inside an LLC, partnership, corporation, or another entity.

That doesn't make it irrelevant to divorce. It means the analysis expands.

You may need to examine:

- Entity documents: Formation records, operating agreements, and ownership schedules

- Purchase records: Who funded the acquisition and when

- Cash flow records: Whether business revenue or marital income paid debt or improvements

- Valuation issues: Whether the property value is separate from the value of the operating business

People often make a costly mistake at this point. They assume they are only dividing "the business" or only dividing "the property." In reality, those issues may overlap.

High-asset estates need a coordinated strategy

When multiple properties exist, the goal usually isn't to fight over every address. The goal is to build a full-picture settlement.

That might involve the marital residence, investment properties, vacation property, raw land, and business-tied real estate. Some assets may be better sold. Others may be better offset with non-real-estate assets to avoid forced liquidation.

The cost of getting this wrong can be substantial. In Texas, the average cost for a divorce with children reaches $23,500, partly because property appraisal and valuation disputes drive expense, and high-asset cases can become even more expensive (Brett Pritchard discussion of Texas divorce process and costs).

That doesn't mean every complex case has to become a courtroom battle. It does mean you should treat organization, valuation, and negotiation as serious work from the beginning.

Military families face unique housing questions

Military divorces often add layers to real estate analysis.

A home may have been purchased in one state and divided in Texas. One spouse may move on short notice. A VA-backed home loan may affect timing, affordability, and who can realistically keep the property after divorce.

The strategic question is often less about legal theory and more about logistics. Who can occupy the home? Who is relocating? Does keeping the property make sense if one spouse expects another move soon?

Trusts family gifts and inherited property

Family money often creates confusion because the source of funds matters.

If a parent helped with a down payment, the legal question becomes whether that contribution was a gift to one spouse, a gift to both, or something else that needs documentation. If inherited property was used in connection with the home, tracing becomes important.

These cases are rarely solved by broad statements such as "my parents gave it to me." Courts and opposing counsel usually want records.

A focused team often matters more than a louder fight

Complex property cases reward documentation and planning. They do not reward panic.

That is where many people choose to work with professionals such as appraisers, forensic accountants, tax advisers, and a Texas family law firm that handles property disputes. The Law Office of Bryan Fagan, PLLC handles divorce-related property division, mediation, and enforcement matters as part of its Texas family law practice.

In complicated real estate cases, the winning move is often the clearest paper trail, not the strongest opinion.

If your case involves a business, military issues, inherited wealth, or several properties, your strategy should be built around the exact way those assets were acquired, funded, titled, and maintained.

What to Do Next A Practical Plan to Protect Your Home and Future

The fastest way to weaken your position in a property case is to wait too long to get organized.

You don't need to solve everything today. You do need to start gathering the right information while it is still accessible and before positions harden.

Start with documents not assumptions

If real estate will matter in your divorce, begin building a file.

Include items such as:

- Deeds and closing papers: These help show when and how property was acquired.

- Mortgage and payoff statements: You need the current debt picture, not an old estimate.

- Tax records: Property tax notices can reveal ownership details and ongoing obligations.

- Improvement records: Save receipts, contracts, and bank records for repairs or renovations.

- Communication history: Keep emails or texts about the house, sale discussions, or payment agreements.

- Business and entity records: If any property is tied to a company, gather ownership and financial records.

Avoid common mistakes early

People under stress often make moves that feel practical in the moment but create legal trouble later.

Be careful with choices like these:

- Moving out without a plan. Leaving the home may affect your negotiating position and daily routine with your children.

- Stopping payments without advice. Mortgage defaults can damage both spouses and shrink settlement options.

- Hiding or transferring assets. That can trigger serious consequences, as discussed earlier.

- Agreeing to a buyout based on guesswork. If value and debt aren't clear, the deal may not be fair.

- Ignoring the decree after signing. The post-divorce transfer steps matter just as much as the settlement terms.

Think in terms of goals

A strong property strategy starts with honest priorities.

Ask yourself:

- Do you want stability for your children, or is a clean sale the healthier choice?

- Can you afford the home on your income alone?

- Would keeping the house prevent you from rebuilding savings?

- Is this really about the property, or about not wanting to let go?

Those questions aren't soft. They're practical.

When to talk with a lawyer

If your case involves a house, land, rental property, business-owned real estate, possible hidden assets, or disagreement about value, legal advice early in the process can save time and prevent expensive mistakes.

You may also want guidance if your divorce involves children, because housing decisions often affect possession schedules, support planning, and the larger settlement structure. Mediation can be useful in many cases, and enforcement options exist if a spouse fails to follow the final orders. Property issues often connect with other family law topics such as custody, support, mediation, and enforcement. Looking at the case as a whole usually leads to better decisions than treating the home as a stand-alone dispute.

Key takeaway

Your best next step is not guessing. It is organizing.

Gather the records. Protect your credit. Don't make side deals. Don't rely on verbal promises. And don't assume the house should stay with the spouse who wants it most. The right outcome is the one that protects your future after the divorce is over.

If you're facing questions about your home, mortgage, hidden assets, or a complicated property division, the Law Office of Bryan Fagan, PLLC offers free consultations for Texans dealing with divorce and family law matters. You can talk through your real estate concerns, understand your options, and get a practical plan for protecting your home, your finances, and your next chapter.