Skip to content

Skip to content Watching your carefully built retirement savings become a point of contention in a divorce is one of the most stressful parts of the process.

In Texas, your 401(k) is typically considered community property, which means the portion earned during your marriage is subject to division. This doesn't mean you automatically lose half of everything. Under the Texas Family Code, it simply means you and your spouse have a shared claim to the growth that occurred while you were married, and that portion must be divided in a "just and right" manner.

Your Retirement Future During a Texas Divorce

That feeling of uncertainty about your financial future is completely normal, especially when a major asset like a 401(k) is on the table. The good news is that Texas law provides a clear framework for handling this, giving you a predictable path forward so you can regain control and protect your future.

Understanding how Texas community property rules apply to your retirement accounts is the first step.

The Texas Family Code views your marriage as a partnership. Any wealth you built during that partnership—including your 401(k) contributions, employer matches, and investment gains—is considered part of the community estate. This principle is designed to recognize the contributions of both spouses, whether you were earning a paycheck or managing the household.

Community Property and Your 401(k)

In Texas, courts generally aim for a fair division of marital assets, which often looks like a 50/50 split of the community portion of a 401(k). The key thing for you to remember is that only the value accumulated after your wedding date is on the table.

Any funds in your 401(k) before you were married remain your separate property, as long as you can clearly trace and prove those pre-marital balances. This distinction is crucial and forms the foundation of negotiations.

The trick is to separate the timeline of your savings:

- Separate Property: The balance in your account the day before your wedding.

- Community Property: All contributions, employer matches, and growth from the date of marriage until the date of divorce.

The Role of a Qualified Domestic Relations Order (QDRO)

You can't just write a check to your ex-spouse for their share of your 401(k). Trying to do so would trigger huge income taxes and a 10% early withdrawal penalty from the IRS. To handle this correctly, Texas law requires a special court order called a Qualified Domestic Relations Order (QDRO).

A QDRO is a legal document, separate from your final divorce decree, that instructs your 401(k) plan administrator on how to divide the account. It allows for a tax-free transfer of funds to your former spouse, protecting the value of your hard-earned retirement savings.

This document is absolutely essential for legally and safely splitting a 401(k) in your divorce.

As you start to reassess your retirement readiness, it can be helpful to see how you stack up. You can learn more about the average 401k balance by age to get a sense of common benchmarks. For a deeper dive into the legal protections available, check out our guide on surviving the financial storm of divorce and retirement in Texas.

Defining What's Yours: Separate vs. Community Property

Watching your hard-earned 401(k) get tangled up in divorce negotiations can feel incredibly personal. However, one of the most important first steps you can take is to clearly figure out which parts of that account are yours alone and which belong to the marital estate. This isn’t about hiding money—it’s about rightfully claiming what Texas law already recognizes as yours.

In Texas, the law draws a sharp line between separate property and community property. The easiest way to think about it is to see your wedding date as a dividing line. Everything you earned and saved in your 401(k) before that day is generally considered your separate property. Anything contributed, matched by your employer, or grown during the marriage falls into the community property bucket, belonging equally to you and your spouse.

The Foundation: Proving What's Separate

Here’s the catch: a Texas court will presume everything you own at the time of divorce is community property. The burden is on you to prove otherwise with clear and convincing evidence.

This process is called tracing, and it demands meticulous documentation. You can’t just tell a judge, "I had $50,000 in my 401(k) when we got married." You have to prove it with financial records.

To successfully trace your separate property claim, you'll need to find these specific documents:

- Pre-Marital Account Statements: This is the most important document. The 401(k) statement from the month or quarter right before your wedding date establishes the starting value of your separate property.

- Historical Account Statements: A complete history of statements from the date you got married to the present is incredibly helpful. These show how contributions and market changes affected the account over the years.

- Plan Documents: These can clarify rules about employer matching, vesting schedules, and other details that could impact how the account is valued and divided.

What About Gains on My Separate Property?

This is where things can get a little tricky. We know the initial pre-marital balance is your separate property, but what about the investment gains that money earned while you were married? In Texas, the appreciation and earnings on separate property generally remain separate property.

For example, say you started the marriage with $50,000 in your 401(k). If that specific $50,000, through nothing but market growth, became worth $75,000 during the marriage, that entire $75,000 could still be considered your separate property. The key, however, is that this growth has to be carefully traced by a financial expert to prove it wasn't mixed with growth from new community contributions.

Identifying Separate vs Community Property in Your 401k

Understanding these distinctions is the first step to protecting your assets. Use this table to help categorize the funds in your 401k and see what's on the table for division in your divorce.

| Asset Component | Classification | Why It Matters in Your Divorce |

|---|---|---|

| Balance Before Marriage | Separate Property | This is your starting point. You must prove this amount with pre-marital statements. |

| Contributions During Marriage | Community Property | Any money you or your employer contributed from your wedding date forward is marital property. |

| Gains on Separate Property | Separate Property | Market growth on your pre-marital balance remains yours, but it requires expert tracing. |

| Gains on Community Property | Community Property | All investment growth on contributions made during the marriage is divisible. |

| Vested Employer Matches | Community Property | If the match vested during the marriage (even if contributed before), it's considered community property. |

This breakdown is crucial because only the community portion of your 401k is subject to a "just and right" division by the court. Getting it right can make a massive difference in your final settlement.

The core principle of Texas community property law is that a marriage is a partnership. To fully understand how this affects all your assets, not just retirement accounts, you can explore our detailed explanation of what it means to be a community property state.

Common Mistakes That Can Cost You Dearly

A major risk in this process is commingling, which happens when separate and community funds get so mixed up that they become impossible to tell apart. While a 401(k) is less prone to this than a checking account, sloppy record-keeping can have the same damaging effect.

The single most common—and costly—mistake is failing to find those pre-marital statements. If you can't produce the documents to trace your separate property claim, a judge may have no choice but to classify the entire account as community property, making every last dollar divisible.

It is absolutely critical to start hunting for these documents the moment divorce seems like a possibility. By clearly defining and proving what portion of your 401(k) is truly yours, you take a powerful step toward protecting your financial future and ensuring the division is genuinely fair.

How a QDRO Legally Splits Your 401k

Your Final Decree of Divorce is a powerful legal document, but when it comes to your 401k, it has one major limitation: it can't actually talk to the plan administrator. For that, you need a very specific tool called a Qualified Domestic Relations Order, or QDRO (pronounced "kwah-dro").

Think of the QDRO as the single most important document for dividing your retirement account. Without one, any attempt to pull money out for your ex-spouse is just a regular withdrawal. You'll get hit with a mountain of income taxes and a nasty 10% early withdrawal penalty.

The divorce decree is like the blueprint—it says what needs to be divided. The QDRO, on the other hand, is the legal key that unlocks the 401k and tells the plan administrator exactly how to make it happen. It's a separate, specialized court order signed by the judge, and it’s what turns a taxable distribution into a clean, penalty-free transfer.

Why Your Divorce Decree Is Not Enough

Many clients are shocked to learn that a sentence in their divorce decree saying, "Jane Doe is awarded 50% of the community portion of John Doe's 401k," is completely unenforceable on its own.

Why? Federal law. The Employee Retirement Income Security Act (ERISA) governs most 401k plans, and it lays down a strict rule: a QDRO is required for any division related to a divorce. If a plan administrator only receives a copy of your divorce decree, they are legally obligated to reject your request. It’s a protection for you, your ex-spouse, and the plan itself, ensuring the split is handled correctly and by the book.

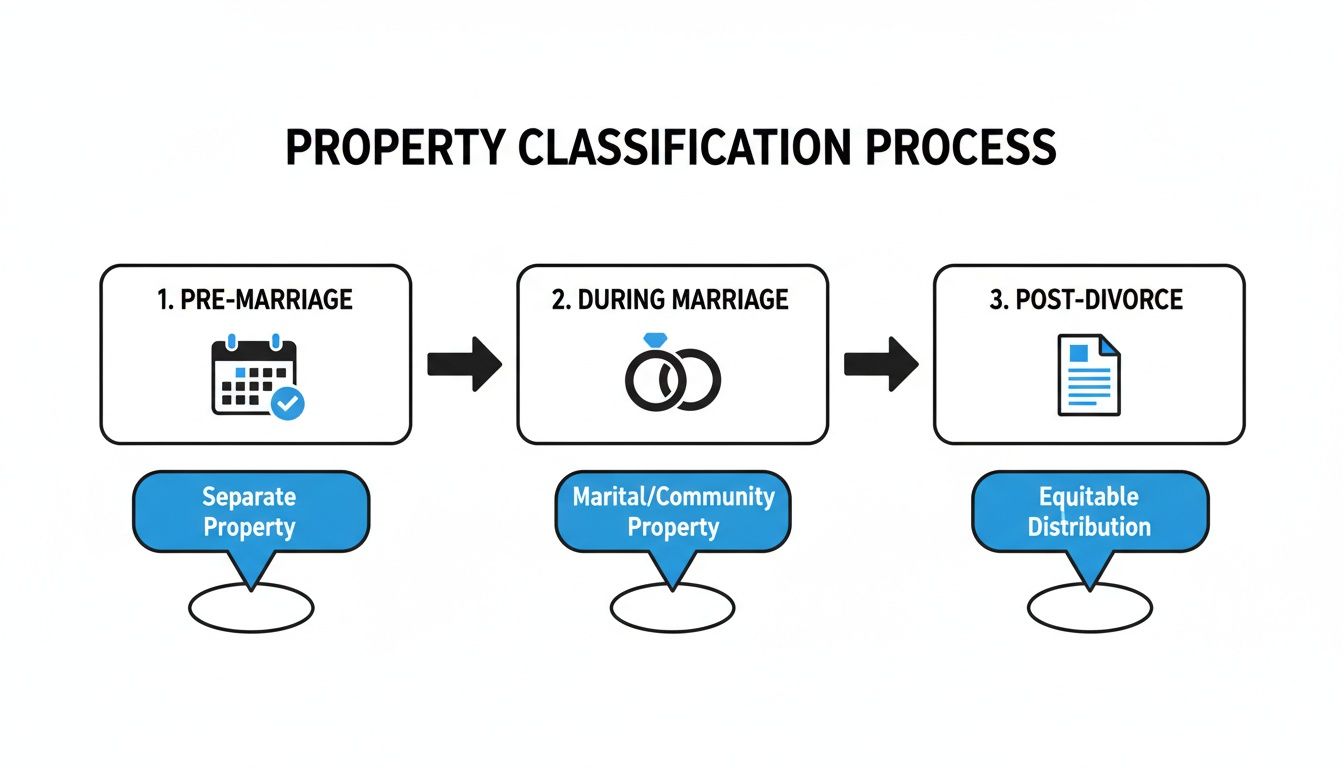

The infographic below shows how property gets classified before a divorce, which is the first step in figuring out what a QDRO will even apply to.

As you can see, the QDRO only targets the assets built up during the marriage—the community estate.

The QDRO Process from Start to Finish

Getting a QDRO isn't something you do at the last minute. Waiting until your divorce decree is signed is one of the most common—and costly—mistakes people make. It can lead to massive delays and headaches.

Here’s a step-by-step breakdown of the QDRO process in a Texas divorce:

- Drafting the Order: Your attorney, sometimes with help from a QDRO specialist, will draft the document. It has to be incredibly specific, listing exact names, plan details, and the precise amount or percentage to be transferred.

- Getting Pre-Approval from the Plan: This is a pro move. Your attorney can send the draft QDRO to the 401k plan administrator before it ever sees a judge. They review it for compliance, catching any language issues that would cause a rejection down the line.

- Approval by Both Sides: Once the draft is good to go, you and your spouse (or your attorneys) will review and sign off on the final version.

- Getting the Judge's Signature: The approved QDRO is then submitted to the court. The judge’s signature makes it an official court order.

- Sending it to the Administrator: The final, certified QDRO is sent to the plan administrator for processing. They will then segregate the funds and transfer them to your ex-spouse, who is now officially known as the "alternate payee."

A properly executed QDRO is your financial shield. It makes it crystal clear that your ex-spouse—not you—is responsible for any taxes when they eventually withdraw the funds from their new retirement account.

Information Your Attorney Will Need

To draft a solid QDRO without delays, your attorney is going to need some key details. Pulling this information together early on will make the entire process run much smoother.

Be ready with this checklist:

- Full Legal Names: The full name of the employee (the "participant") and the ex-spouse (the "alternate payee").

- Current Addresses: Up-to-date mailing addresses for both of you.

- Personal Details: Both Social Security numbers and dates of birth.

- Plan Information: The exact legal name of the 401k plan and the contact information for the plan administrator. You can usually find this on an account statement or by asking your HR department.

- Division Details: The specific dollar amount or percentage being awarded, and instructions on how to handle any investment gains or losses on that amount between the date of divorce and the date of the actual transfer.

From start to finish, getting a QDRO fully processed can take anywhere from a few weeks to several months. Tackling this early in your divorce negotiations is one of the smartest things you can do to protect your financial future.

Navigating the Financial Impact of Division

Let's be honest: splitting a 401(k) in a divorce is more than just a legal step. It’s a moment that can fundamentally change your financial future and your vision for a secure retirement.

Watching an account you’ve spent years building get sliced in half is unsettling. The hard reality is that divorce almost always creates a massive financial hurdle. You’re suddenly trying to support two households on incomes that once supported just one, and that strain hits long-term savings the hardest.

This isn't just a feeling; the research backs it up. Divorce significantly undermines retirement readiness. A report from the Center for Retirement Research at Boston College found that 53% of divorced households face financial risk in retirement, a notable jump from the 48% of non-divorced ones.

The gap in net financial wealth is even more stark. Non-divorced households hold an average of $132,000, which is 30% more than the $101,000 held by divorced households. The reason is simple: splitting a 401(k) can halve your nest egg overnight while your living expenses double. You can dig into the specifics in the full report on how divorce impacts retirement readiness.

The Hidden Costs of Division

Beyond the immediate hit to your account balance, there's a quieter, more powerful cost to consider: the loss of future compound interest. Every dollar transferred to your ex-spouse is a dollar that's no longer growing for your retirement.

Let’s put that into perspective. Imagine the community property portion of your 401(k) is $200,000. In a 50/50 split, your ex-spouse gets $100,000. If that money had stayed put in your account and grown at a modest 7% per year, it would have doubled to $200,000 in about 10 years. That lost future growth is a very real financial impact you have to account for.

Strategic Negotiation: The Asset Buyout

Just because your 401(k) is a divisible asset doesn't mean it has to be split down the middle. Texas law calls for a "just and right" division of the entire community estate, which opens the door for strategic negotiation through mediation. One of the most common and effective strategies here is an asset buyout.

In an asset buyout, one spouse keeps their 401(k) completely intact. To make things fair, the other spouse receives different community assets of equivalent value.

Here’s a practical example:

- Let's say the community portion of your 401(k) is valued at $150,000.

- Your ex-spouse's share would be $75,000.

- You also happen to have $100,000 of equity in the marital home.

Instead of going through the hassle of splitting the 401(k), you could agree that your spouse receives an extra $75,000 of the home equity. In return, you keep your retirement account whole. This can be a win-win, especially if one person is determined to keep the house and the other is focused on preserving their retirement savings.

This approach keeps your retirement funds consolidated and growing, avoiding the disruption of a QDRO. However, it requires having other significant assets to trade and a clear-eyed valuation of everything involved.

Rebuilding Your Nest Egg After Divorce

Seeing your retirement balance drop is disheartening, no question. But it’s not the end of your financial story. Think of it as the start of a new chapter—one that requires a focused and deliberate plan.

Your very first move should be creating a new post-divorce budget. You have to know exactly where your money is going to find opportunities to save. Once you have that clarity, commit to maximizing your 401(k) contributions as quickly as you can. If your employer offers a match, grab it. It's free money, and you can't afford to leave it on the table.

It’s also wise to consider meeting with a financial advisor who specializes in post-divorce planning. They can help you map out a realistic path to get back on track, adjust your retirement timeline if needed, and explore investment strategies that fit your new financial reality. To get a full picture, it's vital to understand the broader tax implications of divorce, which a financial professional can also help clarify.

This process is all about taking back control. While splitting a 401(k) in a divorce is a challenge, strategic negotiation and disciplined planning can put a comfortable retirement back within your reach.

Costly Mistakes to Avoid When Splitting Your 401k

Divorce is an emotional marathon. It’s draining, and it’s all too easy for small details to slip through the cracks—details that can have huge financial consequences later on. Even with the best of intentions, a simple misstep when splitting your 401(k) can cost you thousands of dollars and put your retirement security at risk.

Protecting your future means being proactive and aware of these common pitfalls. This isn’t just about the numbers; it’s about making sure the division of your hard-earned assets is handled correctly, legally, and with your best interests at the forefront. We have seen these mistakes play out time and again, and our goal is to help you sidestep them completely.

Believing Your Divorce Decree Is Enough

One of the most frequent and damaging misconceptions is thinking your Final Decree of Divorce is all you need to divide a 401(k). Your decree can state that your ex-spouse is awarded 50% of the account, but your plan administrator is legally barred from acting on that alone.

You must have a Qualified Domestic Relations Order (QDRO). Without this separate, specific court order, any attempt to move funds will be treated as a taxable distribution. That means triggering income taxes and a potential 10% early withdrawal penalty.

Forgetting to Update Your Beneficiary

Life gets chaotic during a divorce, and this small administrative task often gets pushed to the bottom of the list. But if your spouse is still listed as the primary beneficiary on your 401(k) and you pass away after the divorce is final, they could inherit the entire account.

This can happen regardless of what your divorce decree or will says. The beneficiary designation form on file with your plan administrator is a binding legal contract that almost always overrides other documents.

As soon as your divorce is finalized, make updating your beneficiary designations on all retirement accounts, life insurance policies, and other financial instruments your absolute top priority. It’s a five-minute task that can prevent a devastating and irreversible mistake.

Underestimating the Tax Impact of a Cash-Out

When your ex-spouse receives their portion of the 401(k) via a QDRO, they have a choice: roll it over into their own retirement account or cash it out. If they choose to cash out, they will be responsible for the income taxes on that distribution.

However, a catastrophic error some people make is withdrawing funds directly from their own 401(k) to pay their spouse, completely bypassing the QDRO process. If you do this, you will be on the hook for all income taxes and penalties, creating a massive, unnecessary tax bill for yourself and significantly reducing the net amount your spouse actually receives.

Ignoring an Outstanding 401k Loan

A 401(k) loan is a debt against the account, and it absolutely must be addressed during property division. If you have an outstanding loan, it reduces the account's net value available for division.

Forgetting to account for this loan can lead to a seriously unfair split. Here’s a quick example:

- The Problem: The gross account balance is $100,000, but there’s a $20,000 loan. The actual divisible value is only $80,000.

- The Mistake: If you mistakenly divide the $100,000 gross balance, your ex-spouse gets $50,000. You are left with just $30,000 in assets but are still solely responsible for repaying the $20,000 loan.

- The Solution: The loan must be factored into the valuation from the very beginning to ensure the division is based on the true, accessible account value.

Avoiding these mistakes is crucial for protecting your financial stability. By working with an experienced attorney, you can ensure every detail is handled correctly, safeguarding your retirement savings from costly errors and giving you peace of mind as you move forward.

What to Do Next

Facing the division of your retirement savings can feel overwhelming, but you don't have to navigate this complex process alone. The path forward is about taking clear, strategic steps to protect your financial future.

Here’s where to start:

- Gather Your Documents: Start by collecting every 401(k) statement you can find. The most important one is the statement issued right before your date of marriage. This is your baseline for proving your separate property.

- Consult an Attorney: The complexities of Texas community property law and the technical requirements of a QDRO demand experienced legal guidance. One mistake can cost you tens of thousands of dollars.

- Plan Your Finances: It's never too early to start thinking about your post-divorce budget. You can get a head start by learning how to prepare for divorce financially.

We invite you to schedule a free, confidential consultation with The Law Office of Bryan Fagan, PLLC. Let our experienced Texas divorce attorneys help you create a clear plan to safeguard your retirement and move forward with confidence.

Your Top Questions About Dividing a 401(k), Answered

When you’re staring down the complexities of splitting a 401(k), it’s natural to have a lot of practical questions. You’re not alone. Below, we’ve tackled some of the most common questions we hear from clients just like you, breaking down the answers in plain English.

Do I Have to Give My Spouse Half if We Were Only Married a Few Years?

Yes, but it's crucial to understand it’s only half of the community portion. In Texas, the length of your marriage doesn't change the basic rules of community property. Any growth in your 401(k) from the day you said "I do" until the day your divorce is finalized is considered community property.

That portion is subject to a "just and right" division under the Texas Family Code, which often means a 50/50 split. The money you had in the account before the marriage is your separate property, as long as you have the financial statements to prove it. So, while you aren't splitting the entire account, the piece that grew during the marriage—even a short one—is on the table.

Can We Agree to Trade Other Assets Instead of Splitting the 401(k)?

Absolutely. This is a common and often very smart strategy used in mediation and settlement negotiations. For instance, you might offer your spouse a larger share of the equity in the house or another investment account of equal value in exchange for keeping your 401(k) intact.

The goal in a Texas divorce is to achieve a fair division of the entire community estate. An asset buyout like this can be a win-win, letting each person walk away with the assets they value most. Just make sure this trade-off is clearly spelled out in your Final Decree of Divorce to make it legally enforceable.

What Happens if My Ex Cashes Out the 401(k) Money?

Once the funds are moved into your ex-spouse's name through a Qualified Domestic Relations Order (QDRO), that money is 100% theirs to control. If they decide to cash it out immediately instead of rolling it over into their own retirement account, they are the only one on the hook for the consequences.

This means your ex will be solely responsible for paying the income taxes and any early withdrawal penalties, which is typically a steep 10% if they are under age 59½. The QDRO process is specifically designed so the transfer itself is a non-taxable event for both of you. It shields you completely from any tax mess their future decisions might create.

How Long Does the QDRO Process Take?

The timeline for getting a QDRO finalized can vary, which is why you should get the ball rolling early. First, the QDRO has to be drafted by an attorney, reviewed by both sides, and signed by the judge. But it doesn't end there.

Next, the signed order is sent to the 401(k) plan administrator. They have their own review process to make sure the order meets their internal rules and federal law. This review can take anywhere from a few weeks to several months. Delays are common, so it's critical to get the QDRO process started long before your divorce is final to avoid a frustratingly long wait for the assets to actually be divided.

Navigating the complexities of property division requires a clear strategy and experienced legal guidance. The team at The Law Office of Bryan Fagan, PLLC is here to answer all your questions and protect your financial future. Schedule a free, no-obligation consultation today by visiting us at https://texasdivorcelawyer.us to discuss your case.