Skip to content

Skip to content Facing the financial side of a divorce can feel like staring down a dark, winding road. When you’re trying to figure out how to prepare for divorce financially in Texas, taking the first step to understand your complete financial picture is the most empowering move you can make. This isn't about hiding assets; it's about methodically gathering the information you need to advocate for a fair and just outcome with confidence.

By building a complete inventory of what you own and what you owe, you ensure that you and your attorney have the same information as your spouse. This knowledge is your foundation for taking back control and securing your future.

Your First Steps in Financial Divorce Preparation

When divorce is on the horizon, your head is likely swimming with a storm of emotions. Focusing on your finances can be an anchor in all that uncertainty. This first phase is all about gathering information—a crucial step that builds the foundation for every single decision you'll make from here on out.

Think of it less as an aggressive move and more as a quest for clarity. When you understand the numbers, you can advocate for yourself from a position of strength and knowledge, ensuring you are prepared for the Texas divorce process.

This initial legwork is more than just busy work; it’s essential for your stability. The financial shockwave that follows a divorce can be severe, with some families seeing their income plummet. For a Texas family, a household that was comfortable on a combined income could suddenly face the challenge of surviving on much less. Documenting every penny and building an emergency fund isn't just good advice—it's your practical shield against sudden financial hardship.

Understanding Texas Community Property

Before you can divide anything, you must understand what a Texas court considers marital property. Our state operates under a community property system, which has specific rules you need to know.

In plain English, the Texas Family Code defines community property as nearly all assets and debts acquired by either you or your spouse during the marriage. It doesn't matter whose name is on the title or who opened the account. If it came into your lives while you were married, it's likely considered community property and subject to division.

The flip side is separate property. This includes anything you owned before the marriage, or anything you personally received during the marriage as a gift or an inheritance. Here's the critical part: the burden of proof is on you if you claim an asset is separate. That’s why meticulous documentation is so important from day one.

Start Gathering Key Documents Now

Your mission is to create a complete, unbiased snapshot of your shared financial life. Start by discreetly gathering and making copies of these essential documents. You don’t want to be scrambling for this information later when tensions are high.

- Income Records: Get at least three years of personal and business tax returns, along with recent pay stubs for both you and your spouse.

- Bank and Investment Statements: You need statements from every single account—checking, savings, brokerage, 401(k)s, and IRAs. Don't forget any small accounts you may have forgotten about.

- Debt Information: Pull together records for your mortgage, car loans, student loans, and all credit card statements.

- Property Deeds and Titles: Find the paperwork for any real estate, vehicles, or other high-value assets.

- Insurance Policies: Life, health, home, and auto insurance policies are all part of the marital estate. It's also important to know that divorce is considered an insurance qualifying life event, which gives you a special enrollment period to get new health coverage.

If this feels overwhelming, focusing on the first month can make it manageable. The first 30 days of preparation are about laying a solid foundation for the rest of the divorce process, from filing the petition to the final decree.

Your Financial Preparation Checklist for the First 30 Days

This table breaks down the most critical tasks to tackle right away. Completing these actions in the first month will put you in a much stronger position.

| Action Item | Why It's Important in Texas | Documents to Gather |

|---|---|---|

| Open a Separate Bank Account | To establish financial independence and have a secure place for your own funds. | Your driver's license, Social Security card. |

| Run a Credit Report on Yourself | To identify all joint debts you're legally tied to. You're responsible for them until the divorce is final. | No documents needed—use AnnualCreditReport.com. |

| Gather 3 Years of Tax Returns | These documents provide a comprehensive overview of income, investments, and potential hidden assets. | Federal and state tax returns (personal and business). |

| Copy All Financial Statements | Texas is a community property state; you need a full picture of the entire marital estate to ensure a just and right division. | Bank, investment, 401(k), IRA, and credit card statements. |

| Consult with a Divorce Attorney | To understand your specific rights and obligations under Texas law before making any major decisions. | A list of questions, summary of your assets/debts. |

Tackling this checklist isn't just about paperwork; it's about building a fortress of information to protect your financial future as you navigate the complexities of a Texas divorce.

Building Your Complete Financial Inventory

A fair divorce settlement is built on a foundation of complete transparency. This is where you roll up your sleeves and create a detailed inventory of your entire marital estate, leaving no stone unturned. The goal here is to build a comprehensive financial snapshot that ensures nothing gets overlooked during property division negotiations or court proceedings.

You’re going to move beyond just listing checking and savings accounts. You need to explore every category of what you own and what you owe—real estate, retirement plans like 401(k)s and IRAs, investments, vehicles, and even business interests. It’s a detailed job, but it's absolutely necessary for a fair outcome.

Differentiating Community and Separate Property

In Texas, everything hinges on understanding the difference between community and separate property. Under the Texas Family Code, there's a strong legal presumption that everything you and your spouse acquired from the date of marriage to the date of divorce is community property, meaning it belongs to the marital estate.

Separate property is the exception to the rule. It generally includes:

- Assets you owned before the marriage.

- Property you received as a gift made out specifically to you during the marriage.

- Any inheritance you received during the marriage.

The burden of proof is on the person claiming an asset is separate. You must provide clear and convincing evidence to trace its origins, which is why having pristine documentation is non-negotiable.

A common and costly mistake is commingling, or mixing, separate property with community funds. For instance, if you deposit a $50,000 inheritance into a joint checking account used for household bills, that money can easily lose its separate character and become part of the divisible marital estate.

Assembling Your Asset and Liability Ledger

Think of this as creating a personal balance sheet for your marriage. You need a complete list of everything with a positive value (assets) and everything with a negative value (debts). This level of detail is critical for negotiations and, if necessary, for the court.

Start by listing all identifiable assets. This includes the big, tangible items like your house and cars, but don't forget intangible assets like investment portfolios and retirement accounts.

You also have to account for personal property. While it might seem minor, the collective value of furniture, artwork, and jewelry can add up to a significant amount. A cornerstone of this financial preparation is the thorough process of building your personal property inventory list to ensure every item is accounted for.

Next, you must document every single debt. This means the mortgage, car loans, student loans, personal loans, and the balances on every credit card. In Texas, debts incurred during the marriage are generally considered community debts, no matter whose name is on the account.

When a Forensic Accountant Becomes Necessary

For many couples, a straightforward inventory is sufficient. However, if you own a business, have a high-value estate, or suspect your spouse isn't being truthful about finances, bringing in a specialist is a crucial strategic move.

A forensic accountant is a financial detective. They are trained to dig deeper than a standard accountant, tracing funds, valuing complex assets like a family business, and uncovering any attempts to hide money.

You might need a forensic accountant if:

- Your spouse owns a cash-heavy business where income is hard to track.

- You have complex investments, trusts, or offshore accounts.

- You notice sudden, unexplained changes in financial behavior, like large withdrawals or new, unknown accounts.

Hiring this kind of expert isn't an admission of defeat; it's a powerful step toward ensuring fairness. They provide the court with an objective, expert valuation of your marital estate, which is essential for achieving a just and right division of your property. Their findings can be the key to securing the settlement you deserve.

Creating a Realistic Post-Divorce Budget

Your financial world is about to change, perhaps more than any other part of your life. Creating a budget isn't just about crunching numbers; it’s about figuring out exactly what you'll need from the property division to live comfortably and securely once the divorce is final.

A realistic budget is one of the most powerful tools you have for your long-term stability. It turns vague money fears into concrete, manageable numbers, giving you and your attorney a clear target to aim for during negotiations or mediation.

Establish Your Financial Baseline

Before you can map out your future, you need a crystal-clear picture of where you are right now. The first step is to track your household’s current spending to get an accurate baseline. Don't guess. Pull your bank and credit card statements from the last three to six months and see exactly where every dollar has been going.

You need to categorize everything—from the big-ticket items like the mortgage and car payments down to groceries, utilities, and daily expenses. This detailed breakdown reveals your family’s actual cost of living, which is critical information for determining potential child support or spousal maintenance needs under Texas law.

Project Your Future As A Single Household

Once you have that baseline, the real work begins. Now you have to create a projected budget that reflects what your life will look like as a single person or a single parent. This new budget is going to look very different from your current one.

Some of your expenses might go down, but many new ones will appear. This is where you have to be brutally honest with yourself about the costs you'll now be covering alone.

Your projected budget needs to account for:

- New Housing Costs: Whether you're planning to rent an apartment or hoping to buy out your spouse’s share of the house, you must factor in rent or a new mortgage payment, plus utilities, insurance, and property taxes.

- Healthcare Premiums: If you were on your spouse's health insurance, you will need to get your own policy. This is often one of the biggest and most overlooked financial shocks of divorce.

- Child-Related Expenses: Think beyond the basics. You need to include costs for childcare, extracurricular activities, school supplies, and clothes that you'll now be managing on your own.

- Tax Implications: Your filing status will change from "married filing jointly" to "single" or "head of household." This will have a significant impact on your tax liability, so it’s important to plan for it.

In Texas, this projected budget becomes a crucial exhibit during mediation or court proceedings. It’s not just a personal planning tool; it’s evidence that demonstrates your financial needs to your attorney, the mediator, and potentially a judge.

Secure Your Financial Independence Now

While the divorce is ongoing, it's vital to start establishing your own financial identity. This is a practical step that protects you and prepares you for the moment the divorce is finalized. Taking these actions now shows the court you are financially responsible and helps prevent your spouse from controlling marital funds or damaging your credit.

Start by opening your own individual bank accounts.

- Checking Account: Open a checking account in your name only, preferably at a new bank. This gives you a secure place to deposit your paychecks and pay your personal bills without interference.

- Savings Account: Set up an emergency fund in a separate savings account. This is your safety net for unexpected expenses that will inevitably come up during and after the divorce.

Next, get a handle on your credit.

- Pull your credit report to find every single joint account.

- Open a new credit card in your name only. Use it for small purchases and pay the balance in full each month to start building a strong, independent credit history.

This process of financial separation is a key part of how to prepare for divorce financially. You're building a stable foundation so you can step into your new life with security and confidence.

Protecting Your Home and Retirement Accounts

For most Texans going through a divorce, the thought of losing the family home or watching a hard-earned retirement account get divided is deeply unsettling. Your house isn't just a building; it holds memories. And that retirement fund? It’s your future security. These two assets are almost always the largest and most emotionally charged pieces of the financial puzzle.

Figuring out how to divide them requires a clear head, careful planning, and a solid understanding of Texas law. This isn’t about just splitting things down the middle. It’s about making strategic choices that protect your long-term financial health, because the decisions you make right now will impact you for years to come.

Decoding the Division of Retirement Funds

Here’s a fact that surprises many people: in Texas, any portion of a retirement account—whether it's a 401(k), pension, or IRA—earned during the marriage is considered community property. This means a judge is likely to order a "just and right" division, which often means a 50/50 split of the marital portion.

You might think getting your share is as simple as your ex writing you a check, but it's not that easy. Cashing out retirement funds early triggers massive tax penalties and fees that can wipe out a huge chunk of the money. To divide these assets correctly, you need a very specific legal tool.

The Critical Role of a QDRO

To divide a 401(k) or pension plan without getting hit with significant tax penalties, you absolutely must have a Qualified Domestic Relations Order (QDRO). A QDRO is a special court order, completely separate from your final divorce decree, that gives the retirement plan administrator legal instructions on how to divide the account. It tells them exactly how to pay a portion of the funds to you as the non-employee spouse.

A QDRO isn’t just a suggestion; it’s a legally binding order required by federal law. Without a properly executed QDRO, the plan administrator cannot legally release a single dollar to you. If you fail to get one, you could forfeit your entire share of these retirement assets.

This process is highly technical, and a single mistake in the paperwork can cause major delays or even get the order rejected. For a deeper dive into this crucial step, it's smart to understand the specifics of splitting a 401(k) during a Texas divorce. You need an attorney who has experience drafting and executing QDROs. It's non-negotiable if you want to protect your share of these vital assets.

Making Smart Decisions About the Marital Home

Your home is more than just an asset on a spreadsheet; it's the center of your family's life. When it's time to decide its fate, you generally have three main options, and each one comes with its own financial reality check.

- Sell the House and Split the Proceeds: This is often the cleanest and simplest path forward. You sell the home, pay off the mortgage and closing costs, and divide the remaining equity. It allows both of you to make a fresh financial start.

- One Spouse Buys Out the Other: If you are determined to keep the house, you can buy out your spouse's share of the equity. This almost always requires refinancing the mortgage into your name alone. The big hurdle here is qualifying for that new loan based on a single income.

- Continue to Co-Own the Home: In some cases, usually to provide stability for children, you might agree to co-own the house for a set period after the divorce is final. This path demands a rock-solid agreement spelling out who pays for the mortgage, taxes, insurance, and repairs, and setting a firm date for when the house will eventually be sold.

The right choice comes down to your personal finances and future goals. Can you realistically afford the mortgage, property taxes, and inevitable repairs all by yourself? Sometimes, selling the house is the best move because it gives you the cash you need to find a new place and start rebuilding your life with confidence.

Navigating Divorce as a Business Owner

When your life's work is tangled up in your marriage, divorce feels like more than just a legal process—it's personal. For entrepreneurs and business owners in Texas, a company isn't just an asset; it’s your income, your identity, and your future. The complexity can feel overwhelming, but with the right strategy, you can protect both your financial future and the company you’ve poured your heart into.

This isn't just about dividing an asset. It's about preserving the value and viability of the enterprise you've worked so hard to create. That requires a careful, methodical approach from day one.

Determining the Community Property Interest

The first question a Texas court will ask is: how much of this business belongs to the marital estate? Under the Texas Family Code, any value a business gains during the marriage is presumed to be community property. This holds true even if you started the business long before you were married.

For example, you started your company five years before your wedding. At the time you got married, a valuation showed it was worth $200,000. After a ten-year marriage, the business has grown and is now worth $1 million. In the eyes of the court, that $800,000 increase in value is likely community property, subject to a "just and right" division.

To sort this out, you absolutely must be able to prove the business's value on the date of marriage. This requires a formal, professional valuation.

The Non-Negotiable Step of Business Valuation

You simply cannot reach a fair settlement without an accurate, objective business valuation. This is not a job for your company's regular CPA or a DIY project. You need a neutral, third-party financial expert—usually a credentialed business appraiser or a forensic accountant who specializes in divorce cases.

This expert will analyze:

- Financial Records: Combing through years of tax returns, profit and loss statements, and balance sheets.

- Assets and Liabilities: Taking stock of everything from equipment and real estate to outstanding loans.

- Goodwill: Calculating the intangible value tied to the business’s reputation, brand, and customer base.

Sometimes, both you and your spouse hire your own experts to analyze the numbers. It is also common to agree on a single, neutral expert to produce one unbiased report for use in mediation or court. To get a handle on this crucial step, you can learn more about the details of business valuation in a Texas divorce.

A proper valuation is your shield against an unfair outcome. It provides the court with a credible, evidence-based number, preventing one spouse from undervaluing the business to minimize a payout or the other from overvaluing it out of emotion.

Strategies to Protect Business Operations

While the divorce is proceeding, your business still has to run. The last thing you need is the legal conflict disrupting daily operations, spooking clients, or harming employee morale. Protecting the business itself has to be a top priority.

One of the first moves your attorney will likely recommend is putting a Temporary Restraining Order (TRO) or standing court order in place. These orders establish clear financial rules for both spouses while the divorce is pending.

These court orders can prevent either you or your spouse from:

- Making unusually large withdrawals from business accounts.

- Selling off key business assets without court permission.

- Taking on significant new debt against the business.

- Destroying, hiding, or altering financial records.

This creates much-needed stability and ensures the business's value is preserved until a final property division can be reached. It’s a vital step in separating the marital conflict from the day-to-day health of your company.

Common Financial Questions in a Texas Divorce

When you're facing a divorce in Texas, the financial side of things can feel like a whirlwind. The questions are often urgent, stressful, and loaded with uncertainty. Here are plain-English answers to some of the financial questions we hear most often.

Can I Take Half the Money from Our Joint Account Now?

This is a common question, and the temptation is understandable. While the money in a joint account is legally considered community property, draining a large sum right before or during a divorce is a huge red flag for Texas courts.

Judges often see a sudden, large withdrawal as an attempt to unfairly hide or control marital assets. This move can seriously damage your credibility and backfire when it's time to divide property.

The correct approach is to work with your attorney. We can file for a Temporary Orders hearing to get you the funds you need for living expenses and legal fees. At this hearing, a judge will set fair financial ground rules for both you and your spouse to follow while the divorce is pending, ensuring everything is handled properly.

How Do I Protect My Credit Score During the Divorce?

Your credit score is one of your most important financial assets for life after divorce, and it's vulnerable right now. The first thing you need to do is pull your credit report to see every single joint account you share.

If you and your spouse are on decent terms, try to work together to pay off and close any joint credit cards.

At the same time, open a new credit card in your name only. Start small—use it for gas or groceries and pay the balance in full every month. This is how you begin building your own, independent credit history. Most importantly, make absolutely sure that all joint debts, especially your mortgage, continue to be paid on time. Even one missed payment will hurt both of your credit scores, no matter who the judge eventually holds responsible for the debt.

What if I Think My Spouse Is Hiding Money?

If you suspect your spouse is hiding assets, trust your instincts and tell your attorney immediately. This is a serious issue, and Texas courts have zero tolerance for it.

Your lawyer will initiate the formal discovery process. This isn't just a casual request; it's a set of powerful legal tools, including depositions and formal demands for specific financial documents, designed to uncover inconsistencies and follow the money trail.

For more complex situations, like money funneled through a business or into offshore accounts, we bring in a forensic accountant. These financial detectives are experts at tracing funds and exposing hidden assets. If they prove financial fraud, the Texas Family Code gives judges the power to award a disproportionate share of the marital estate to you—the wronged spouse.

What to Do Next

Knowing how to prepare for divorce financially in Texas is the first step toward reclaiming your future. You've already done the hard work of gathering information. Now, it’s time to turn that knowledge into a clear, prioritized action plan. This is your roadmap for moving forward with confidence.

Your first moves should focus on establishing financial independence and legal protection.

- Open a new bank account and credit card in your name only.

- Consolidate all gathered documents into a secure file for your attorney.

- Consult with an attorney to understand your specific rights under the Texas Family Code.

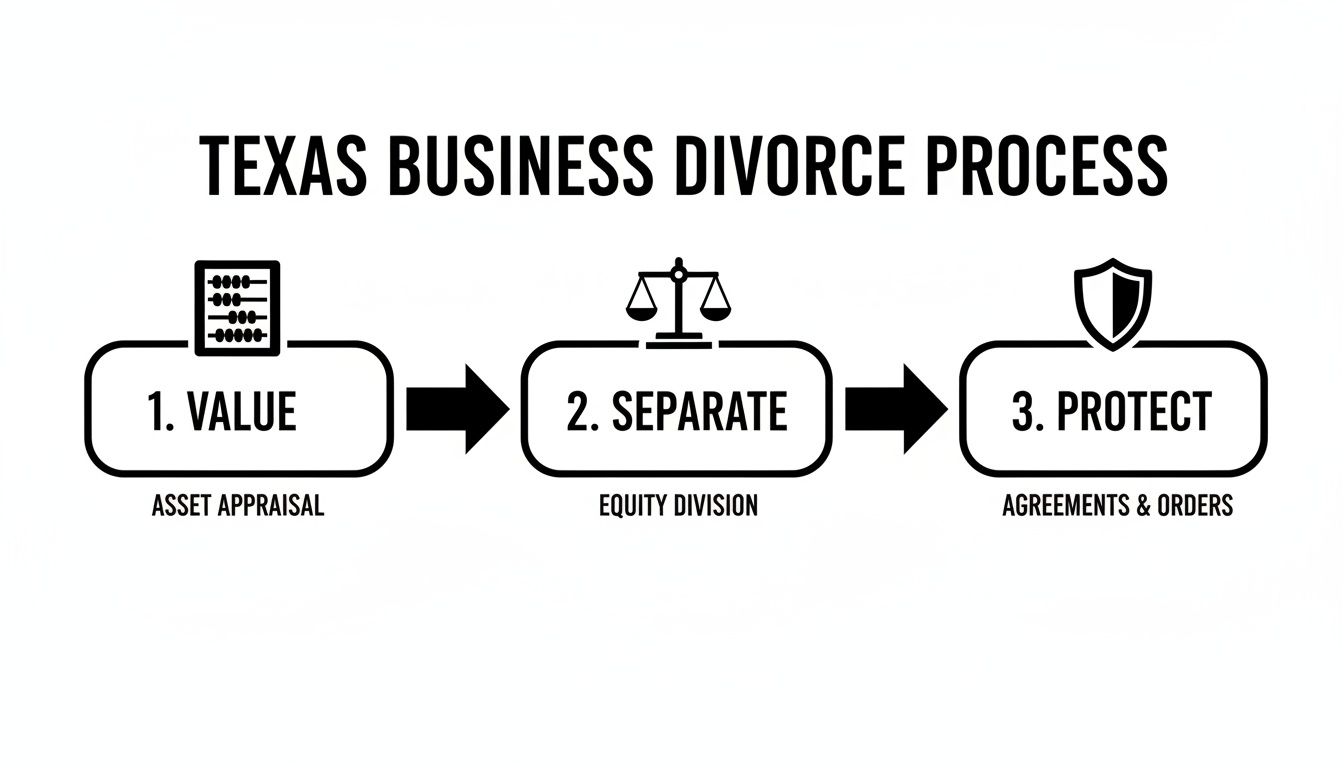

A fair outcome isn't accidental. It's the result of a deliberate strategy that first determines true value, then equitably divides it, and finally legally protects it through court orders. The path to financial security during a divorce is built one step at a time, but the single most critical step you can take is to consult with a skilled Texas family law attorney.

Take control of your future today. Your financial action plan is the first chapter of your new life. Schedule a free, confidential consultation with The Law Office of Bryan Fagan, PLLC. Let our experienced Texas family law attorneys help you translate your preparations into a powerful strategy for a secure and stable future. Visit our Texas Divorce Lawyer contact page to get the experienced legal support you deserve.