Skip to content

Skip to content Watching your shared life get divided up is painful, and the thought of losing your family home can feel like the final blow. A mortgage assumption after divorce is a powerful option that allows you to take over the existing home loan—and its often favorable interest rate—transferring the financial responsibility entirely into your name without the need for a costly refinance. This strategy is a key tool for creating stability, especially when children are involved.

Keeping Your Home After a Texas Divorce

For many Texas families, the home is more than just an asset; it's the heart of your life and a source of stability for your kids. When you're facing divorce, the idea of uprooting everyone can be devastating. Fortunately, Texas law provides a clear path for you to keep your home through a process called a mortgage assumption.

This isn't just about avoiding a move. It’s about preserving a sense of normalcy during a period of immense change. The Texas Family Code treats the marital home as community property, meaning it has to be divided fairly. A mortgage assumption is a strategic way to handle this division, allowing you to keep the home while buying out your spouse's equity interest.

Why Assumption Matters Now More Than Ever

In today's economic climate with fluctuating interest rates, refinancing can be financially crippling. A mortgage assumption lets you bypass that hurdle by keeping the original loan's terms, including what might be a much lower interest rate.

This is a critical advantage for many Texas families. Statistics show that roughly 60% of homeowners carry mortgages into divorce, making assumption a lifeline against financial strain. After a divorce, your single income often has to stretch further, and avoiding a higher monthly payment can make all the difference. To learn more about the financial realities many face, you can explore the insights on navigating a mortgage during a divorce from Fortune.

Protecting Your Financial Future

Beyond keeping your payments manageable, a successful assumption protects both you and your former spouse. For you, it provides the security of keeping your home. For your departing spouse, it ensures their name is removed from the mortgage liability, freeing them to secure new loans without being tied to the old debt. For those of you deciding between keeping or selling, you might be interested in our guide on selling your home during a Texas divorce.

A key financial benefit for Texas homeowners, particularly after a divorce, is understanding and utilizing the Homestead Exemption in Texas. This can provide significant property tax relief, making homeownership more affordable on a single income.

Ultimately, a mortgage assumption is a solution-focused approach designed to provide a clean financial separation and a stable foundation for your new beginning.

Navigating the Mortgage Assumption Process

Taking on the mortgage after a divorce might seem like a huge hurdle, but it's a well-traveled path when you know the steps. Your starting point isn't just calling the bank—it's understanding the powerful legal protection you have on your side. This process is all about securing the home for your future.

A critical piece of federal law, the Garn-St. Germain Depository Institutions Act of 1982, is your strongest ally here. In simple terms, this act stops lenders from calling your loan due (using the "due-on-sale" clause) just because the home's title is transferred to you in a divorce. They can't force you into a brand-new, and likely more expensive, refinance.

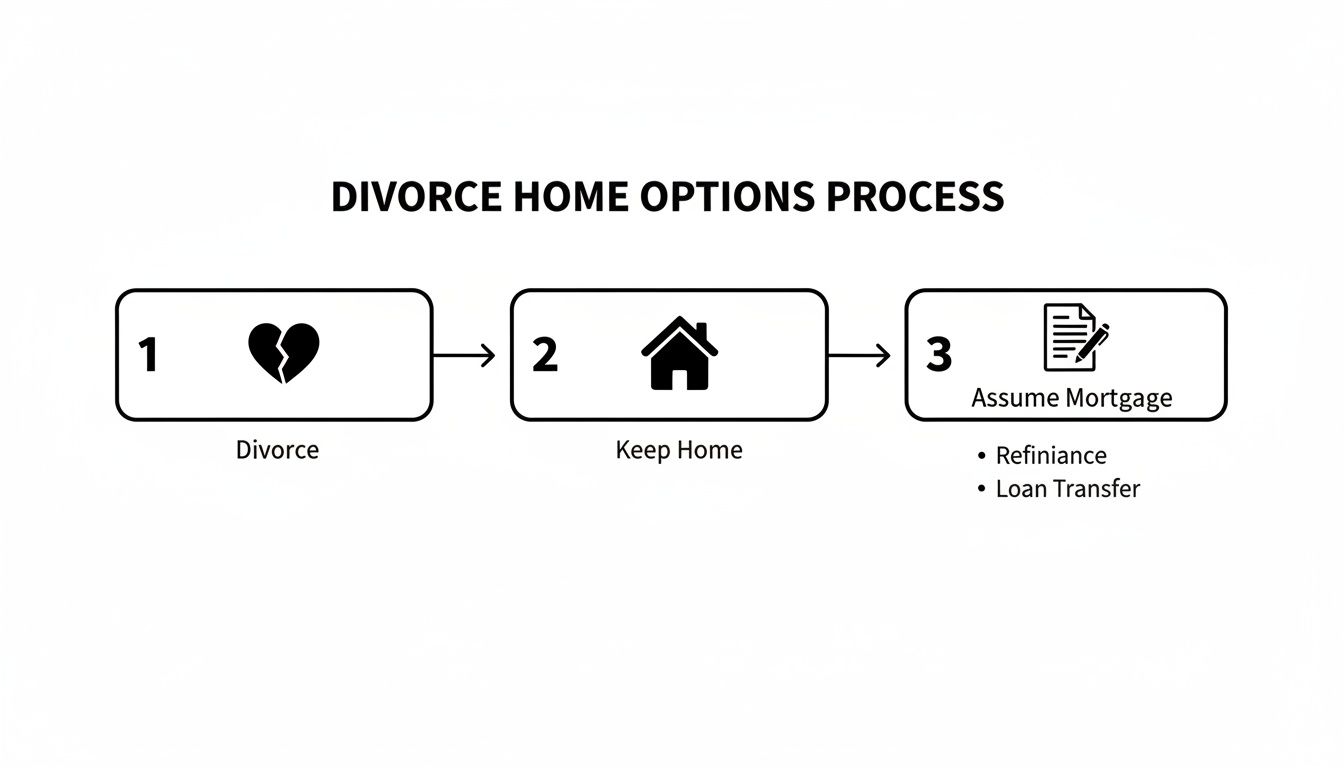

This visual lays out the typical path from the initial divorce decisions to officially making the home and mortgage yours.

As you can see, keeping the home and assuming the mortgage is a direct, viable option—not a long shot. It's a clear alternative to selling the property and starting over.

Step 1: Your Initial Investigation

Before making any calls, the first thing you need to do is dig out your original mortgage documents. Find the paperwork you signed at closing and look for two specific things: an assumability clause and a due-on-sale clause.

Don't panic if you see a standard due-on-sale clause. Remember, the Garn-St. Germain Act creates a federal exception specifically for property transfers tied to a divorce decree. Knowing what your contract says just helps you go into the conversation with your lender fully prepared. For a deeper dive, we created a detailed guide on the specifics of assuming a mortgage after divorce tailored to Texas law.

Step 2: Contacting the Right Department

With your documents in hand, it's time to call your mortgage servicer—the company that collects your monthly payments. This next part is crucial: do not just call the main 1-800 customer service number.

You need to ask specifically to be connected to the Assumption Department or the team that handles loan modifications. The front-line support staff often aren't trained on the nuances of divorce assumptions and might give you wrong information, like insisting that a refinance is your only option. Getting to the right specialists from the start will save you a world of time and frustration.

Once you're on the line with the right person, state your situation clearly and confidently:

- You are finalizing a divorce in Texas.

- The property is being awarded to you in the divorce decree.

- You plan to assume the existing mortgage, as protected by the Garn-St. Germain Act.

This direct, informed approach lets the lender know you've done your homework and are serious about the process.

Step 3: Gathering Your Financial Documents

At the end of the day, the lender’s main concern is simple: can you afford the payments on your own? They will need you to prove your financial stability, much like you did when you first got the loan. While it’s not a brand-new loan application, the financial scrutiny is very similar.

Get ready to pull together a complete financial package.

- Income Verification: This means recent pay stubs, W-2s, and likely your last two years of tax returns. If you're self-employed, you'll need profit and loss statements and other business documentation.

- Proof of Other Income: In Texas, court-ordered payments count toward qualification. Have documentation ready for any child support or spousal maintenance you will receive.

- Asset Statements: Gather recent statements for all checking, savings, and retirement accounts.

- Debt Information: The lender will run your credit, but it helps to have a clear list of all your current debts, like car loans, student loans, and credit card balances.

Your Final Decree of Divorce is the most important document in this entire process. Lenders will not move forward without a copy of the final, judge-signed decree that explicitly awards you the house and makes you solely responsible for the mortgage debt. This is non-negotiable.

Coming to the table with organized, complete documentation shows the lender you're financially capable and helps move their review along. This entire process has to be timed carefully with your Texas divorce proceedings to ensure the transfer of your family home is both seamless and legally sound.

Meeting Lender Requirements and Securing a Release of Liability

Keeping your home really boils down to one critical question: can you prove to the lender that you're financially ready to handle the mortgage on your own? This is where the process shifts from a legal agreement between you and your ex to the financial reality of satisfying the bank. Lenders need absolute confidence in your ability to make every single payment on time, by yourself.

Going through a divorce in Texas is tough, and the family home often feels like the last piece of stability. With about 41% of first marriages ending in divorce—and a staggering 60% for second marriages—you are far from alone in facing this challenge. A mortgage assumption can be a game-changer, allowing you to take over the loan and keep that fantastic low interest rate from years ago. This alone can provide some much-needed financial breathing room.

Proving Your Financial Fitness

To even consider approving the assumption, the lender is going to put your finances under a microscope, much like they did when you first bought the place. They aren't trying to make your life difficult; they're just managing their risk by making sure the loan stays in good hands.

You’ll need to demonstrate your creditworthiness and your solo ability to pay. Here’s what they’ll be looking at:

- Stable and Verifiable Income: The lender wants to see consistent, predictable income. Be ready to hand over recent pay stubs, W-2s, and probably your last two years of tax returns.

- Credit Score: Your credit history is a huge factor. A solid track record of paying bills on time sends a strong signal that you're a reliable borrower.

- Debt-to-Income (DTI) Ratio: This is a key metric for lenders. It compares your total monthly debt payments (the mortgage you want to assume, car loans, credit cards, etc.) to your gross monthly income. A lower DTI ratio shows you have plenty of cash flow to comfortably manage all your obligations.

Here in Texas, your financial picture includes more than just your salary. If your divorce decree awards you spousal maintenance or child support, this court-ordered income can absolutely be used to help you qualify. Just make sure you have the official court documents to prove these payments are consistent and legally mandated.

The Non-Negotiable Release of Liability

While qualifying for the assumption is your goal, protecting your ex-spouse is just as crucial for achieving a clean financial break. This is done with a formal document from the lender called a Release of Liability.

This piece of paper is the official confirmation that your former spouse is no longer legally or financially responsible for the mortgage debt. Without it, your ex remains on the hook in the eyes of the lender, even if your divorce decree says the house is yours. That's an unacceptable risk for them.

If you were to miss a payment, the lender could legally go after your ex-spouse for the money and report the delinquency on their credit report. This could destroy their ability to get a new loan for a car or even a home of their own.

Securing this release is the final, essential step in the assumption process. It completely severs the financial tie to the mortgage, allowing your ex-spouse to move on without being tethered to the old debt. This protection is a cornerstone of any well-managed property division. You can explore other strategies for safeguarding your finances in our article on how to protect assets during divorce.

Meeting the lender's requirements is a detailed but manageable process. By preparing your financial documents and understanding the critical importance of the release of liability, you can confidently take the steps needed to secure your home and your financial independence.

The Role of Your Divorce Decree in a Mortgage Assumption

When that gavel comes down and the judge signs your Final Decree of Divorce, it might feel like the end of a marathon. But if you’re assuming a mortgage, it’s really just the starting line. That decree isn’t just a piece of paper; it’s the legally binding roadmap that dictates every single step of transferring the house and the loan.

Getting the language in that document exactly right is the single most important thing you can do to protect yourself. Vague instructions or missing details can lead to expensive delays, new fights, and even force the sale of the home you worked so hard to keep. This legal document has to be ironclad.

Essential Language for Your Decree

Your divorce decree needs to do more than just say, "You get the house." It has to lay out specific, enforceable instructions that leave zero room for argument. Think of it as a set of crystal-clear instructions that a judge can easily enforce if someone doesn't cooperate.

At a bare minimum, the decree should include:

- A Firm Deadline: You need a specific timeline to apply for the mortgage assumption. A common and reasonable timeframe in Texas is 90 to 180 days from the date the judge signs the decree. This prevents the process from dragging out forever.

- A Cooperation Clause: This is a must-have. It legally requires your ex-spouse to cooperate fully with the process. That means signing whatever documents the lender needs, and doing it promptly.

- A Contingency Plan: What if the lender says no? A well-drafted decree anticipates this. It should clearly outline the next steps, like selling the home and how to split the proceeds, so you aren't forced back into court to figure it out later.

Under the Texas Family Code, a Final Decree of Divorce isn't a suggestion—it's a court order. If your ex refuses to sign the assumption paperwork as required, you can take them back to court on an enforcement action.

This is where having an experienced family law attorney is invaluable. We know how to draft language that is not just clear, but powerful and enforceable under Texas law, shielding you from future headaches.

To make sure your agreement is legally sound, it’s crucial to include specific provisions that protect both parties. Below is a breakdown of the clauses we insist on including in our clients' decrees to ensure a smooth and secure mortgage assumption.

Essential Clauses for Your Texas Divorce Decree

A checklist of critical legal provisions to include in your Final Decree of Divorce to ensure a successful and legally protected mortgage assumption.

| Clause Provision | Purpose | Why It's Critical |

|---|---|---|

| Clear Award of Property | Explicitly states who is awarded the house and its full legal description. | Removes any ambiguity about ownership and is the foundational statement for all other actions. |

| Assumption Obligation | Legally obligates you to assume the mortgage debt. | This creates a legal duty to take over the loan, not just the property. |

| Specific Deadline | Sets a non-negotiable date (e.g., 90 days) to apply for the assumption. | Prevents procrastination and provides a clear trigger for further action if the deadline is missed. |

| Cooperation Mandate | Requires your ex-spouse to sign all necessary lender documents promptly. | Without this, an uncooperative ex can halt the entire process, leaving you stuck. |

| Release of Liability | States the goal is to secure a full "Release of Liability" for the departing spouse. | Clarifies that the process isn't complete until the lender formally removes your ex from the loan. |

| Contingency for Denial | Outlines what happens if the assumption is denied (e.g., sell the house, refinance). | This is your Plan B. It prevents a future court battle by deciding the outcome in advance. |

| Indemnification Clause | Protects your ex-spouse from financial harm if you default before the assumption is final. | Provides a legal remedy to recover damages if your failure to pay hurts your ex's credit. |

Including these clauses provides a comprehensive legal framework that protects everyone involved and gives the court a clear path to enforce the agreement if necessary.

The Deeds That Make It Official

Beyond the divorce decree, two other legal documents are absolutely critical to finalize the transfer and protect both of you. These aren't just formalities; they are the legal instruments that actually change ownership and secure the financial agreement.

First is the Special Warranty Deed. This is the document that officially transfers the property's title from both of your names to just yours. Once your ex-spouse signs it and it’s filed with the county clerk, the legal ownership of the house changes hands.

The second, and equally important, is a Deed of Trust to Secure Assumption. This is the ultimate safety net for the spouse who is moving out. It works by placing a temporary lien on the property in their favor, which stays there until the mortgage lender officially grants the Release of Liability.

This Deed of Trust prevents a nightmare scenario: what if you get the house but stop making the mortgage payments before the assumption is final? In that case, your ex-spouse's name is still on the loan and their credit gets destroyed, but they no longer have any ownership of the property. The Deed of Trust gives them the legal power to step back in and force the sale of the home if you default on the agreement, protecting them from being left financially exposed.

When Assumption Is Denied: Your Backup Plan

It’s a tough pill to swallow when your plan to assume the mortgage falls apart. After all that work, hearing "no" from the lender or discovering your loan isn't assumable can feel like a huge setback. But this isn’t the end of the road—it’s just a detour.

While a mortgage assumption is an excellent goal, a realistic divorce plan always has solid backup options. Whether the lender turns you down or your specific loan type bars assumption, you still have powerful alternatives for securing your financial independence and moving forward.

Alternative 1: Refinancing the Mortgage

The most traditional alternative is to refinance the mortgage. This means you apply for a brand-new loan in your name only, which then pays off the original joint mortgage. It’s a clean break that gets your ex-spouse's name and liability off the books entirely.

The current interest rate environment, however, makes this a challenging path for many. The reality is pretty stark: in 2022, a striking 53.4% of divorced individuals co-owned their homes, making the mortgage a central issue in the property division. Couples who locked in rates around 3% just a few years ago are now looking at rates closer to 7%. That kind of jump can easily add over $1,000 to a monthly payment—an unbearable increase for most post-divorce budgets. You can find more insights on these market trends and their impact on assumptions.

Even with higher rates, refinancing might still be the right move if:

- You have significant home equity and need to "cash out" some of it to buy out your spouse's share.

- Your credit score has improved dramatically, which might qualify you for better terms than you expect.

- The emotional value and stability of keeping the home outweigh the higher monthly cost.

If assumption isn't on the table, exploring refinancing options is often the next logical step to find a new financial path forward.

Alternative 2: A Structured Buyout

Another strong option is what’s called a structured buyout. Here, you pay your ex for their share of the home's equity without refinancing the mortgage right away. This approach definitely requires some creative financial planning.

For instance, you might use other assets from the divorce settlement—like a portion of a retirement account (through a QDRO), an investment portfolio, or savings—to pay your spouse their share of the equity. This lets you keep the house and the low-interest mortgage, though your ex-spouse’s name would stay on the loan until a future sale or refinance.

This strategy absolutely requires a carefully drafted divorce decree with a solid indemnification clause. This clause is critical because it protects the departing spouse by holding you legally responsible for any financial damage—like missed payments—that could harm their credit while their name is still on the loan.

Alternative 3: Selling the Home and Splitting the Proceeds

For some couples, the cleanest break is to sell the marital home. While it can be an emotional decision, selling the property provides a clear and final resolution with no lingering financial strings attached.

Once the house is sold, the existing mortgage gets paid off from the proceeds. Whatever profit is left is then divided between you and your former spouse as laid out in your divorce decree. This allows both of you to walk away with capital to start fresh, free from the shared debt of the old home.

What to Do Next

Trying to navigate a mortgage assumption during a Texas divorce can feel like you’re flying blind. But with a clear plan, you can absolutely secure your home and protect your financial future. The process comes down to three critical actions: confirming your mortgage is assumable, proving to the lender you can handle the payments, and getting ironclad language into your Final Decree of Divorce. This isn’t just a financial hoop to jump through; it's a legal process that demands perfect sync between your divorce case and the bank's red tape.

Your Action Plan for Moving Forward

- Get Your Paperwork in Order: Start pulling everything together now. You'll need your original mortgage documents, the last two years of your tax returns, recent pay stubs, and any court orders about child support or spousal maintenance.

- Find the Right Person to Talk To: When you call your mortgage servicer, ask specifically for the "Assumption Department." Explain your situation and ask for their complete application package and a checklist of their requirements.

- Loop in Your Lawyer: Take everything the lender gives you straight to your family law attorney. They will use that information to draft specific, enforceable language for your divorce decree that protects you and legally requires your ex-spouse to cooperate.

This is not a DIY project. One small mistake in the legal wording or a misstep with the lender could have devastating financial consequences, even forcing you to sell the very home you fought so hard to keep. You have the power to protect your home and start this next chapter of your life on solid ground.

Whether you're in Houston, Dallas-Fort Worth, or anywhere else in Texas, you don’t have to figure this out alone. The experienced team at The Law Office of Bryan Fagan, PLLC is here to give you the clear guidance and strong advocacy you need. We invite you to schedule a free, confidential consultation with one of our attorneys. We’ll listen to your story, answer your questions, and help you build a smart plan to protect your home, your family, and your future.

Common Questions About Divorce and Mortgage Assumption

Going through a divorce and trying to figure out the mortgage brings a flood of questions. It’s a stressful time, and getting straight answers can make all the difference in feeling confident about your next steps. Here are some of the most common questions we get from clients in Texas and the no-nonsense answers you need.

How Long Does the Mortgage Assumption Process Take?

Be prepared to be patient. Once you submit a complete application package to the lender, you can generally expect the review and approval to take anywhere from 30 to 90 days.

This timeline can shift depending on your lender's workload or the complexity of your finances. This is exactly why it’s so critical to have firm language in your Final Decree of Divorce. Your decree should set a hard deadline for applying for the assumption, since the final approval date is out of your hands.

What Are the Common Costs Involved?

While assuming a mortgage is almost always cheaper than a full refinance, it isn’t completely free. Lenders will typically charge an assumption fee, which could be a few hundred dollars or climb to around 1% of the remaining loan balance. You'll also likely see some smaller charges for things like credit reports and administrative processing.

What if My Ex-Spouse Will Not Cooperate?

This is where a skillfully drafted divorce decree becomes your most powerful tool. If your attorney included a "cooperation clause," your ex-spouse is under a court order to sign the necessary assumption paperwork.

If they refuse, they're in direct violation of that order. At that point, your attorney can file an enforcement action with the court to force them to comply. A judge has the power to order them to sign and can even make them pay for the attorney's fees you had to spend to bring them back to court.

Navigating the legal and financial maze of a mortgage assumption after divorce demands a clear strategy and an experienced guide. At The Law Office of Bryan Fagan, PLLC, our attorneys are here to offer the compassionate advice and assertive representation you need to protect your home and secure your future. We invite you to schedule a free, confidential consultation to talk through your specific situation.