Skip to content

Skip to content Watching the retirement account you've poured your life's work into become a battleground in a divorce can be a gut-wrenching feeling. The biggest fear for most people facing this is that they'll automatically lose half of everything they've saved. But the reality of a 401(k) divorce split in Texas is much more specific: only the portion earned or grown during the marriage is considered community property and up for division.

Navigating Your 401k Division in a Texas Divorce

Divorce is hard enough without the added stress of worrying about the retirement you've carefully planned. This guide is designed to cut through the noise and give you clear, straightforward answers to protect your financial future. We'll start by demystifying how Texas community property laws treat your retirement funds, so you can see exactly what's on the table—and what isn't.

Texas is a community property state, which means courts generally aim for a just and right division of all marital assets, which often looks like a 50/50 split. When it comes to your 401(k), this applies to the portion built up during the marriage. Any contributions and growth that occurred before you got married are considered your separate property, as long as you can trace them properly. You can learn more by understanding how Texas community property state laws affect your divorce.

The Role of a QDRO

A critical piece of this puzzle is a legal tool called a Qualified Domestic Relations Order (QDRO). This is the specific court order required to transfer retirement funds to your ex-spouse without triggering massive tax penalties. Trying to split a 401(k) without a QDRO is a recipe for financial disaster, and it's a mistake we see all too often.

Our goal here is to replace your uncertainty with confidence. By understanding the core principles and procedures, you can walk into negotiations with a clear-headed strategy. Think of this guide as a roadmap to protecting the nest egg you've worked so hard to build. You don't have to go through this alone—knowing your rights is the first step toward securing your future.

Understanding Community Property and Your Retirement

To protect the 401(k) you’ve worked so hard to build, you first need to understand how Texas law views your money. The entire system for splitting assets in a Texas divorce boils down to one core idea: community property. This principle sorts everything you own into two buckets, which ultimately decides what’s on the table for division and what’s not.

Think of it like this: before you got married, you had your own financial life—let's call it your "separate property" jar. Any money in that jar, including whatever your 401(k) was worth on your wedding day, is considered yours alone. Once you were married, you and your spouse started filling a "community property" jar together. Everything earned, bought, or saved during the marriage goes into this shared jar.

When a divorce happens, the court only divides what’s in that shared "community" jar. Your separate property jar is supposed to remain yours, but there's a catch: you have to prove it.

How This Applies to Your 401k

This distinction is absolutely critical when it comes to a retirement account. Many people are surprised to learn that just because the 401(k) is in your name, it doesn’t mean it’s all yours. The portion of your 401(k) that Texas considers community property includes:

- Contributions from your paycheck made between the day you got married and the day you get divorced.

- Any employer matching funds you received during that same time frame.

- All investment growth, interest, and dividends that were earned on the community portion of the account.

It’s a huge misconception that your 401(k) is safe just because your name is on the statements. Under the Texas Family Code, Section 3.002, the law starts with a powerful presumption: all property that either spouse has at the time of divorce is community property. The system is designed to assume everything is shared unless you can prove otherwise.

The burden of proof is on you if you are claiming an asset as separate property. Without clear evidence, a court will presume the entire 401(k) is part of the community estate and subject to a "just and right" division, which often means 50/50.

The Importance of Tracing Your Separate Property

This is where the work of tracing comes in, and it's especially important if you had a significant 401(k) balance before you walked down the aisle. Tracing is simply the process of using financial records to prove the exact value of your separate property claim. You can’t just say you had money; you have to provide "clear and convincing evidence" to beat that community property presumption.

To do this, you’ll need to dig up documents that clearly show what the account was worth on or around your wedding date. We’re talking about things like:

- Old 401(k) statements from the months leading up to the marriage.

- A letter from the plan administrator confirming the pre-marriage balance.

- Records that can help distinguish how that separate chunk grew over time, separate from all the new contributions.

For long marriages or accounts where money has been moved around a lot, this can get messy fast. Funds get commingled, making it tough to tell what's separate and what's community. This is precisely why getting an experienced attorney on your side is so vital—they know what evidence to look for and how to present it to protect what is rightfully yours.

Community Property vs Separate Property in a 401k

| Asset Component | Characterization | Why It Matters |

|---|---|---|

| Account Balance on Wedding Day | Separate Property | This amount belongs solely to you and is not subject to division, but you must prove its value with documents. |

| Contributions During Marriage | Community Property | All money you contributed from your paychecks during the marriage is considered a shared asset to be divided. |

| Investment Gains During Marriage | Community Property | The growth on the community portion of your 401k is also part of the marital estate and must be split. |

| Employer Match During Marriage | Community Property | Any matching funds your employer contributed while you were married are also considered a shared asset. |

In short, the law looks at your marriage as a financial partnership. The retirement funds built during that partnership are considered a joint effort, regardless of whose name is on the account. Your job is to clearly identify and prove what you brought into the marriage to keep it off the negotiating table.

How a QDRO Protects Your 401k from Penalties

When you think about splitting a 401(k), you might picture simply writing a check—but doing that would trigger a financial nightmare of taxes and penalties. This is where a Qualified Domestic Relations Order (QDRO) becomes the single most important document in your property division. It’s not just paperwork; it’s your shield against very costly mistakes.

A QDRO (pronounced “kwah-dro”) is a special type of court order, completely separate from your final divorce decree. It gives your 401(k) plan administrator specific, legally-binding instructions on how to divide the account between you and your soon-to-be ex-spouse. Its entire purpose is to bypass the rules that normally punish you for taking money out of a retirement account before age 59½.

Without this legal instrument, any withdrawal from your 401(k) would be treated as an early distribution. That means you could instantly lose 20% to federal income tax withholding, plus a hefty 10% early withdrawal penalty. A QDRO is the only IRS-approved method to split these funds and protect the value you've worked so hard to build.

The Critical Role of a QDRO

Think of a QDRO as a special key that unlocks your 401(k) for one specific purpose—divorce—without setting off all the financial alarms. It’s a formal communication from a Texas judge directly to the financial institution managing the retirement account. This order legally compels the plan administrator to create a separate account for your ex-spouse or to facilitate a direct rollover of their awarded share.

This process is absolutely non-negotiable for 401(k) plans, which fall under a federal law called ERISA (the Employee Retirement Income Security Act). Just stating in your divorce decree that your spouse gets "50% of the 401k" isn't good enough. The plan administrator will reject it and refuse to distribute any funds until they receive a properly drafted and court-signed QDRO.

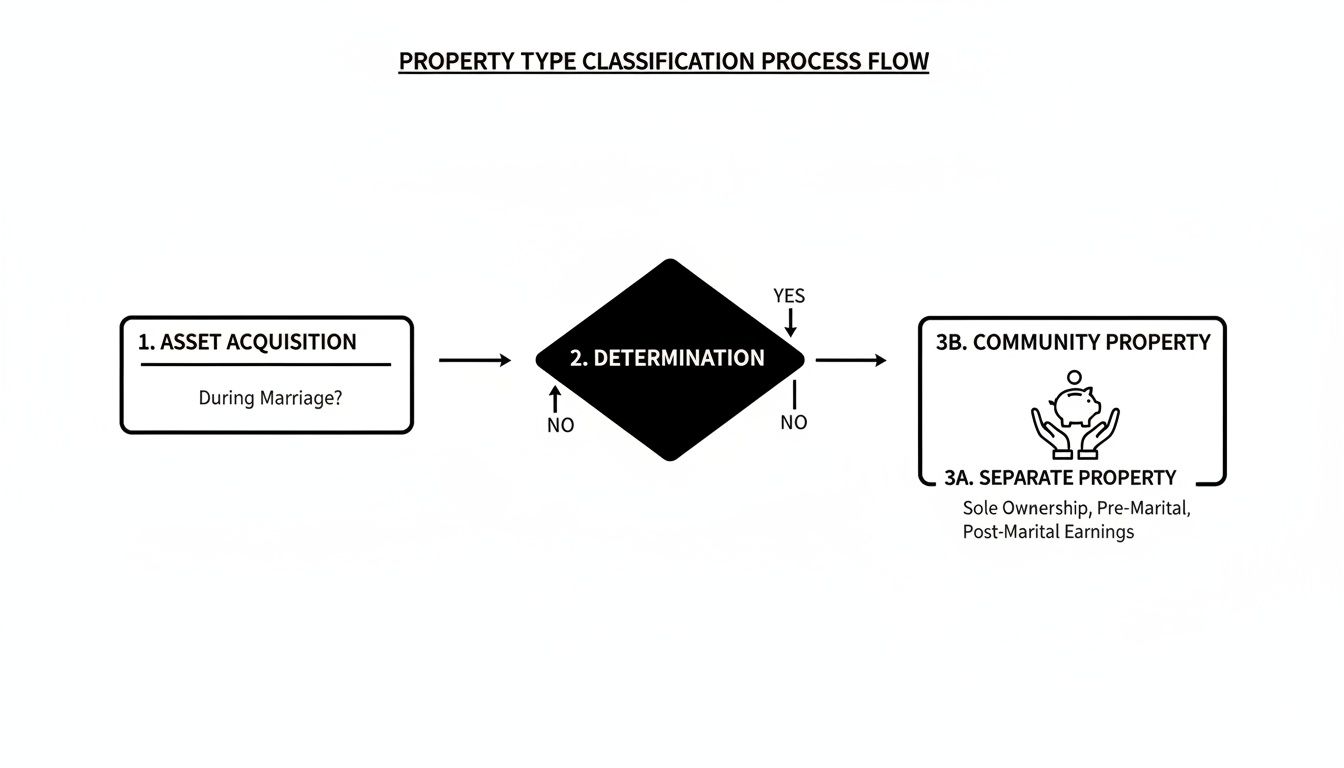

The infographic below shows the basic difference between separate and community property—the very first step in figuring out what portion of the 401(k) the QDRO will actually divide.

This visual helps clarify how your assets are categorized. The QDRO then acts as the legal tool to correctly divide the community portion determined in your divorce.

The Step-by-Step QDRO Process

Getting a QDRO finalized requires precision and patience. A single mistake can lead to rejection and months of delays. While the details can vary, the general path in a Texas divorce follows a clear sequence.

- Drafting the Order: After you and your spouse agree on how to split the account (or a judge orders it), an attorney drafts the QDRO. This isn't a simple form; it has to contain very specific information, like exact names, addresses, account numbers, and the precise dollar amount or percentage being transferred.

- Approval by the Plan Administrator: Before it ever sees a judge, the smart move is to send a draft to the 401(k) plan administrator for pre-approval. They'll check it against their internal rules and tell you if anything needs to be fixed. This step prevents a lot of headaches later.

- Signature from the Judge: Once the draft is pre-approved, it's submitted to the court. A judge signs it, making it an official, enforceable court order.

- Final Submission and Execution: The signed QDRO is then sent back to the plan administrator. They will formally process it and divide the account exactly as the order instructs.

This entire process can take several months, often stretching well past the date your divorce is finalized. Each step is a potential bottleneck, especially if the initial draft has errors or uses ambiguous language.

Why You Need an Attorney to Handle Your QDRO

It might be tempting to find a generic QDRO template online to save money, but this is one of the riskiest shortcuts you can take in a divorce. Every 401(k) plan has its own unique and incredibly strict requirements. If the language in your QDRO doesn’t match exactly what the plan administrator needs to see, they will reject it without a second thought.

A rejected QDRO sends you right back to the beginning—redrafting the document, getting new signatures, and resubmitting everything, all while legal fees continue to mount. An experienced family law attorney knows how to get it right the first time, protecting both your time and your money.

How to Value and Divide Your 401k

Watching your 401(k) balance become a negotiating point can feel intensely personal. After all, you earned it. But a fair division always starts with objective, accurate numbers. Before you can split the community portion of your retirement savings, both sides have to agree on exactly what it’s worth. This process is more than just glancing at the latest statement; it involves key decisions that can dramatically change the outcome of your 401k divorce split.

The first big question is picking a valuation date. This is the specific "snapshot" date used to calculate the value of the community property part of the 401(k). It might seem like a minor detail, but in a fluctuating market, the date you choose can swing the final dollar amount by thousands.

Choosing a Critical Date

In a Texas divorce, there's no single, legally required valuation date. This makes it a crucial point of negotiation between you and your spouse. The most common dates you’ll see are:

- Date of Separation: The day you and your spouse officially stopped living together as a married couple.

- Date of Filing: The day the Original Petition for Divorce was filed with the court.

- Date of Mediation: The day you sit down to formally hammer out a settlement.

- Date of Final Divorce: The day the judge signs the Final Decree of Divorce.

It’s pretty straightforward: choosing a date when the market was high could benefit the non-employee spouse, while a date during a market dip would favor you if the account is in your name. This is often a strategic tug-of-war, negotiated with your attorney’s guidance to ensure the final division is truly "just and right" for your specific situation.

Formulas for Tracing Separate Property

Once you've settled on a valuation date, the next step is to carve out your separate property—that’s the portion of the 401(k) you owned before the marriage. You can’t just subtract the starting balance from day one of the marriage. You also have to account for all the growth that the separate portion generated over the years.

To untangle this, financial experts often use specific tracing formulas. One common method is a pro-rata calculation, which figures out what percentage of the account was separate property at the beginning and applies that same percentage to the investment gains earned during the marriage. This "tracing" process demands meticulous records, which is a key part of the formal discovery process you can learn about in our guide to discovery in a Texas divorce.

A fair valuation isn't just about the numbers on a statement. It's about accurately tracing what you brought into the marriage and ensuring that only the true community portion is subject to division.

When to Call in a Financial Expert

For a lot of straightforward cases, you and your lawyer can handle the valuation with the right 401(k) statements. However, some situations are just too messy and demand a higher level of financial expertise. You should seriously think about hiring a forensic accountant or another financial pro if:

- The marriage was long-term: We’re talking decades of contributions, stock splits, and investment changes that can make tracing feel like an impossible puzzle.

- The 401(k) is a high-value asset: When there are hundreds of thousands or even millions of dollars on the line, the cost of an expert is a smart investment to guarantee accuracy.

- Records are missing or incomplete: An expert often has the tools and methods to reconstruct an account's history even with gaps in the paper trail.

- Funds have been commingled: If money was moved back and forth between different retirement and non-retirement accounts, an expert can unravel that financial spaghetti.

Bringing in a financial expert adds a layer of clarity and credibility. Their impartial report can break a deadlock in negotiations and give the court the clear, hard evidence it needs to make a fair ruling. It’s about making sure your final property division is truly equitable.

Strategic Alternatives to Splitting Your 401k

The thought of a judge carving up the 401(k) you’ve spent a lifetime building is a major source of anxiety in any divorce. For many people, especially business owners or those closing in on retirement, keeping their main investment vehicle intact is priority number one. The good news is, a physical 401k divorce split isn't your only move.

With a smart strategy, you can find creative solutions that let you keep your retirement account whole while still making sure the division of your community property is fair and equitable. The most common and effective alternative is what we call an asset buyout or an asset trade-off.

How an Asset Buyout Works

The idea is pretty straightforward: you keep your entire 401(k), and in exchange, your spouse gets other community assets of equal value. Instead of splitting one big asset down the middle, you’re essentially trading different pieces of your shared financial portfolio until the scales are balanced.

Picture your community estate as a collection of items on a table—the house, cars, a savings account, and your 401(k). If your spouse is entitled to $150,000 from the community portion of your 401(k), you could "buy out" their share by offering them $150,000 worth of other assets.

This trade-off could look a few different ways:

- Giving your spouse a larger cut of the equity from the sale of the family home.

- Transferring a brokerage account or another investment portfolio into their name.

- Giving up your claim to another significant asset, like a valuable art collection or a vacation property.

This approach demands a clear-eyed valuation of every single asset to make sure the trade is truly equal. You also have to consider the after-tax value of different assets, because $100,000 in a pre-tax 401(k) is not the same as $100,000 cash in a checking account.

Pros and Cons of a Buyout Strategy

Before you go down this road, it’s critical to weigh the benefits and the drawbacks. This strategy can be incredibly effective, but it’s not the right fit for every single situation.

Potential Advantages:

- Keeps Your Retirement Intact: You sidestep the complexities of a QDRO and keep full control over your long-term investment strategy.

- Avoids Market Timing Issues: You don’t have to stress about cashing out investments during a market downturn just to split the account.

- Offers Creative Flexibility: It lets you and your spouse customize a settlement that actually meets your individual financial goals.

Potential Disadvantages:

- Requires Liquid Assets: You have to have enough other community property to offset the value of the 401(k) share. If the 401(k) is your only major asset, this just won't work.

- Complex Tax Implications: Trading pre-tax retirement funds for post-tax assets like home equity requires very careful calculation to be fair. A financial expert is almost always needed here.

- Risk of Future Regret: If the asset your spouse takes (like stocks) skyrockets in value later on, you might feel like you got the short end of the stick, and vice-versa.

Finding Creative Solutions in Mediation

These kinds of strategic trade-offs are rarely decided by a judge in a courtroom. A judge's job is to divide property according to the letter of the law, which often just means splitting things right down the middle. Creative solutions like an asset buyout are born from negotiation and collaboration.

This is where methods like mediation truly shine. In a mediation setting, you have the freedom to explore unique financial arrangements that a court might not even consider. You can build a settlement that reflects what’s most important to each of you.

By working together, you can design a property division that feels like a win-win. Maybe keeping the 401(k) gives you peace of mind for retirement, while your spouse would rather have the immediate cash from the house sale to start fresh. To see how this collaborative process can unlock better outcomes, you can learn more about mediation for divorce in Texas and how it can help you protect your most important assets.

Answering Your Top Questions About 401k Splits

When you’re facing a 401k divorce split, it's totally normal for your mind to be racing with questions. The whole process can feel like a tangled mess, but getting straight answers is the first step toward taking back control of your financial future. Let's walk through some of the most common concerns we hear from clients every day.

Can my spouse get my 401k in a short marriage?

Yes, they can—but only their share of the community property portion. Here in Texas, any contributions you made and any growth that happened from the day you got married to the day you divorced are on the table for division.

Whatever was in your 401(k) before the marriage is still your separate property, but you have to be able to prove it with clear, pre-marriage statements. For a short marriage, the amount up for grabs might be pretty small, but the same rules of division still apply.

What happens to a 401k loan I took out?

If you took out a 401(k) loan during the marriage, it’s almost always treated as a community debt. Think of it this way: when it's time to figure out what the account is worth, the outstanding loan balance is subtracted from the total value before the community portion is calculated. It’s absolutely critical that this loan is spelled out clearly in your final divorce decree to sidestep any ugly surprises down the road.

Do I have to sell investments to split the account?

In most cases, no. When a 401(k) is split using a QDRO, the spouse receiving the funds can just roll their share into their own IRA or another retirement account.

This is usually done through an "in-kind" transfer, which means the actual investments—stocks, bonds, mutual funds—are moved over without being sold. This is a huge advantage because it prevents you from getting hit with capital gains taxes. Your spouse could choose to cash out, but that’s almost always a bad move, triggering immediate income taxes and, often, early withdrawal penalties.

Getting a handle on the tax implications is a non-negotiable part of any property settlement. It's not just about the direct split of assets; you need a bigger-picture understanding of how major life changes like divorce impact your taxes to make smart, informed choices.

How long does the QDRO process take?

Be prepared for this to take some time. The timeline is different for everyone, but it can easily stretch for several months, often lasting long after your divorce is officially final. Here’s a rough idea of the step-by-step procedure after the divorce decree is signed:

- Drafting and Review: First, your attorney drafts the QDRO, which is then sent to the plan administrator for pre-approval.

- Judge's Signature: Next, it goes to the court to be signed by the judge.

- Final Submission and Processing: Finally, the signed order is sent back to the 401(k) plan administrator for their final review and execution of the transfer.

Delays are incredibly common, especially if the QDRO is drafted incorrectly and gets kicked back by the plan administrator. This is exactly why it pays to have an experienced family law attorney in your corner—they can get it right the first time and save you from months of frustrating and expensive setbacks.

What to Do Next to Protect Your Retirement

Knowing the rules for splitting a 401(k) in a Texas divorce is a great start, but it's the actions you take now that will truly protect your financial future. That retirement account represents years of your hard work, and you can't afford to leave its protection to chance during such an uncertain time.

Whether you're a business owner with a complex investment portfolio or a parent focused on stability for your kids, every decision you make from here on out will have a long-lasting impact. The smartest way forward is with an expert who lives and breathes Texas family law.

Your first moves should be about getting clarity and taking back control. Here’s a simple game plan to start with:

- Gather All Your Financial Documents: Dig up every 401(k) statement you can find, paying special attention to the ones from around the date you got married. This paperwork is the bedrock of your separate property claim.

- Understand All Your Options: Don't just assume a direct split is your only choice. There are other routes, like trading other assets in a buyout, that might align better with your long-term financial health.

- Talk to a Lawyer First: Do not sign or agree to anything without fully understanding the consequences. One small misstep now could cost you a fortune down the road.

After a major life event like divorce, it’s also a good time to get smarter about your investments. Things like rebalancing your investment portfolio become even more important for your long-term security. A good attorney can connect you with financial experts to help map out a solid post-divorce plan.

Your future isn't just about dividing what you already have. It's about setting yourself up for financial independence and peace of mind for decades to come. Taking control right now is the most powerful move you can make.

Don't sit back and let your financial future be decided for you. The decisions you make during a divorce will echo through your life for years. At The Law Office of Bryan Fagan, PLLC, we are committed to helping you protect your retirement and build a secure future. We invite you to schedule a free, no-obligation consultation with our team. We'll listen to your story, explain your options in plain English, and help you build a solid plan to protect what you’ve rightfully earned. Contact us online or call our office to get started.