Skip to content

Skip to content When you're trying to run a business while going through a divorce, it can feel like you’re caught in two storms at once.

Putting a number on what your business is worth—a process known as business valuation—is one of the most critical steps in making sure assets are divided fairly under Texas law. For many families, the business isn't just a job; it's their single largest and most complicated asset, which makes getting this part right absolutely essential for your future. This guide will walk you through the process step-by-step, so you can feel confident and prepared.

Your Business and Your Divorce: What's at Stake?

You've poured your heart, soul, and savings into building something from the ground up. The idea of that very business becoming a point of contention in your divorce is more than just unsettling—it's personal. You’re not just thinking about balance sheets and profit margins; you’re worried about your future, your legacy, and the financial stability you've worked so hard to create. Feeling this way is completely normal, but with a clear plan and the right information, you can get through it.

The first step is to understand why your business is even part of the conversation. In Texas, the law sees a marriage as a partnership. That means most property acquired or grown during that partnership belongs to both of you, in what's called the community estate.

According to the Texas Family Code § 3.002, community property is made up of any assets that either spouse acquires during the marriage. This legal presumption means a business started or even just grown significantly while you were married is subject to a "just and right" division when you divorce.

Understanding Community Property in Texas

This core principle has huge implications for you as a business owner. Even if your name is the only one on the company's legal documents, a huge chunk of its value could still be considered a shared asset. This typically includes:

- Businesses started during the marriage: These are almost always presumed to be 100% community property.

- Businesses that grew during the marriage: What if you owned the business before you ever said "I do"? While the business itself might be your separate property, any increase in its value that came from your or your spouse's efforts during the marriage can be classified as community property.

Because of this, Texas courts require a formal business valuation. This isn't just a back-of-the-napkin estimate. It’s a detailed financial analysis performed by an expert to determine the business's fair market value. That final number becomes a key piece of the marital estate that needs to be divided. This process involves sharing incredibly sensitive financial data, which highlights the importance of strong law firm data security to protect your privacy and your assets.

This guide will break down the entire process into clear, manageable steps. We'll walk through how experts calculate a business's value, what documents you’ll need to pull together, and how you can prepare for a fair outcome. For those with high-value estates, learning about specific strategies for protecting business assets in a high-net-worth Texas divorce can offer crucial insights into safeguarding what you've built. Our goal is to give you the knowledge and confidence to move forward.

The Three Methods for Valuing a Business

Figuring out what a business is worth during a divorce can feel like trying to hit a moving target, especially when the stakes are so high. This isn't about pulling a number out of thin air; it's a structured process that financial experts use to arrive at a fair, defensible valuation. In the world of divorce, professionals primarily rely on three core methods.

Understanding how these work will empower you to follow along with your expert, ask the right questions, and feel more confident in the final number. If you want to dig deeper into the core concepts, you can explore this guide on how to value a business accurately to see these proven methods in action.

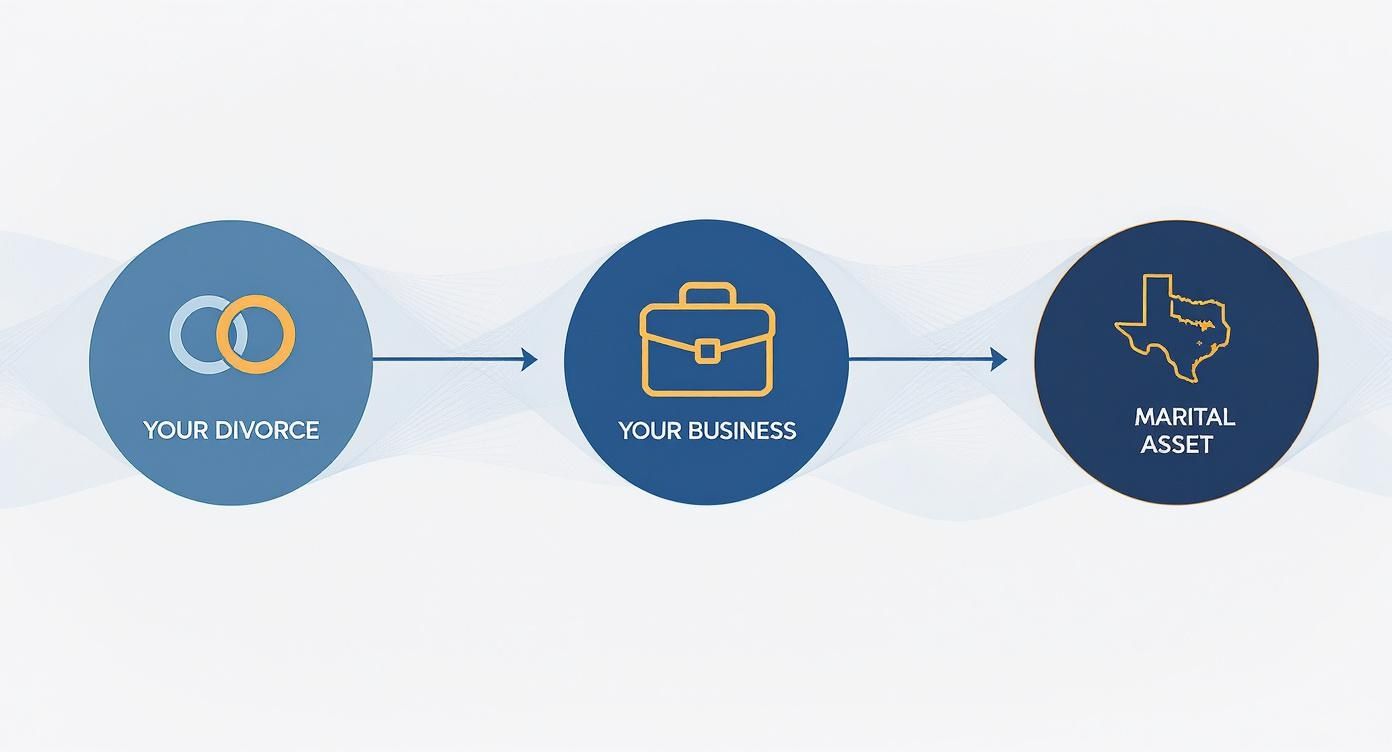

This flowchart shows the direct link between your divorce, your business, and how it becomes classified as a marital asset under Texas law.

As you can see, the moment a divorce begins, a business owned or grown during the marriage is considered part of the community estate. This makes a formal valuation not just a good idea, but a necessity.

The Income Approach

Think of the Income Approach like you're evaluating a rental property. You wouldn't just look at what similar buildings have sold for; you'd want to know exactly how much rental income it’s expected to generate in the future. This method applies the same logic to your business.

A valuation expert will analyze the business's historical earnings and cash flow to project its future earning potential. They then apply a "capitalization" or "discount" rate to figure out what those future earnings are worth in today's dollars.

This approach is particularly powerful for businesses with a solid track record of profitability, like a stable consulting firm or a thriving medical practice. Their value is directly tied to the income they consistently produce.

The Market Approach

The Market Approach is a lot like how a real estate agent prices a home. The agent doesn't guess; they pull "comps"—recent sales of similar houses in the neighborhood. For a business valuation, an expert does the exact same thing.

They research the sale prices of comparable businesses in the same industry and of a similar size. By analyzing what those businesses actually sold for, often as a multiple of their revenue or earnings, the expert can land on a realistic market value for your company.

This method is most effective when there's good, clean data available on the sales of similar private companies.

The Asset Approach

The last of the three, the Asset Approach, is the most straightforward of the bunch. Imagine you were closing down a retail store and had to sell off everything inside. You’d create a detailed inventory of all the furniture, equipment, and merchandise, add it all up, and then subtract any outstanding debts or bills.

That's exactly how the Asset Approach works. An expert calculates the fair market value of all the business's tangible assets (like vehicles, machinery, and real estate) and intangible assets (like patents or trademarks). From that total, they subtract all the business's liabilities, like loans and accounts payable.

- Total Assets: The value of everything the company owns.

- Total Liabilities: The sum of everything the company owes.

- Net Asset Value: Total Assets minus Total Liabilities.

This method is less common for profitable, ongoing businesses because it doesn't really capture the value of future income or brand reputation (often called goodwill). However, it's essential for asset-heavy businesses like manufacturing plants or real estate holding companies, or for businesses that are no longer profitable and might be worth more liquidated than as a going concern.

To help clarify when each method is most appropriate, this table breaks down their core focus and best-use cases.

Comparing Business Valuation Methods

| Valuation Method | What It Measures | Best For |

|---|---|---|

| Income Approach | The business's future earning potential | Service-based businesses with consistent profits (e.g., law firms, medical practices) |

| Market Approach | What similar businesses have recently sold for | Industries with plenty of public sales data (e.g., restaurants, retail stores) |

| Asset Approach | The net value of the company's assets | Asset-heavy businesses or companies facing liquidation (e.g., manufacturing, real estate holdings) |

Ultimately, a skilled valuation expert won't just pick one method and call it a day. They will often use a combination of these approaches, weighing each one based on the specific type of business and the quality of the available data. This blended technique provides a much more comprehensive and defensible final number for your divorce proceedings.

Why the Valuation Date Is So Important

They say timing is everything, and that’s never truer than when putting a price on your business during a divorce. The specific day chosen to value your company—the valuation date—can radically change the final number. This isn't just a minor detail; it’s a strategic decision that could be worth hundreds of thousands of dollars, directly shaping your financial settlement and future.

You might think the business would be valued on the day you filed for divorce, but in Texas, that's rarely the case. The courts here have a different approach that can make a massive difference.

How Texas Courts Determine the Valuation Date

In Texas, there isn’t a single, mandatory date for valuing assets. Instead, the Texas Family Code gives judges the flexibility to pick a date that is fair and just based on the specifics of the case. In practice, however, the most common approach is to set the valuation date as close as possible to the date of trial.

Why is this so critical? Because a business isn’t a static asset like a savings account. Its value can swing dramatically over the months—or even years—it takes for a divorce to be finalized.

A business is a living, breathing entity. Its value is influenced by market conditions, industry trends, and its own performance. A valuation is a snapshot in time, and choosing when to take that picture is one of the most critical decisions in your divorce.

Think about it this way: a construction company might be thriving during a real estate boom but struggling during a recession. If the valuation happens during the boom, its value will be high. If it's valued during a downturn, the number could be significantly lower. This is precisely why your attorney’s role in fighting for a fair valuation date is so crucial.

Real-World Examples of Fluctuating Value

The difference a few months can make is staggering. This variability is one of the biggest challenges in business valuations during a divorce. A business valued during a market slump could be worth 30-50% less than its value in a boom period, which completely changes how assets are divided. The variability makes it clear why selecting the right valuation date and method is so important, as even a small time gap can create huge discrepancies in the settlement. You can discover more insights about valuation date impacts from other family law experts.

Let's look at a couple of scenarios to see this in action:

- Scenario 1: The Restaurant A popular restaurant's value might spike during the busy holiday season but dip during the slow summer months. A valuation set for December 31st would likely show much stronger numbers than one set for July 31st.

- Scenario 2: The Tech Startup A tech company could land a major new contract, causing its projected future earnings—and its current value—to skyrocket overnight. On the flip side, if a competitor launches a superior product, the company's value could plummet just as fast.

In situations like these, one spouse will naturally argue for a date when the business was at its peak value, while the other will push for a date when it was performing poorly.

Arguing for a Fair Valuation Date

Because the "date of trial" is the standard, it's the default starting point. But what if something extraordinary happens that artificially inflates or deflates the business’s value right before trial—something that doesn't reflect its true, stable worth? In that case, your attorney can argue for a different date.

For example, if a business owner intentionally ran up debts or delayed signing a big client contract just to tank the business's value before trial, an attorney could present evidence of this behavior. They could then ask the court to use an earlier valuation date that more accurately reflects the company's true financial state. The goal is always to land on a value that is just and right, reflecting the business's legitimate financial reality.

Understanding the strategic importance of the valuation date empowers you to work with your legal team to ensure the final number is fair. It’s a key part of protecting what you’ve built and securing a stable financial footing as you move forward.

Uncovering the True Value of Your Business

A business's value isn't just what's on a tax return. When you’re facing a divorce, getting the complete financial picture is the only way to reach a fair outcome. This means looking beyond the surface-level numbers to understand two critical, and often overlooked, factors: personal goodwill and hidden or miscategorized expenses. These elements can dramatically alter the final valuation, ensuring the division of assets is based on reality, not just creative accounting.

Personal Goodwill vs. Enterprise Goodwill

One of the trickiest concepts in business valuations in divorce is "goodwill." Goodwill is the intangible value a business has beyond its physical assets—think of its reputation, customer base, and brand recognition. In Texas, the law makes a crucial distinction between two types of goodwill, and it's a distinction that can make or break a fair property division.

- Enterprise Goodwill: This is the value tied directly to the business itself. It’s the company name, its prime location, established customer lists, and solid operational systems. This value would stick around even if you, the owner, were no longer involved. Enterprise goodwill is considered a community asset and is divisible in a divorce.

- Personal Goodwill: This is the value tied directly to you—your personal skills, stellar reputation, and the relationships you've built. Think of a renowned surgeon whose patients come for them, not just the clinic, or a popular artist whose name alone sells their work. In Texas, personal goodwill is treated as your separate property and is not subject to division.

Separating these two is a vital, and often complex, task for a valuation expert. They have to carefully analyze how much of the business's success is tied to its own systems versus your personal talent and influence. Getting this calculation right is non-negotiable; it ensures your spouse doesn't receive a share of value that is inherently tied to your future work and personal earning capacity.

Adjusting for Personal Expenses and Hidden Assets

Let's be honest: many small business owners run personal expenses through the company. It's common practice for tax purposes. These might include car payments, cell phone bills, family vacations disguised as "business trips," or meals out with friends. While it may seem harmless, this practice artificially lowers the business's stated profits on paper.

During a divorce valuation, this becomes a serious problem. A lower profit suggests a lower business value, which can lead to a profoundly unfair division of assets. This is exactly where a forensic accountant becomes invaluable.

The process of adding back personal expenses to the business's income to find its true profitability is called "normalization." It provides an accurate picture of the cash flow a business truly generates, which is the foundation of a fair valuation.

A forensic accountant will meticulously comb through financial records—bank statements, credit card bills, and expense reports—to identify and add back these personal expenses. This normalization process reveals the business's actual earning power. For instance, in one documented case, a business's reported net income was $400,000, but after adjusting for $80,000 in discretionary expenses, the normalized income shot up to $480,000. That single adjustment increased the business’s valuation by 20%.

This process is also crucial for uncovering intentionally concealed income or assets. If one spouse is deliberately depressing the business’s value to gain an advantage, a thorough financial investigation is the only way to get to the truth. Our guide on identifying hidden assets in a divorce offers more detail on the red flags to watch for.

Building Your Financial Expert Team

Trying to navigate the financial maze of a business valuation during a divorce can feel like an impossible task to tackle on your own—and frankly, you shouldn't have to. Assembling the right team of financial professionals isn't a luxury; it's a strategic necessity to protect your interests and make sure the outcome is fair. This team works right alongside your attorney, bringing the specialized knowledge needed to uncover the true value of your business.

The two key players you'll almost certainly need to know are a business valuation expert and a forensic accountant. While their roles can sometimes overlap, they each serve a distinct and vital function.

The Business Valuation Expert

A business valuation expert is the professional who formally appraises your company. The easiest way to think of them is like a real estate appraiser, but for your business. Their entire job is to analyze the financials, market conditions, and how the business operates to determine a defensible fair market value. They are specialists in the three core valuation methods—income, market, and asset—and know exactly how to apply them to your specific industry.

When you're choosing a valuation expert, their credentials and experience are everything. You'll want to look for professionals with designations like:

- CVA (Certified Valuation Analyst)

- ABV (Accredited in Business Valuation)

- ASA (Accredited Senior Appraiser)

Just as important, you need an expert who has deep experience in Texas family law. Valuing a business for a potential sale is a completely different ballgame than valuing one for a divorce. An expert who has actually testified in Texas courts knows how to defend their valuation under cross-examination and how to build a report that resonates with judges.

The Forensic Accountant

If a valuation expert is an appraiser, then a forensic accountant is a financial detective. Their role is to dig much deeper into the numbers to make sure they are accurate and, more importantly, complete. A forensic accountant is absolutely essential when you suspect there might be more to the story than what the official books are showing.

They specialize in things like:

- Uncovering hidden assets or income that hasn't been disclosed.

- Identifying personal expenses being run through the business (a very common issue).

- "Normalizing" the financials to reflect the business's true profitability.

- Tracing separate versus community property funds.

If your spouse is the one controlling the business finances and you have a gut feeling you're not getting the full picture, a forensic accountant is your best advocate for financial transparency. They are the ones who provide the hard evidence needed to ensure the valuation is based on facts, not fiction.

A strong legal strategy depends on a strong financial foundation. The right expert doesn't just give you a number; they provide clarity, credibility, and confidence when you need it most.

One Expert or Two?

In your divorce, you really have two main options for bringing in these experts. You can each hire your own, or you and your spouse can agree to use a single, neutral expert. A joint expert can definitely save money and cut down on conflict, but it only works if both of you are committed to being fully transparent.

If the situation is contentious, hiring your own expert is often the best way to ensure your interests are aggressively represented. This decision is a crucial part of your overall legal strategy, which is why it's so important to find the right legal guidance from the start. To get a better handle on what to look for, you can learn more about how to choose a divorce lawyer who fits your specific needs.

Your Action Plan for a Fair Business Valuation

It's completely normal to feel overwhelmed by the sheer number of financial details involved in a divorce. This final section is designed to cut through the noise and give you a clear, step-by-step checklist to prepare for your business valuation. Think of this as your roadmap to being proactive instead of reactive. In this process, preparation is your single most powerful tool for achieving a fair outcome.

Your Immediate Next Steps

The moment divorce is on the table, the clock starts ticking. It’s time to get your financial life in order. Taking control of your documentation right away gives your legal team the solid foundation they need to build a strong case for a fair business valuation in your divorce.

Here is what you should start gathering right away:

- Financial Statements: Track down at least three to five years of profit and loss statements, balance sheets, and cash flow statements.

- Tax Returns: You'll need both personal and business tax returns going back five years.

- Bank and Loan Documents: Compile all business bank statements, loan applications, and statements for any outstanding debts.

- Corporate Records: Locate the foundational documents of your business, like your articles of incorporation, partnership agreements, or shareholder agreements.

- Major Contracts: Pull together any significant client or vendor contracts that have a real impact on the business's revenue and obligations.

This paperwork provides the raw data a valuation expert needs to even begin their analysis. Having it ready not only speeds things up but also shows you’re organized and transparent from the get-go.

Critical Mistakes to Avoid

Just as important as knowing what to do is knowing what not to do. Certain actions can torpedo your credibility in court and lead to a disastrous outcome. It's absolutely essential to avoid these common traps.

A Texas court values transparency and fairness above all else. Any attempt to hide assets or cook the books can result in severe penalties and will almost certainly crater your position in the divorce.

- Do Not Hide or Transfer Assets: Moving money to secret accounts or transferring ownership of assets to friends or family is a massive red flag. The court will find out, and the consequences will be serious.

- Avoid Making Sudden Financial Changes: Don't abruptly change how you run the business. Taking on unusual debt or selling off major assets without talking to your attorney first is a bad move.

- Don't Destroy Records: Deleting emails, shredding documents, or conveniently "losing" financial records will be viewed with extreme suspicion by the court. Don’t do it.

What to Do Next

Ensuring an accurate business valuation means you have to dig deep into the financials. It requires distinguishing between your personal value and the business's value and normalizing the income to reflect the company's true performance.

- Be Transparent with Your Attorney: Disclose any personal expenses you run through the business from the start. This allows your legal team to account for them properly and build a strong case.

- Gather Detailed Records: Collect several years' worth of bank statements, credit card records, and general ledgers that show all business spending. The more documentation, the better.

- Hire a Qualified Legal Team: If you suspect hidden assets or commingled expenses, hiring an experienced attorney isn't just a good idea—it's a necessary step toward protecting your interests.

Navigating a business valuation during a divorce is a high-stakes process where you absolutely need expert guidance. But you don't have to face this challenge alone. The experienced attorneys at The Law Office of Bryan Fagan are here to protect your business and your financial future.

We live and breathe the complexities of Texas community property law and have a network of trusted financial experts ready to ensure your business is valued accurately and fairly. The hard work you’ve put into your business deserves to be protected.

Schedule a free, confidential consultation with us today. Let us help you create a clear strategy to protect what you've built and move forward with confidence.

Frequently Asked Questions About Business Valuations

Even after breaking down the process, it’s completely normal to have more questions swirling around. This is a complex corner of divorce law, and it often brings up very specific concerns about everything from costs to disagreements, especially when a business you started long before the marriage is on the line.

Let's tackle some of the most common questions our clients ask us when it comes to business valuations in a Texas divorce.

What Happens If My Spouse and I Disagree on the Business Value?

It’s not just common—it’s practically expected. Disagreements over the final valuation number happen all the time in divorce cases. When you and your spouse each hire an expert and their numbers don't line up, the first step is for your attorneys to try and negotiate a settlement. They'll dig into the methodologies each expert used, looking for common ground or even potential flaws that could open the door to a compromise.

If negotiations or even formal mediation can’t get you to an agreement, the issue may have to be settled at trial. In the courtroom, both valuation experts will present their findings and face cross-examination. It’s then up to the judge to weigh each expert's credibility, review all the evidence, and make the final call on the business's value for the purpose of dividing your marital estate.

How Much Does a Business Valuation Cost in a Divorce?

The cost of a business valuation can swing wildly. The final price tag really depends on the complexity of the business, the state of its financial records, and, frankly, the level of conflict between you and your spouse.

- For a small, straightforward business with clean books, a valuation might run a few thousand dollars.

- For a larger company with complicated assets, multiple locations, or messy financials that need a forensic accountant to untangle, the cost can easily climb into the tens of thousands.

It’s best to think of this as a critical investment. When the business is likely your largest marital asset, getting an accurate number is essential to ensuring a fair and equitable division.

Can I Protect a Business I Started Before Marriage?

Yes, you can, but it’s not as simple as you might think. A business you owned before you said "I do" is generally considered your separate property in Texas. The catch? The law recognizes that a business can grow significantly during a marriage, often thanks to the work put in by one or both spouses.

Under the Texas Family Code § 3.001, a business owned before marriage is your separate property. However, any increase in its value during the marriage due to the time, toil, and effort of either spouse is considered community property.

That increase in value—what we call appreciation—is often classified as community property and is subject to division. This is why a comprehensive business valuation is still necessary. An experienced attorney can help you trace and shield the separate property portion while ensuring the community share is divided fairly and justly, protecting the legacy you built from the very beginning.

The complexities of business valuations in divorce demand a legal team with both financial savvy and a compassionate approach. At The Law Office of Bryan Fagan, PLLC, we have the experience and resources to protect your business interests and guide you toward a secure future. Don’t try to handle this challenge alone. Schedule a free, confidential consultation with us today by visiting https://texasdivorcelawyer.us to create a clear strategy for protecting what you’ve built.