Skip to content

Skip to content Losing your home during a divorce can feel like the ground is shifting beneath your feet. But it doesn't have to be that way. The good news for many Texans is that you can often assume the mortgage after a divorce, which allows you to take over the existing loan, keep its terms—and most importantly, hold onto that favorable interest rate you locked in years ago.

Can You Keep The House After A Texas Divorce?

The thought of leaving your family home adds another heavy layer of stress to an already emotional time. For so many of us, the house is more than just a line item on a spreadsheet; it's where memories were made and your kids grew up. The big question is: how can you stay without having to start from scratch with a new, much more expensive mortgage?

Understanding Mortgage Assumption in Texas

A mortgage assumption is a formal process where one spouse takes over the entire home loan. It's not the same as refinancing, where you're getting a completely new loan. Instead, you are stepping into the original agreement and inheriting everything that comes with it:

- The Original Interest Rate: This is the biggest win, especially if you secured a rate far below what the market offers today.

- The Remaining Loan Balance: You pick up right where you and your ex left off, taking over the existing debt.

- The Existing Repayment Schedule: The end date of your loan doesn't change.

This process is absolutely critical for truly separating your financial lives. The end goal is to get the lender to issue a "Release of Liability" for your ex-spouse, which officially takes their name off the loan and removes their legal obligation to pay.

Why This Matters in Your Divorce

In Texas, the family home is usually the most significant piece of community property, so how it's divided has to be handled with care. Under the Texas Family Code, community property is everything you and your spouse acquired during the marriage, and it must be divided in a "just and right" manner. Assuming the mortgage is a smart, strategic way to manage this major asset while keeping some stability for you and your family. A recent study actually found that 53.4% of divorced individuals in the U.S. co-owned their homes, making this a common and critical challenge to overcome. For a deeper dive into how property is divided in Texas, check out our comprehensive guide to Texas divorce property division.

One of the most common mistakes I see is when couples think just removing an ex-spouse from the property deed is enough. The deed is about ownership, but the mortgage is a totally separate contract with the bank. Without a formal assumption or refinance, your ex is still legally on the hook for the debt, and their credit is at risk.

Making this happen involves getting the lender's approval, using specific legal language in your divorce decree, and having a clear picture of your own financial health. It takes some planning, but successfully assuming your mortgage can secure your home and give you a solid foundation for your financial future. If you're interested in the data, you can find additional insights about marital home ownership here.

Mortgage Assumption vs. Refinancing in a Divorce

Deciding what to do with the house in a divorce often comes down to two paths: assuming the current mortgage or refinancing into a totally new one. They might sound similar, but the financial ripple effects are massive, especially when today's interest rates are so much higher than they were just a couple of years ago. The choice you make here will shape your monthly budget for years to come.

Getting clear on the fundamental difference is your first step. One option lets you hang on to a fantastic interest rate you already have, while the other means starting from scratch with a brand-new loan at today's much higher market rates.

The Core Difference Explained

A mortgage assumption is like taking over someone's car lease. You step directly into the original loan agreement, keeping the exact same terms—the interest rate, the monthly payment, and the remaining time on the loan. The whole point is for you to become the sole borrower and get your ex-spouse formally released from any and all financial responsibility for the debt.

A mortgage refinance, on the other hand, is a completely new loan. This new mortgage pays off and closes out the old joint one forever. That means you'll have a new interest rate, a new monthly payment, and a brand-new repayment schedule.

When you're staring down major financial decisions like this, having a structured way to think through it can be a lifesaver. For anyone looking to sharpen their financial planning skills, mastering the financial decision-making process offers some really helpful frameworks.

Why Assumption Often Wins

The biggest reason to assume a mortgage after a divorce is simple: preserving a low interest rate. If you locked in a rate around 3% a few years ago, refinancing into a new loan at today's 7% could jack up your monthly payment by hundreds, or even over a thousand, dollars.

Consider this real-world scenario: A $300,000 mortgage at 3% has a principal and interest payment of about $1,265. If you were to refinance that same $300,000 at 7%, the payment would jump to nearly $2,000. That's a staggering difference of over $700 every single month.

Assumption lets you dodge that "payment shock," making it a much more affordable way to keep the family home. You'll also typically find that the closing costs are lower than a full refinance, saving you a nice chunk of money right at the start.

When Refinancing Becomes Necessary

While assumption is often the smarter financial move, it has one major drawback: it doesn’t give you cash. If you need to buy out your ex-spouse's share of the home's equity, a simple assumption won't get you the funds to do it.

This is where refinancing becomes the practical, and sometimes only, choice. A "cash-out" refinance lets you borrow against the home's equity, giving you the money needed to pay your former spouse what they're owed. The new, larger loan will be entirely in your name, which satisfies the requirements of the divorce decree.

The trade-off is pretty clear. You solve the equity buyout problem, but you're taking on a brand-new loan, almost certainly at a much higher interest rate and with higher closing costs. Solid financial planning is absolutely critical here; for more tips, you can dig into our guide on planning your finances for a divorce in Texas.

Comparing Your Two Paths

To make the best call for your situation, you need to see how these two options stack up side-by-side. The table below breaks down the key differences to help you see what each path really means for your financial future.

| Factor | Mortgage Assumption | Mortgage Refinancing |

|---|---|---|

| Interest Rate | Keeps the original, often lower, interest rate of the existing loan. | Replaces the old loan with a new one at current market rates, which are likely higher. |

| Monthly Payment | Your principal and interest payment remains exactly the same. | Your monthly payment will almost certainly increase due to the higher interest rate. |

| Closing Costs | Significantly lower, typically involving just an assumption fee. | Higher, as it includes standard closing costs for a new loan (origination fees, appraisal, title, etc.). |

| Equity Buyout | Does not provide funds to buy out your ex-spouse's equity. This must be handled separately. | Allows you to borrow against home equity to fund the buyout as part of the new loan. |

| Main Benefit | Affordability. Preserves a low payment, making it easier to qualify and manage post-divorce. | Liquidity. Solves the problem of paying your ex-spouse their share of the home's value. |

Ultimately, your decision will hinge on your financial priorities and the specific terms hammered out in your divorce settlement. Do you need to lock in the lowest possible monthly payment, or is freeing up equity for the buyout your most pressing concern? Answering that question will point you in the right direction.

Your Action Plan for Assuming a Mortgage in Texas

Facing the practical steps of a mortgage assumption can feel overwhelming, but it's a journey you can absolutely navigate with the right map. This is your step-by-step guide to move you from uncertainty to confident action. We'll break down exactly what you need to do, from that first call to the lender to securing the final document that separates your financial futures for good.

The path forward begins with a simple question: can your loan even be assumed? From there, it's all about proving you have the financial strength to carry the mortgage on your own.

Step 1: Confirm Your Mortgage Is Assumable

Before you get too far down this road, you have to find out if your mortgage is even assumable. The good news is that many common loan types are designed with this exact possibility in mind.

You'll generally find that government-backed loans are your best bet:

- FHA Loans

- VA Loans

- USDA Loans

These loans are almost always assumable, as long as you meet the lender's qualifications. But what if you have a conventional loan? Most of those include a "due-on-sale" clause, which sounds like a deal-breaker.

Don't worry. A crucial piece of federal law, the Garn-St. Germain Act, provides a powerful exception specifically for divorce. This law stops lenders from calling the loan due when a house is transferred to a spouse in a divorce. This gives you a clear legal path to assume the mortgage after divorce, even with a conventional loan, provided you can qualify for it on your own.

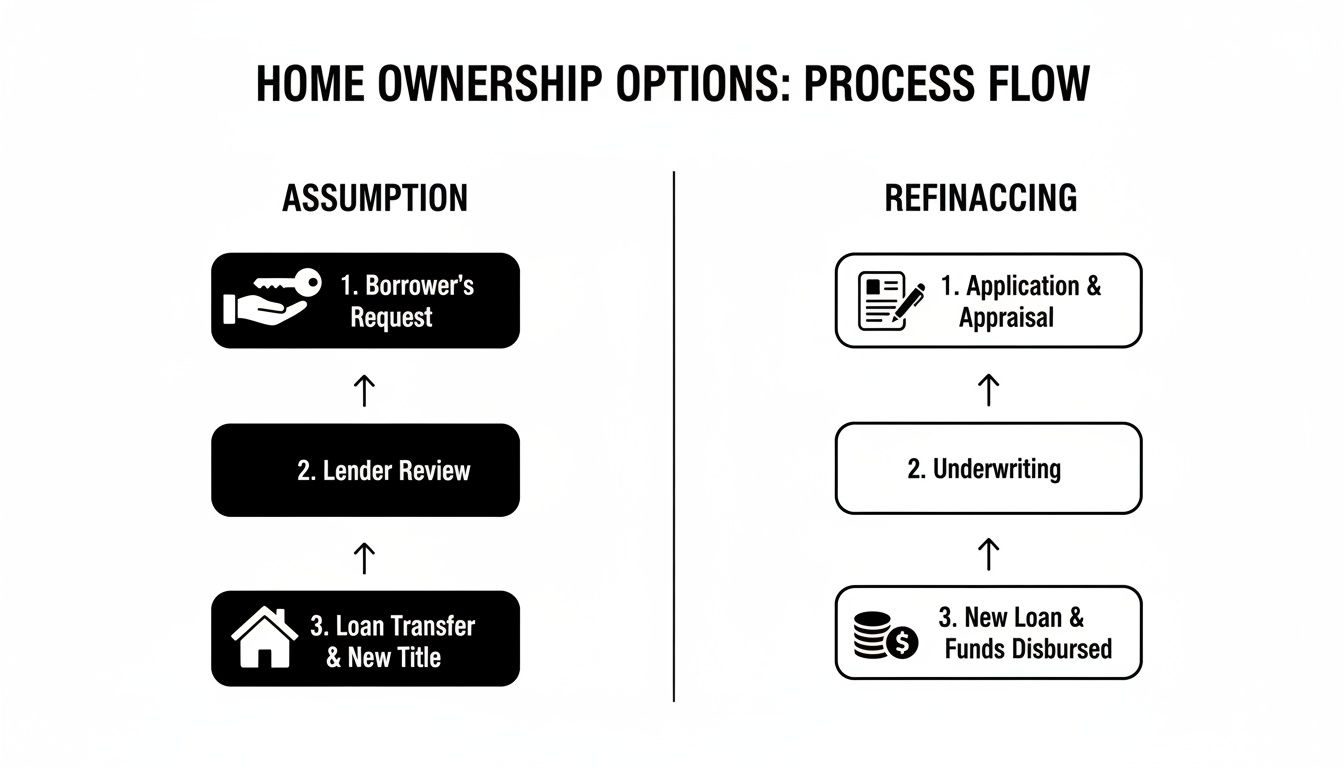

This side-by-side comparison shows the typical process for both a mortgage assumption and a refinance.

The key takeaway here is that while both paths lead to you owning the home by yourself, the assumption process is designed to keep your existing loan terms intact. Refinancing, on the other hand, means starting over with a brand-new loan.

Step 2: Gather Your Financial Documentation

Once you've confirmed your loan is likely assumable, the lender will need to see proof that you can handle the payments solo. They're going to re-underwrite the loan with you as the only borrower. Think of it like applying for a new mortgage, but for the house you already live in.

Start gathering these documents now to get ahead of the game:

- Proof of Income: Typically, this means your last two years of W-2s, your most recent pay stubs, and recent tax returns. If you're self-employed, be ready to provide profit and loss statements.

- Asset Statements: Round up recent statements from all your bank accounts (checking and savings), retirement accounts like your 401(k) or IRA, and any other investment accounts.

- Debt Information: Make a clear list of all your monthly debts—car loans, student loans, credit card payments, etc. The lender is going to pull your credit report, of course, but having this list helps you see your own financial picture clearly.

- Your Divorce Decree: The lender will need a copy of the finalized, signed decree that officially awards you the house and states that you will be assuming the mortgage.

Your debt-to-income (DTI) ratio is the magic number here. It's the percentage of your gross monthly income that goes toward paying your monthly debts. Lenders have strict DTI limits, and proving you meet them on your own is the single biggest hurdle to getting approved.

Step 3: Navigate the Formal Application and Underwriting

With your documents in hand, you'll submit a formal assumption application to your lender. This is what officially kicks off the underwriting process, where the lender's team digs in to verify your financial stability.

Be prepared for this to take time. In Texas, the process often takes anywhere from 60 to 120 days after your divorce is final.

Communication is everything during this waiting period. Stay in touch with your loan processor and respond immediately to any requests for more information. Delays often happen because of missing paperwork, so staying organized and responsive will keep things moving.

Step 4: Secure the Release of Liability

This is it—the final and most important step in the entire process. Once the lender approves your assumption application and you've signed all the final paperwork, they will issue a Release of Liability.

This legal document is your golden ticket. It officially removes your ex-spouse's name from the mortgage, permanently severing their legal and financial obligation to the debt. Without this document, your ex is still on the hook, and their credit remains tied to your house.

Getting that Release of Liability is non-negotiable. It protects your ex-spouse’s financial future and solidifies your sole ownership of, and responsibility for, the home. Make sure you receive a physical copy of this document and store it safely with your divorce decree and property deed. It's the proof that you successfully completed your action plan.

How Your Divorce Decree Protects Your Financial Future

Relying on a handshake deal or a verbal promise about the house is one of the most dangerous financial mistakes you can make in a divorce. Your Final Decree of Divorce isn't just another piece of paper—it's a court order. It is your single most powerful tool for protecting your financial future.

When you're dealing with something as massive as a mortgage, getting precise, enforceable language in that decree isn't just a good idea. It's an absolute necessity. This legal document is what turns your agreement into a binding obligation, removing all ambiguity and protecting your credit and legal rights to the property.

Why Vague Language Is Your Enemy

Leaving the terms of a mortgage assumption open to interpretation is a recipe for disaster. I've seen it happen time and again. Ambiguous wording like, "Spouse A will take over the mortgage payments," is completely inadequate and legally toothless. It doesn't set a firm deadline, fails to mention the critical Release of Liability, and gives you no recourse if your ex-spouse simply ignores the agreement.

Your divorce decree has to be a clear, actionable roadmap. It needs to leave zero room for confusion or delay. That legal clarity is your primary safeguard against being financially tangled with your former partner for years to come. The current economic climate has made this legal precision more vital than ever. For a deeper dive into these economic pressures, you can explore detailed insights on divorce and mortgages at Attorney at Law Magazine.

Essential Clauses Your Texas Divorce Decree Must Include

To effectively protect both you and your ex, your attorney will draft specific language that covers every potential outcome. Think of these clauses as the legal armor defending your financial well-being.

Your decree should contain several non-negotiable elements:

- Formal Award of the Property: The decree must explicitly state that you are being awarded the house as your "sole and separate property." This is the exact language that allows you to present the decree to the lender as proof of your ownership rights.

- A Firm Deadline for Assumption: You need a clear, non-negotiable deadline for completing the mortgage assumption or refinance. A typical and reasonable timeframe is 90 to 180 days from the date the judge signs the decree.

- Securing the Release of Liability: The language must explicitly require that your ex-spouse be released from all liability on the mortgage debt. This is the clause that protects their credit and officially severs their financial ties to the home.

- A "What-If" Plan: What happens if the lender denies your application or you can't meet the deadline? A well-drafted decree includes a contingency plan, which often triggers a forced sale of the home if the assumption fails.

A common contingency clause might state: "If the assuming spouse fails to secure the release of the other party's liability by the specified date, the property shall be listed for sale with a licensed real estate agent within 15 days." This creates a clear and immediate consequence for inaction.

Enforcing the Terms of Your Decree

Even with the strongest language, sometimes an ex-spouse might refuse to cooperate. They might drag their feet or refuse to sign necessary paperwork. This is where the power of a court order comes into play. Because your decree is legally binding, you are not left without options.

If your ex-spouse fails to comply with the terms related to the house, you can take them back to court. By filing a legal action to compel them to follow the judge's orders, you can force the process to move forward. If you find yourself in this situation, it is crucial to understand your rights. You can learn more about this legal process by reviewing our guide on filing a Motion to Enforce in Texas. This is your legal remedy to hold your ex-spouse accountable to the exact terms you both agreed upon.

Solving Common Mortgage Assumption Roadblocks

Even with the best-laid plans, trying to assume a mortgage during a divorce can hit some seriously frustrating snags. What happens if your ex just won't sign the paperwork? Or worse, what if the lender flat-out denies your application?

These moments can feel like the end of the road, but they’re not. They're just problems that demand a new strategy. Knowing your legal and financial options ahead of time is your best defense.

When Your Ex-Spouse Won't Cooperate

One of the most stressful roadblocks I see is an ex-spouse who drags their feet or outright refuses to cooperate. They might not sign the deed, fail to provide documents the lender needs, or just generally stall the whole process your divorce decree clearly laid out.

Here's the good news: you are not stuck. Your Final Decree of Divorce is a legally binding court order, and their refusal to comply is a direct violation of it.

Your next move is to file a Motion for Enforcement with the court. This is a legal action that essentially asks the judge to force your ex-spouse to follow the decree's terms. A judge can order them to sign the documents and may even make them pay your attorney's fees for having to file the motion in the first place. It’s a powerful tool to hold a non-cooperative party accountable.

If the Lender Denies Your Application

Getting a denial letter from the lender is a gut punch, especially after you've jumped through all the hoops. Most often, a denial comes down to your individual income not meeting the lender’s strict debt-to-income (DTI) ratio requirements. But a "no" today doesn't have to mean "never."

You have a few strategic paths forward:

- Bring in a Co-Signer: A creditworthy family member, like a parent or sibling, could co-sign the assumption with you. Their income can help you get over the DTI hump, but just remember—they are now legally on the hook for the loan if you can't pay.

- Renegotiate the Asset Split: It might be time to go back to the negotiating table (or mediation) to rework the property division. Maybe you can trade another asset, like a slice of a retirement account, in exchange for your ex leaving more cash in the estate to help you qualify on your own.

- Sell the Home: This is often the last resort, but sometimes it's the only practical option if you simply can't qualify to assume or refinance. A well-drafted decree should already have a contingency clause for this scenario, ensuring a clear process for listing the house and dividing the proceeds without more conflict.

As you plan your financial future, it's also smart to understand strategies for avoiding severe financial outcomes like foreclosure if major challenges come up.

The Unique Hurdles of a "Gray Divorce"

The rise in "gray divorces"—couples splitting up after 50—introduces its own set of challenges for mortgage assumptions. These situations can wreak havoc on retirement plans. A recent study found that 56% of married Americans believe a divorce would completely derail their financial security.

Lenders can get particularly nervous about approving an assumption based on a single, fixed income from sources like a pension or Social Security. You can learn more about how divorce can impact retirement security from Allianz Life.

If you're in this boat, don't lose hope. There are creative solutions. We can explore using other assets to demonstrate financial stability or even structure spousal support payments in a way that lenders will recognize as qualifying income. You still have strategic options.

What to Do Next: Your Key Takeaway

Getting through a mortgage assumption during a divorce is a marathon, not a sprint. We've walked through the legal hoops, financial qualifications, and common roadblocks you're likely to face. Now it's time to put that knowledge into practice and start securing your future. The good news? You don't have to figure this out alone.

Your Immediate To-Do List

To keep things moving forward, focus on these critical next steps. Think of this as your game plan to stay organized and proactive:

- Dig Out Your Mortgage Paperwork: First thing's first—find out if your loan is assumable. If it's an FHA, VA, or USDA loan, you're in a good position. If it’s a conventional loan, you'll be relying on federal law to make your case.

- Talk to a Family Law Attorney: This is non-negotiable. You need to make sure your divorce decree contains the exact, ironclad language required to protect you from future liability.

- Start Gathering Your Financials: Don't wait until the lender asks. Start pulling together recent pay stubs, tax returns, and bank statements now. Being prepared will make the whole application process smoother.

Don't Skip the Most Important Step

Trying to handle a mortgage assumption on your own is one of the biggest financial risks you can take in a divorce. The choices you make in the coming weeks will directly impact your financial stability for years. Getting solid legal advice isn't a luxury—it's essential protection.

We understand this is a stressful, uncertain time. The single most important thing you can do right now is get advice tailored to your specific situation. We invite you to schedule a compassionate, no-strings-attached consultation with The Law Office of Bryan Fagan, PLLC. Our experienced Texas family law attorneys are here to help you protect your home, your finances, and your peace of mind.

Common Questions About Mortgage Assumptions

When you're trying to figure out a mortgage assumption during a divorce, a lot of specific questions pop up. Let's tackle some of the most common ones we hear from our clients right here in Texas.

How Long Does a Mortgage Assumption Take in Texas?

The timeline can vary, but you should plan on it taking anywhere from 60 to 120 days after the judge has signed your final divorce decree.

The speed really comes down to your lender, how quickly you get them all the financial paperwork they ask for, and how backed up their underwriting department is. This is exactly why we insist on writing a firm deadline into the divorce decree—it holds everyone accountable and keeps the process moving.

What Happens if My Ex-Spouse Files for Bankruptcy?

This is a scenario you absolutely want to avoid. If your ex's name is still on the mortgage and they declare bankruptcy, you're looking at some serious legal and financial trouble. Even if their personal obligation to pay the mortgage gets wiped out in their bankruptcy, the bank's lien against your home does not disappear.

The bottom line is the lender could still foreclose on your house if payments are missed. This really drives home why getting a formal "Release of Liability" through a mortgage assumption isn't just a good idea—it's essential for protecting your home.

Can I Get My Ex Off the Deed Without an Assumption?

Yes, you can, and this is one of the most dangerous misconceptions in a divorce. Removing your ex-spouse from the property deed is fairly simple with a document called a Special Warranty Deed.

But here's the catch: the deed only handles ownership. It does absolutely nothing to take their name off the mortgage loan.

They are still 100% on the hook for the entire debt in the eyes of the lender. Any late or missed payments will tank their credit score right along with yours. The deed and the mortgage are two completely separate legal contracts, and both have to be handled properly to truly untangle your financial lives.

At The Law Office of Bryan Fagan, PLLC, we help Texas families protect their homes and their futures with clarity and confidence. If you're facing a divorce and have questions about your mortgage, schedule a free consultation with our experienced attorneys today at https://texasdivorcelawyer.us.