Skip to content

Skip to content Facing a divorce means confronting the division of everything you've built together, and for many, that includes your retirement savings. In Texas, any portion of a 401(k) earned during your marriage is considered community property, meaning your spouse has a legal claim to a fair share, no matter whose name is on the account. Understanding this single concept is the first step toward protecting your financial future.

Your Financial Future and the 401k Divorce Split

It’s completely normal to feel protective of the money you’ve worked so hard to save. For many Texas families, a 401(k) is their largest asset right after the family home. The good news is that Texas law provides a clear, structured path for dividing these accounts fairly, so you’re not left guessing.

The entire process boils down to a few key terms you'll hear over and over again.

Community Property vs. Separate Property

In Texas, anything you acquire from the day you say "I do" until the day the divorce is final is community property. This includes all contributions you made to your 401(k), any employer matches you received, and all the investment growth that happened during that time. It all goes into the marital pot to be divided.

On the other hand, separate property is anything you owned before the marriage. So, the balance in your 401(k) on your wedding day is yours to keep. The catch? You have to prove it with clear documentation, which can sometimes be tricky. Any gifts or inheritances you received during the marriage also count as separate property.

The QDRO: Your Most Important Tool

This is where the magic happens. A Qualified Domestic Relations Order (QDRO) is the legal document that makes the 401k split during divorce possible. It’s a special court order—completely separate from your actual divorce decree—that tells the 401(k) plan administrator exactly how to divide the account.

Without a QDRO, trying to pull money out of a 401(k) to pay your ex-spouse would trigger massive taxes and early withdrawal penalties. The QDRO is the key that unlocks the account and lets the funds be transferred without those nasty consequences.

Here’s a quick table to help you keep these terms straight. You'll be hearing them a lot, so it's good to have a cheat sheet.

Key Terms for Your Texas 401k Division

| Term | What It Means for You in Texas |

|---|---|

| Community Property | All assets and debts acquired from the date of marriage until the divorce. Your 401(k) contributions and growth during this time fall into this category. |

| Separate Property | Assets you owned before the marriage or received as a gift or inheritance during it. Proving this requires solid financial records. |

| Qualified Domestic Relations Order (QDRO) | A court order, separate from your divorce decree, that instructs the 401(k) administrator on how to divide the account without tax penalties. |

| Alternate Payee | The non-employee spouse who is receiving a portion of the 401(k) funds. In this case, that's your ex-spouse. |

| Plan Participant | The employee whose name is on the 401(k) account. |

Think of these terms as the basic vocabulary you'll need to navigate the process confidently.

Protecting Your Long-Term Security

Dividing a 401(k) isn't just about splitting a number on a statement today; it's about rebuilding your financial foundation for tomorrow. This is especially true if you are divorcing later in life. A divorce can halve your retirement assets while doubling your living expenses. That reality makes a careful, strategic approach absolutely critical.

Since a 401(k) is built for the long haul, now is the perfect time to get familiar with proven long-term investing strategies. It helps shift your focus from what's being lost today to how you can grow your share for a secure retirement.

At The Law Office of Bryan Fagan, we see this process not as losing half of your savings, but as securing the portion you are entitled to so you can move forward with confidence. We are here to ensure every step is handled with precision to protect your nest egg.

How Texas Community Property Law Affects Your 401k

It’s a deeply unsettling feeling to watch your retirement savings, something you’ve worked years to build, become a point of contention in a divorce. Many people believe a common and painful myth: that the 401k is yours alone just because your name is on the account. In Texas, the law sees things very differently. Getting a handle on this perspective is the first step toward protecting your financial future.

Texas is a community property state, a legal framework that completely shapes how assets are divided in a divorce. The core idea is straightforward: anything you or your spouse earned or acquired from the day you said "I do" until the day the divorce is finalized belongs to the "marital estate." This doesn’t just mean the house or the cars; it absolutely applies to your retirement accounts.

The Marital Estate and Your 401k

Every single dollar you contributed to your 401k during your marriage is considered community property. This also includes any employer matching funds you received and, just as importantly, all the investment gains and interest that built up on those marital contributions.

The law treats your marriage as a partnership. Both spouses are seen as contributing to the household's financial health, regardless of who was the primary wage earner. Because of that, the growth of the retirement account during that partnership is considered a joint asset. If you want to dive deeper into this concept, you can learn more about how community property in Texas works in our detailed guide.

Tracing Your Separate Property

So, what about the money you had in your 401k before you got married? That portion, and only that portion, is considered your separate property and isn't up for grabs.

However, there’s a catch. The burden of proof is entirely on you to clearly and convincingly trace those funds. This isn’t a casual process—it means you must provide hard documentation, like old account statements, showing the exact value of the account on your wedding day.

This is where things can get messy. Over a long marriage, separate and community funds can easily get mixed together, making it tough to distinguish the investment gains on your separate property from the gains on the community portion.

Under the Texas Family Code, the law starts with the assumption that all property is community property. It's up to you to present "clear and convincing evidence" to overcome this assumption and prove a piece of your 401k is separate.

Let’s walk through a real-world example to see how this actually works.

A Practical Scenario: 15 Years of Marriage

Imagine Sarah had $50,000 in her 401k when she married David. Over their 15-year marriage, she kept contributing, and her employer offered a generous match.

By the time they filed for divorce, the account had grown to $300,000. How does the court split this?

-

Identify Separate Property: Sarah’s pre-marital balance of $50,000 is her separate property. She’ll need to track down account statements from around the time of the wedding to prove this amount.

-

Calculate the Community Portion: This is the total value minus her separate property.

- $300,000 (Total Value) – $50,000 (Sarah's Separate Property) = $250,000 (Community Property Portion)

-

Divide the Community Property: This $250,000 belongs to the marital estate. Texas law requires a "just and right" division, which very often means a 50/50 split.

- $250,000 / 2 = $125,000 for David

In this scenario, David would be entitled to $125,000 from the 401k. Sarah would keep her $50,000 separate property plus her half of the community funds, for a total of $175,000. This example highlights how the part of the 401(k) built up during the marriage is considered a marital asset and gets divided.

Without the right legal guidance, it's incredibly easy to make a mistake in this calculation—a mistake that could cost you tens of thousands of dollars from your retirement nest egg.

Untangling Your 401k with a QDRO

Watching your retirement savings get caught up in a divorce is frustrating, to say the least. This is your future we’re talking about. But there's a specific, powerful tool designed for this exact situation: the Qualified Domestic Relations Order, or QDRO. Don't think of it as just another legal form—it's a specialized court order that is absolutely essential for a clean 401k split during divorce.

A QDRO is a legal command, completely separate from your final divorce decree, that tells your 401k plan administrator exactly how to divide the account. Its main job is to let the funds move to your ex-spouse (who the law calls the "alternate payee") without triggering a massive tax bill for you.

Without a properly executed QDRO, trying to split the account would be seen as a taxable distribution in your name. That’s a mistake that could easily cost you thousands in income taxes and early withdrawal penalties.

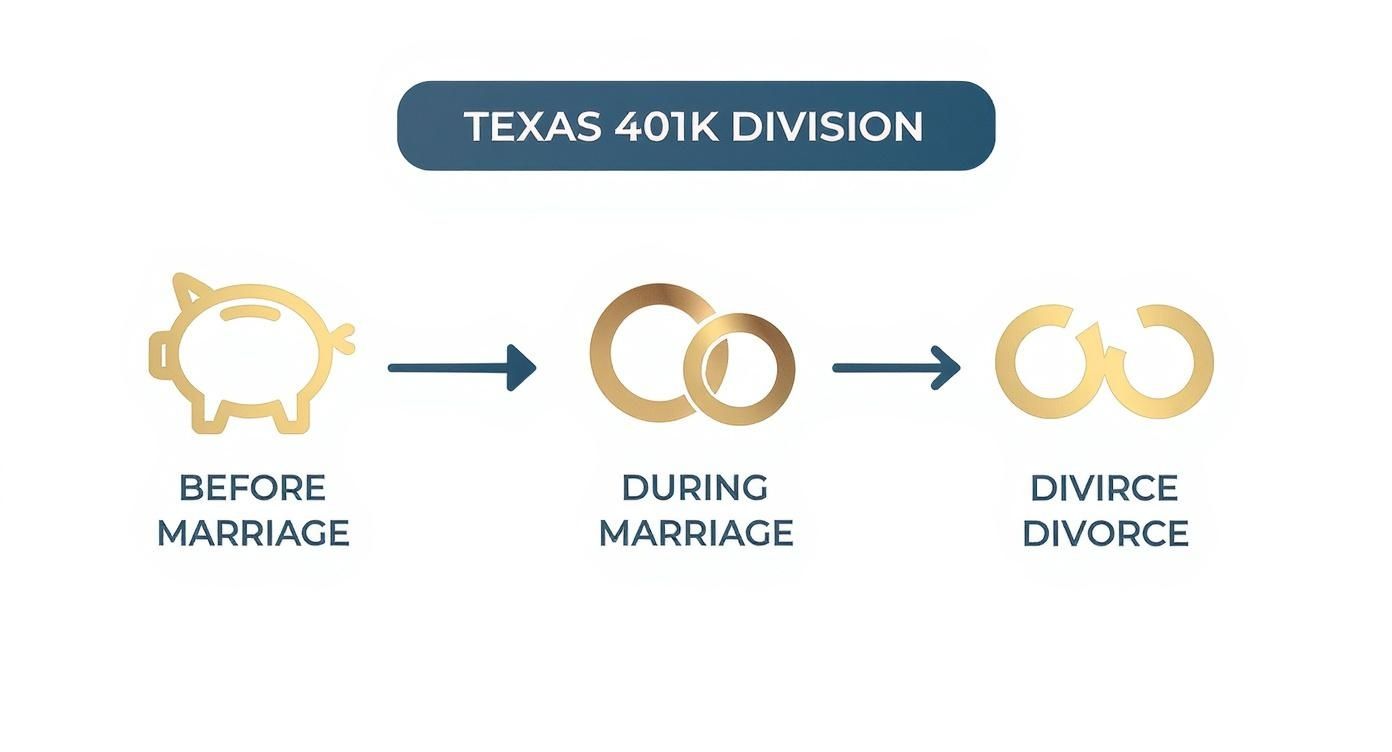

The infographic below breaks down how your 401k funds are viewed under Texas law—from your contributions before the marriage to the final division.

As you can see, your pre-marital savings are generally safe, but any growth that happened during the marriage is considered community property and is on the table for division.

Who Actually Drafts the QDRO?

This is a critical point that trips up many people. A QDRO is a highly technical legal document, not something you can just download and fill out. In fact, many divorce attorneys will bring in a third-party QDRO specialist or a dedicated firm that does nothing but draft these orders.

Why the specialization? Every single 401k plan has its own unique rules and picky requirements for what must be in a QDRO. The language has to be incredibly precise to comply with both the plan's internal rules and federal law—specifically, the Employee Retirement Income Security Act of 1974 (ERISA). A single wrong phrase can cause the plan administrator to reject the order, sending you right back to the drawing board.

The Make-or-Break Details a QDRO Must Contain

For a plan administrator to even look at a QDRO, it needs to contain specific, non-negotiable information. Think of it as a detailed instruction manual that leaves zero room for error.

- Complete Participant and Alternate Payee Information: We're talking full legal names, last known mailing addresses, and Social Security numbers for both you and your ex-spouse.

- Exact Plan Identification: The order must name the specific 401k plan it applies to. Big companies often have several retirement plans, so getting this right is vital.

- Division Method and Amount: The QDRO has to state either the exact dollar amount or the exact percentage of the account being transferred. It also needs to lock in the specific date used for valuing the account.

- Timeline and Form of Payment: It needs to spell out how and when the payment will be made, whether it's a lump-sum check or a direct rollover into another retirement account.

This document is just one piece of the puzzle. For a bigger picture of all the paperwork involved in a Texas divorce, take a look at our complete guide to essential divorce documents, which is packed with useful checklists and tips.

The Step-by-Step QDRO Process in Texas

Once the QDRO is drafted, it has to go through a strict approval pipeline, and it's not always fast. Here is a step-by-step breakdown of how it works:

- Drafting and Review: First, an attorney or specialist drafts the order based on what was agreed upon in your divorce decree.

- Submission to Plan Administrator: Here's a pro tip: Before it ever sees a judge, a draft is often sent to the 401k plan administrator for a pre-approval review. This is a crucial step to catch any mistakes that would cause an official rejection down the road.

- Signatures and Court Filing: Once pre-approved, you, your ex-spouse, and your lawyers will sign it. It’s then filed with the court and signed by the judge, making it an official court order.

- Final Submission and Execution: The official, court-certified QDRO is sent back to the plan administrator. They will then formally approve it and segregate the funds into a separate account for your ex-spouse.

The entire QDRO process, from the first draft to the final distribution of funds, can easily take several months. This is exactly why getting it drafted correctly the first time isn't just about convenience—it's a financial necessity.

One of the key benefits of using a QDRO is that it typically allows the receiving spouse to access the funds without paying the usual 10% early withdrawal penalty. Getting familiar with the rules around penalty-free 401k withdrawals can give you some helpful context as you start mapping out your own financial future.

How to Value and Divide Your Retirement Account Fairly

That number on your 401(k) statement looks so concrete, doesn't it? But when you're in the middle of a divorce, it's anything but stable. The stock market’s daily rollercoaster means the value of your retirement account can swing wildly from the day you file for divorce to the day the judge finally signs the decree. This creates a huge challenge: how can you possibly agree on a fair value for a moving target?

This isn't just a minor detail—it's a critical point of negotiation. Your 401(k) is a living asset, growing and shrinking with the market. For couples who have been married a long time, the stakes are even higher. The market has seen incredible long-term growth, so an account started decades ago could be one of the largest assets you own, making an accurate valuation absolutely essential.

Choosing a Valuation Date

One of the first practical hurdles you and your spouse will have to clear is picking a valuation date. This is the specific date you'll use to establish the account's value for the purpose of the split. There’s no single "correct" date; the best choice really depends on the specifics of your situation and Texas court processes.

Here are a few common options you'll likely consider:

- The Date of Filing: The day the original divorce petition was officially filed with the court.

- The Date of Separation: The day you and your spouse physically stopped living together as a married couple.

- The Date of Mediation: A date you both agree on during your mediation sessions, a common practice in Texas divorce.

- The Date of Final Decree: The day your divorce becomes official.

Picking a date in the past gives you certainty, but it completely ignores any market gains or losses that have happened since. On the other hand, choosing a future date, like the day your divorce is finalized, feels more current but introduces a lot of uncertainty into your negotiations.

Fixed Dollar Amount vs. Percentage Split

Once you've settled on a valuation date, the next big question is how to actually divide the money. You generally have two ways to go, and each one comes with major financial consequences.

A fixed dollar amount seems simple enough. For example, if the community property portion of the 401(k) is valued at $200,000, you might agree that your spouse gets exactly $100,000. It’s predictable, but it can also be incredibly unfair. If the market takes off while the QDRO is being processed, your spouse still only gets their $100,000, and you get to keep all the gains. But what if the market tanks? You’re still on the hook for that full $100,000, even if the account is now worth much less.

A percentage split is almost always the more equitable path. By agreeing to a percentage (say, 50% of the community portion), both of you share in any market ups and downs that happen between the valuation date and the day the funds are actually distributed. This method ensures the final split truly reflects the account's value at the time it happens.

Key Takeaway: A percentage-based division automatically adjusts for market volatility. This approach protects both spouses from the risk of a market downturn and ensures both benefit from any growth, making it a fairer method for a 401k split during divorce.

What About an Outstanding 401k Loan?

It's common for people to take out loans against their 401(k)s. If there's an outstanding loan, it’s treated as a marital debt, and it directly reduces the net value of the account available for division.

For instance, if the community portion of your 401(k) is $100,000 but you have a $20,000 loan against it, the net value for division is only $80,000. Your divorce decree has to be crystal clear about how that debt is handled—whether it’s assigned to one person or considered a shared responsibility. Ignoring this can open the door to serious financial arguments long after you think the divorce is over. Getting a handle on these financial complexities is critical, and our guide to surviving the financial storm of divorce and retirement can offer more clarity.

Common Pitfalls When Dividing a 401k

Knowing the rules for splitting a 401(k) in a divorce is your best defense against a mistake that could torpedo your financial security. The path is littered with potential missteps, but once you know what they are, you can sidestep them and protect the retirement funds you've worked so hard to build.

Every error, from a poorly drafted legal document to a simple oversight after the divorce is final, can have lasting consequences. Let’s walk through the most frequent mistakes we see and, more importantly, how you can avoid them.

The Dangers of a Generic QDRO Template

In an effort to save money, it’s tempting to search online for a "QDRO template" or even try to draft this document yourself. I can't stress this enough: this is one of the most financially dangerous mistakes you can make. A QDRO isn't a simple fill-in-the-blank form. It’s a complex legal order that has to meet the strict, unique requirements of your specific 401(k) plan and federal law.

Plan administrators are notorious for rejecting QDROs with even the slightest errors in language or formatting. A rejected order means you have to go back to court, which will cost you a significant amount of time and legal fees.

What you should do instead: Always have your QDRO drafted by an attorney with specific experience in this area. Many family lawyers work with QDRO specialists to ensure the document is perfect before it’s ever submitted. That upfront investment prevents costly delays and ensures your retirement assets are divided correctly the first time.

Cashing Out Instead of Rolling Over

When your ex-spouse receives their share of the 401(k), they have a choice to make. One option is to take the money as a cash distribution. While this might seem like a quick infusion of cash, it’s almost always a terrible financial move.

That cash payout will be treated as taxable income. On top of that, if they are under the age of 59 ½, they’ll also get hit with a 10% early withdrawal penalty from the IRS. This can instantly erase a huge chunk of the funds.

Solution-Focused Strategy: The smartest move is a direct rollover. This allows the receiving spouse to move their awarded funds directly into their own IRA or another qualified retirement account. A direct rollover is a tax-free, penalty-free transfer that preserves the money for its intended purpose—retirement.

Forgetting to Update Your Beneficiaries

This is a devastatingly common and easily avoidable error. After your divorce is finalized, you absolutely must update the beneficiary designations on your remaining 401(k), life insurance policies, and other accounts. If you don't, your ex-spouse could legally inherit your retirement savings, even if your will says otherwise.

Federal law (ERISA) often requires the plan administrator to pay out to the person named on the beneficiary form, regardless of what your divorce decree says. This single oversight can unintentionally disinherit your children or new spouse.

What to do now:

- As soon as your divorce is final, contact your 401(k) plan administrator.

- Request the necessary forms to change your primary and contingent beneficiaries.

- Do not assume your divorce attorney or the court will handle this for you. This is your responsibility.

Your Next Steps for Protecting Your Retirement

Knowing what a QDRO is and how the process works is a great start, but real security comes from taking action. This is the moment to shift from learning the concepts to actively protecting your financial future. A 401k split during divorce doesn't have to feel like you're losing control—it's about having a clear, strategic plan to carry you through it.

Protecting your retirement assets begins right now with a few organized, practical steps. This isn't about gearing up for a fight. It's about arming yourself with the right information so you can have a productive, intelligent conversation with an attorney from day one.

Your Immediate Action Plan

Start by creating a dedicated file—a physical folder or a digital one on your computer—and begin gathering the essential documents. Taking this step now will save you a ton of time and stress down the road. More importantly, it gives your legal team exactly what they need to start building a strong case for you immediately.

Here's your initial checklist to get you started:

- Recent 401(k) Statements: Pull together at least the last 12 months of statements for every single retirement account you or your spouse have.

- Pre-Marriage Account Records: This one is crucial. If you had a 401(k) before getting married, you need to find a statement showing its value as close to your wedding date as possible. This is the bedrock of your separate property claim.

- The Summary Plan Description (SPD): Get in touch with your HR department or the plan administrator directly and ask for a copy of the SPD. This document is the rulebook for your specific 401(k) and spells out exactly how it handles divorces and QDROs.

Prepare for Your First Legal Consultation

With these documents in hand, you're ready for a genuinely effective meeting with an attorney. You'll be able to skip the basic fact-finding and dive right into strategy. Before you even make the call, take a few minutes to think about what a successful outcome looks like for you. What are your non-negotiables?

A productive first consultation isn’t just about getting answers; it’s about building a partnership. When you come prepared with your documents and your goals, you empower your attorney to start crafting a personalized strategy from the very first conversation.

Finally, think about how you'd prefer to handle this. Are you and your spouse able to sit down and work things out through mediation? This collaborative approach can save a huge amount of time, money, and emotional energy. Or, is litigation—going to court—the more likely path? Knowing your options helps set the tone for the entire process.

Taking these steps gives you a sense of agency in a situation that can often feel completely overwhelming. You're not just reacting; you're building the foundation for a stable and secure life after divorce.

What to Do Next

The path to protecting what you've worked so hard for starts with a single, confidential conversation. You don't have to figure all this out by yourself. Our team is here to listen, review your specific situation, and map out a clear, strategic path forward.

Take the first step toward securing your future. Schedule a free, no-obligation consultation with The Law Office of Bryan Fagan, PLLC today to discuss your case and learn how we can help protect your retirement savings.

Your Top Questions About Dividing a 401(k) in a Texas Divorce

When you start digging into the details of a 401(k) split during a divorce, it’s completely normal to have a ton of specific, practical questions. Feeling a little lost is part of the process, but getting clear answers is the key to making confident decisions for your financial future. Let's walk through some of the most common questions we hear from our Texas clients every single day.

Can I Keep My Full 401(k) and Give My Spouse Other Assets Instead?

Absolutely. This is a very common negotiation tactic, often called an "asset offset." In Texas, the law calls for a "just and right" division of community property, which doesn't mean you have to slice every single asset right down the middle.

If you and your spouse are on the same page, you can trade the value of the marital portion of your 401(k) for other assets of equal value. For business owners or those with high-value estates, this can mean trading equity in the family home, another investment account, or a business interest. For this to work, you both must agree on the valuation of every asset involved. This approach demands a careful financial analysis to make sure the trade is truly fair and equitable for everyone.

What Happens to a 401(k) Loan I Took Out During the Marriage?

A loan taken out against your 401(k) is almost always treated as a marital debt. The outstanding loan balance simply lowers the net value of the account that’s available to be divided.

For example, let's say the divisible community portion of your 401(k) is valued at $100,000, but you have an outstanding $20,000 loan. The net value that will be split is now $80,000. It's critical that your final divorce decree clearly spells out who is responsible for repaying that loan to avoid any arguments down the road.

How Long Does the QDRO Process Take After the Divorce Is Final?

This is one of those things that can vary wildly and almost always takes longer than people expect. Once the judge signs your divorce decree, the QDRO has to be drafted, reviewed, signed by both of you, and then sent back to the judge for their signature.

From there, it goes to the 401(k) plan administrator for their final review and approval. This is where the delays often happen. Plan administrators in Texas can take anywhere from a few weeks to several months to approve and process a QDRO. Even a tiny error in the paperwork can trigger a rejection, leading to major delays and more legal costs.

What Are My Options After I Receive My Share of the 401(k)?

Once the QDRO is finally approved and the funds are officially yours, you typically have two main options to avoid getting hit with immediate taxes and penalties. The most common and financially sound choice is to do a direct rollover into your own retirement account, like an Individual Retirement Account (IRA).

This is the smartest move because it preserves the tax-deferred status of the money, letting it continue to grow for your own retirement without any immediate financial hit.

Your other option is to take a cash distribution, but this is rarely a good idea. If you go this route, the funds will be subject to ordinary income taxes, and you could face an additional 10% early withdrawal penalty. This can take a huge bite out of the amount you actually get to keep.

You have questions, and you deserve clear, compassionate answers. At The Law Office of Bryan Fagan, PLLC, we believe that informed clients are empowered clients. If you are facing a divorce in Texas and are concerned about protecting your retirement, our experienced attorneys are here to provide the guidance you need. We will help you understand your rights and build a strategy to secure your financial future.

Take the first step today. Schedule a free, no-obligation consultation to discuss your case by visiting https://texasdivorcelawyer.us.