Skip to content

Skip to content Watching the retirement savings you’ve worked so hard to build become a point of conflict in a divorce can be incredibly disheartening.

In Texas, your 401(k) is considered community property, which means the portion you and your employer contributed during your marriage is on the table for division. To split these funds without getting hit by heavy taxes and early withdrawal penalties, you will need a special court order called a Qualified Domestic Relations Order (QDRO). This document is absolutely essential for protecting the nest egg you’ve spent years growing, and understanding how it works is your first step toward financial security.

Your Financial Future and Divorce

It’s natural to feel like you’re losing a piece of your future security when a major asset like your 401(k) gets carved up. You have likely spent years contributing, planning, and watching it grow, only to now see it become part of divorce negotiations. This is a huge source of anxiety for anyone going through a divorce in Texas, and you are not alone in feeling this way.

The good news is that the process for splitting a 401(k) is structured and manageable once you know what to expect. Texas law provides a clear framework for handling these assets to ensure the division is "just and right"—which doesn't always mean a simple 50/50 split of the entire balance.

Understanding the Basics of 401(k) Division

The most important concept to understand is that Texas is a community property state. This legal standard directly controls how your retirement accounts are handled in a divorce. Here’s what that means for you:

- Community Property: According to the Texas Family Code, any money put into your 401(k) from the day you got married until the day your divorce is finalized is considered marital property. This includes your contributions, your employer's matching funds, and all the investment gains and losses that occurred during that time.

- Separate Property: The account balance you had before the marriage, plus any growth specifically tied to those pre-marital funds, is your separate property. This part of the account is not subject to division.

Proving what's separate versus community is often the most challenging part. It requires careful documentation and sometimes the help of a financial expert to trace the funds accurately. This is a critical step in protecting what is rightfully yours. Learning how to prepare for divorce financially can give you a solid foundation for this entire process.

The Role of a QDRO

You might think your final divorce decree is all you need to split the account, but it’s not. A 401(k) plan administrator cannot legally touch the account based on a divorce decree alone. They need a Qualified Domestic Relations Order (QDRO).

A QDRO is a specific court order that gives your retirement plan administrator exact instructions on how to divide the account between you and your ex-spouse. Without a properly executed QDRO, any withdrawal will be treated as a regular, taxable distribution, likely triggering a 10% early withdrawal penalty on top of income taxes. This is a costly mistake you can easily avoid.

Beyond the details of the 401(k) division, understanding the bigger picture of comprehensive retirement planning is crucial for getting back on your feet financially after the divorce. This guide will walk you through each part of the process, giving you the clarity and confidence to protect your assets and move forward.

How Community Property Rules Affect Your 401k

When you're facing a divorce in Texas, what happens to your 401(k) boils down to one core legal principle: community property. While it sounds like legal jargon, the concept is straightforward.

Think of your marriage as a financial partnership. Under the Texas Family Code, nearly everything you or your spouse earned or acquired from the date of marriage until the divorce is finalized belongs to the "marital estate." This is the community property that a judge must divide in a "just and right" manner.

Your 401(k) is absolutely part of that equation. Every contribution you made, any matching funds from your employer, and all investment growth that occurred during the marriage are considered part of the community pot.

Separate vs. Community Property in Your 401k

Here is a critical distinction: not every dollar in your 401(k) is automatically up for grabs. Texas law also recognizes "separate property," which is anything you owned before you were married.

This is the key to protecting the retirement savings that are rightfully yours alone. Here’s the breakdown:

- Separate Property: The total value of your 401(k) on the day you got married is your separate property. Any growth and earnings that can be directly traced back to that pre-marriage balance also remain yours.

- Community Property: All contributions, employer matches, and investment earnings that accumulated from your wedding date onward are considered community property and are subject to division.

The burden of proof is on you to prove which part of the account is separate. If you cannot provide clear evidence, the court will presume the entire 401(k) is community property.

Proving Your Separate Property Claim

This is where the real work begins. To successfully claim a portion of your 401(k) as separate property, you must be meticulous with your records. It’s not enough to simply remember the balance on your wedding day; you have to trace its growth over the years through a process called "tracing and characterization."

This is often where legal battles are fought in a Texas divorce. While some might use a simple subtraction approach, that method often misses the growth on your separate funds. More often, financial experts are brought in to trace the investments and pinpoint exactly what is and isn't divisible.

To build a solid case, you need to start gathering documents like:

- Account statements from immediately before your marriage date.

- Annual statements from throughout the marriage.

- Records of any loans or withdrawals taken from the account.

Getting these records is non-negotiable. To understand the legal weight of this evidence, it helps to know how to conduct legal research and build an effective argument. For a more detailed look at the state laws at play, our guide on what is community property in Texas is a great resource. Arming yourself with this knowledge is the first step in protecting what you’ve worked so hard to earn.

A Practical Guide to Valuing and Dividing Your 401k

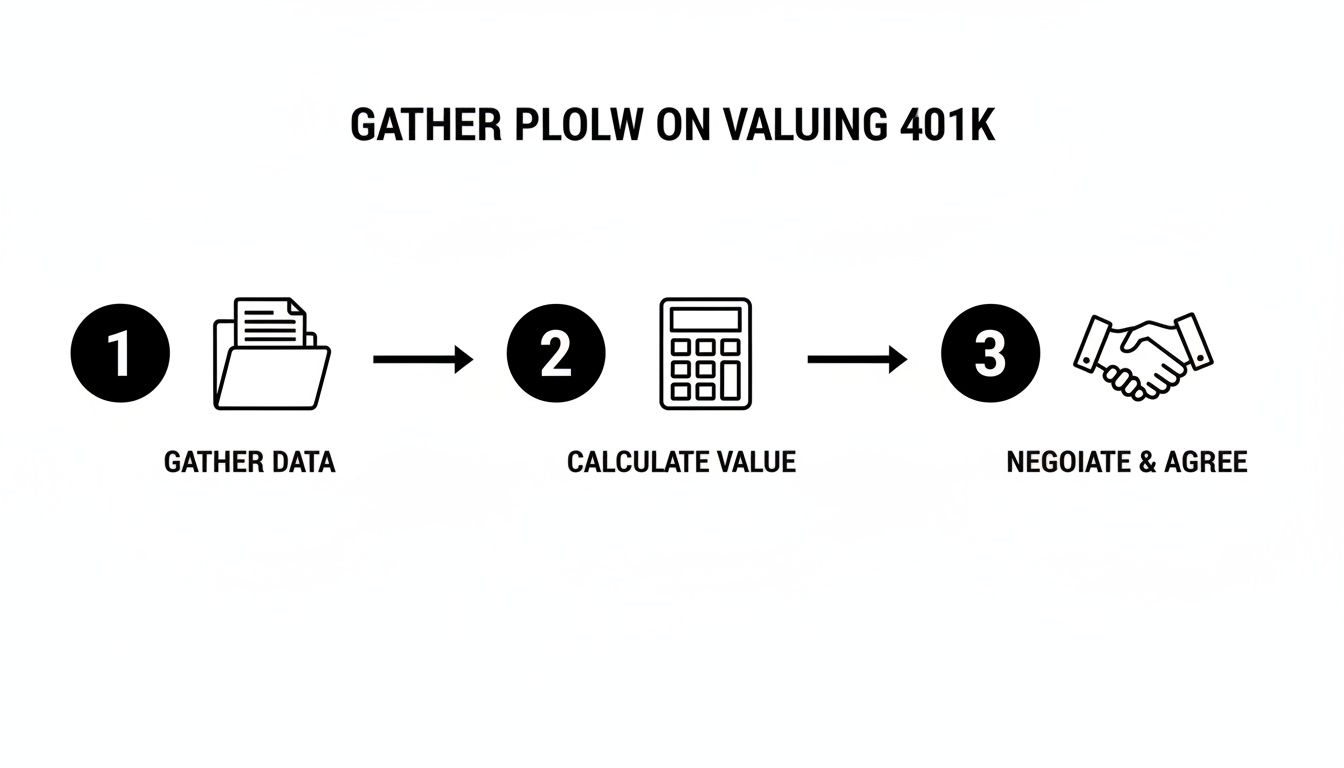

Now that you understand the legal definitions, let's get into the practical, hands-on steps of actually splitting a 401(k). This is where you move from understanding the rules to actively protecting your financial future. It all starts with getting the right paperwork in order.

To determine the true marital portion of a 401(k), you need a clear financial timeline. This isn't just about looking at the latest statement; you need a snapshot of the account's value from the day you got married.

Step 1: Gather the Essential Financial Documents

Your first task is to locate every relevant 401(k) statement. These documents are the foundation of your claim, proving what’s yours alone versus what needs to be split. You will absolutely need:

- The statement closest to your date of marriage: This is the single most important document for protecting pre-marital funds. It establishes the starting value of your separate property.

- The most recent account statement: This shows the current, total value of the account that's on the table in the divorce.

- Annual statements for the duration of the marriage: In a long-term marriage, these can be a lifesaver for tracing the growth of your separate property funds over time.

If you can't find these statements, don't panic. You can request historical records directly from the plan administrator or your company’s HR department. It’s a necessary step to ensure you don't accidentally give up savings that are rightfully yours.

Step 2: Choose the Right Valuation Date

A 401(k)'s value isn't static; it fluctuates with the stock market every day. Because of this, you and your spouse must agree on a specific valuation date to lock in the account's worth for the division. Often, this is the date one of you filed for divorce or a date close to mediation or final trial, but it is negotiable.

This single date matters immensely. Imagine the market tanks right after you file. Using the filing date value could mean your spouse gets a disproportionately large share of the current, depleted account. This decision can swing the final numbers by thousands of dollars, making it a key point of negotiation.

Step 3: When to Bring in a Financial Expert

For many straightforward divorces, your account statements are probably enough. But some situations are too complex to handle on your own. You should seriously consider hiring a Certified Divorce Financial Analyst (CDFA) if your 401(k) involves:

- Outstanding Loans: A loan taken against the 401(k) during the marriage is a community debt. A CDFA can properly calculate how that debt affects the final split.

- Commingled Funds: If you rolled a previous 401(k) or an IRA into your current account during the marriage, a financial expert can trace the separate and community portions to untangle the funds.

- Complex Investment Growth: When it's nearly impossible to tell how much growth came from pre-marital funds versus marital contributions, a CDFA can perform a detailed tracing analysis.

A CDFA provides an objective, third-party valuation that can prevent expensive arguments and ensure the division is truly "just and right," as Texas law requires. Their report often becomes the foundation for a fair settlement.

Step 4: Negotiate the Split

Once the marital portion has a firm value, you have options. A 50/50 split is common, but it's not set in stone. Texas law encourages flexibility, allowing you to negotiate a division that makes sense for your specific situation through mediation or informal settlement talks.

Using other assets to offset the 401(k) value is a powerful negotiation tool. For example:

- Keeping Your 401(k) Intact: If you’d rather not touch your retirement account, you could offer your spouse a larger share of the equity in the family home instead.

- Trading Other Assets: You might agree that your spouse keeps their entire pension in exchange for you keeping your entire 401(k), assuming the values are reasonably close.

- Assuming More Debt: Sometimes, one spouse might agree to take on more marital credit card debt in exchange for keeping more of the retirement assets.

Splitting a 401(k) has profound, long-term consequences for your financial well-being. The reality is that divorce can take a serious toll on retirement savings. An analysis of Census Bureau data revealed that the average married retiree has over $100,000 more in their 401(k) and other savings than a divorced retiree. You can see more details about these retirement savings gaps on Business Insider.

This statistic isn't meant to scare you—it's meant to underscore why meticulous valuation and strategic negotiation are so critical for protecting your financial future.

This process shows that valuing and negotiating are just the first steps. The QDRO is the essential legal tool that makes the division happen.

Key Stages of Splitting a 401k in a Texas Divorce

This table summarizes the critical steps from initial filing to final distribution, helping you track your progress.

| Stage | What It Involves | Key Tip |

|---|---|---|

| 1. Initial Assessment | Identifying all retirement accounts and gathering initial statements. | Start collecting documents early. Don't wait until the last minute to request historical statements. |

| 2. Valuation | Determining the marital portion by establishing values at the date of marriage and the agreed-upon valuation date. | Discuss the valuation date with your attorney. Market fluctuations can significantly impact the final numbers. |

| 3. Negotiation | Deciding on the division percentage (e.g., 50/50) or negotiating an offset with other community assets in mediation. | Think outside the box. Trading assets like home equity for retirement funds can be a win-win. |

| 4. QDRO Drafting | Having an attorney or specialist draft the Qualified Domestic Relations Order (QDRO). | Make sure the person drafting the QDRO is an expert. A poorly written QDRO can be rejected by the plan administrator. |

| 5. Judicial Approval | Submitting the drafted QDRO to the judge for signature along with the Final Decree of Divorce. | The QDRO and the Final Decree are separate documents. Both must be signed by the judge. |

| 6. Plan Administrator Approval | Sending the signed QDRO to the 401(k) plan administrator for their review and approval. | Follow the plan administrator's instructions to the letter to avoid delays or rejection. |

| 7. Distribution | The plan administrator segregates the funds into a new account for the non-employee spouse, who can then roll it over. | Immediately decide what you will do with the funds (e.g., IRA rollover) to avoid potential taxes and penalties. |

The QDRO: Your Key to a Penalty-Free 401(k) Split

Watching your retirement savings get divided is painful enough. The last thing you need is the IRS swooping in to take another huge bite out of it.

Many people assume their final divorce decree is all they need to divide a 401(k), but that’s a costly mistake. If you simply withdraw money from your account to give to your ex-spouse, you’ll be hit with a 10% early withdrawal penalty on top of a massive income tax bill.

There's only one way to avoid this financial disaster: a Qualified Domestic Relations Order, or QDRO. A QDRO is a separate, highly specific court order that gives direct instructions from a Texas judge to your 401(k) plan administrator. It’s the legal key that tells them exactly how to split the account for your divorce without triggering those brutal penalties.

What Exactly Is a QDRO?

Think of it this way: your 401(k) administrator is legally bound by federal law (ERISA) to protect your account. They cannot simply give your money to someone else, even your soon-to-be ex-spouse.

A QDRO is the only legal tool that can override those protections. It authorizes the administrator to create a separate account for your ex-spouse (called the "alternate payee") and transfer their share of the funds.

This document must be perfect. It contains critical details that leave no room for error:

- The full legal names and last known mailing addresses of both spouses.

- The exact, official name of the retirement plan.

- The precise dollar amount or percentage of the benefits going to the alternate payee.

- The specific number of payments or the time frame the order applies to.

If a single detail is wrong or the language is ambiguous, the plan administrator will reject the QDRO. That sends you back to your attorney and the court, racking up more fees and leaving your assets in limbo.

Why Your Divorce Decree Isn’t Enough

Your Final Decree of Divorce is a powerful state document. It officially ends your marriage and spells out the terms you and your ex-spouse agreed to, including that a portion of the 401(k) is awarded to them.

But it’s not enough for the 401(k) company.

Plan administrators are notoriously strict. They operate under federal regulations and have their own internal rules for what a QDRO must include. Your divorce decree simply doesn't contain the technical, ERISA-compliant language they need to act. This is why the QDRO is the final, essential step to execute the financial agreement you reached.

Common Mistakes That Can Invalidate Your QDRO

Drafting a QDRO is not a DIY project. It’s a specialized task at the intersection of Texas family law, federal tax law, and complex financial regulations. One wrong move and the whole thing can get rejected.

Common mistakes include:

- Incorrect Plan Name: Using a casual name like "the AT&T 401(k) plan" when the official legal title is something far more specific.

- Ambiguous Division Formula: Using vague language like "one-half of the marital portion" is often not enough. The order needs a fixed dollar amount or an exact, unchangeable percentage.

- Requesting Benefits the Plan Doesn't Offer: A QDRO can't force a plan to do something it's not designed to do, like issue a lump-sum payment if the plan only allows for annuities.

- Forgetting Survivor Benefits: The order must clearly state what happens if either you or your ex-spouse passes away before the funds are fully paid out.

A rejected QDRO is more than a paperwork headache. It can leave your ex-spouse without the funds awarded to them in the divorce, potentially exposing you to an enforcement action from the court for failing to comply with the decree. Having an experienced Texas family law attorney draft your QDRO is non-negotiable to get it right the first time.

Strategic Decisions After the 401k Is Divided

Once the QDRO is approved, you can finally breathe a sigh of relief. But this is just the beginning of your new financial life. Now is the time to shift your focus from dividing assets to confidently rebuilding your own secure retirement plan.

Whether you’re receiving funds or your account was divided, the choices you make next are just as important as those made during the divorce. This is your chance to take control and set a new course.

For the Spouse Receiving the 401k Funds

If you are the "alternate payee"—the spouse who just received a portion of your ex's 401(k)—you have a few options. Acting thoughtfully is critical due to the long-term tax consequences.

Your best option in nearly every scenario is to execute a direct rollover into an Individual Retirement Account (IRA) in your name. By moving the funds directly from your ex-spouse's 401(k) plan into your new IRA, you avoid immediate taxes and the 10% early withdrawal penalty. Your money stays invested and continues to grow tax-deferred.

You could also take a cash payout. A QDRO gives you a one-time pass to avoid the 10% penalty, but the money will face a mandatory 20% federal tax withholding. The entire amount is also treated as ordinary income, which could push you into a higher tax bracket. Unless you are facing an extreme financial emergency, cashing out is rarely a smart move.

For the Spouse Whose 401k Was Divided

Seeing your 401(k) balance drop can be disheartening, but this is not an endpoint; it’s a new starting line. Your focus should immediately shift to a proactive rebuilding strategy to get your retirement savings back on track.

The most direct way to recover is to increase your future contributions. If you’re not already maxing out your annual contributions, now is the time to get as close as you can. For those over 50, take full advantage of the "catch-up" contributions allowed by the IRS, which let you save thousands more each year.

This is also a perfect opportunity to re-evaluate your entire investment portfolio. With a new, single financial future ahead, your old strategy might no longer fit your goals. Consider if a slightly more aggressive allocation is appropriate to help you make up for lost time.

Adjusting Your Retirement Timeline and Goals

A divorce changes everything, including when you might be able to retire. Both you and your ex-spouse should use this moment to conduct a complete financial review.

Practical steps to take right now include:

- Create a New Budget: Your income and expenses have changed dramatically. A new, realistic budget will show you exactly how much you can afford to save.

- Recalculate Your Retirement Needs: Use a retirement calculator to project how much you’ll need based on your new financial reality. This will give you a clear, updated savings target.

- Meet with a Financial Advisor: A professional can help you create a personalized financial plan, adjust your investment strategy, and provide objective advice to help you feel confident about your future.

What to Do Next: Take Control of Your Financial Future

Untangling a 401(k) during a Texas divorce can feel overwhelming, but you can get through it with a clear, strategic plan. It all comes down to understanding Texas community property law, valuing your retirement correctly, and using a perfectly drafted QDRO to finalize the split. These aren't just legal hoops to jump through—they are the building blocks for your financial security after the divorce is final.

The decisions you make right now will directly shape your long-term financial health. Don't let anxiety or uncertainty paralyze you. It’s time to move from uncertainty to action. Your hard-earned savings are far too important to leave to chance. For more strategies you can implement right away, our guide on how to protect assets during divorce is a great next step.

At The Law Office of Bryan Fagan, PLLC, we help Texas families navigate the complexities of property division with empathy and confidence. We are here to provide the clear explanations and practical advice you need to protect your future.

Schedule a free, confidential consultation with us today and let us help you safeguard the retirement you've worked so hard to build.

Key Takeaway

Protecting your 401(k) in a Texas divorce requires three critical actions:

- Trace Your Separate Property: Gather pre-marriage account statements to prove what is yours alone.

- Negotiate Strategically: Use mediation to reach a fair division, potentially trading other assets to keep your retirement intact.

- Insist on a Professional QDRO: This non-negotiable legal document is the only way to split the account without facing massive taxes and penalties.

Unpacking Common Questions About Dividing a 401(k) in Texas

When you're going through a divorce, it's the real-world, practical questions that keep you up at night. Let's tackle some of the most common questions we hear from clients just like you.

Can my spouse get half of my 401(k) if we were only married for a few years?

Yes, but it's not half of the entire account. While the length of your marriage doesn't change Texas's community property rules, it completely changes the math.

If you were married for only two years, for example, the court is only looking at the contributions and growth that happened during that 24-month window. Anything you had in the account before the marriage is your separate property and stays yours. So while your spouse is entitled to a "just and right" share of the marital portion, that piece will be much smaller than in a 20-year marriage.

What happens if I take money out of my 401(k) during the divorce?

Taking money from your 401(k) while a divorce is underway is a very bad idea. The moment a divorce is filed in Texas, most courts put Standing Orders in place that freeze your financial accounts. These orders prevent either spouse from making unusual transactions or draining assets without permission.

If you ignore this and make a withdrawal, a judge could see it as an attempt to hide or waste community funds. They could penalize you by awarding your spouse a larger portion of the remaining assets to make up for the money you took. It’s far better to leave the account untouched until the divorce is final.

Do I have to sell my investments to split the account?

In most cases, no. You don't have to liquidate the stocks or mutual funds inside your 401(k) to divide it. When the QDRO is processed, the plan administrator usually handles the split in one of two ways:

- In-Kind Transfer: This is the most common method. They simply transfer a portion of each investment directly into your spouse's new account. So, if you have 100 shares of a fund, they might get 50 of those exact shares.

- Cash Equivalent: Less common, but sometimes the administrator will calculate the cash value of your spouse’s share and transfer that dollar amount.

The method used depends on the 401(k) plan's rules. The goal is always to divide the assets without triggering a taxable event, which means keeping the underlying investments intact whenever possible.

Protecting your retirement savings is one of the most critical parts of your divorce. The choices you make now will shape your financial security for decades. The team at The Law Office of Bryan Fagan, PLLC is here to bring clarity and skilled legal strategy to the table, ensuring your future is safeguarded. Schedule a free, confidential consultation with us today to discuss your specific situation and get started.